Life

General

Support

Resources

Building Reliable Insurance Systems

That

Hold Up in Real Life

Featured 25 th May 2026

⏱️30 seconds Transparency Report Summary

- Death claim settlements got faster: 76% closed within 3 days; average TAT at 1.82 days.

- Claim payouts scaled up: Total claims settled touched ₹4.58 billion, up 59.18% YoY.

- High-value claims: Largest Group Term Life claim of ₹4.5 crore came from Maharashtra.

- Don't Miss "The Year That Was": Our fast and quirky proof-points from FY26.

- Customer servicing stayed ahead: Most policy servicing request TATs averaged nearly same day. Complaint resolution averaged 4.13 days.

- WhatsApp support scaled: 3,500+ customers served with 12,000+ chats.

- Call centre performance: Volumes up 59.58% YoY. Talk time improved (5:38 → 5:06) with 71% first-time resolution.

- Underwriting decisions got quicker: ~90% completed within ~13 hours.

- System resilience remained strong: 99.82% uptime for policy issuance systems, 99.96% for claims systems.

- Policy issuance stayed efficient: 90.29% of retail policies issued within 15 hours. High-value group policies (₹30 crore) issued in as little as 10 working hours.

- Operational scale peaked: 1.37 lakh policies issued in a day; 1.44 lakh lives covered under one group policy.

- Our Financials: GWP grew to ₹1,990 crore from ₹1,316 crore, with ~38% growth in new business premium.

"There is more wisdom in your body than in your deepest philosophy."

—Friedrich Nietzsche

Every institution claims to have a purpose and talks about reliability. For a life insurer, reliability can’t be a tagline; it quietly exists in what a family experiences when life takes an unexpected turn.

It’s because our moment of truth rarely arrives on a good day. It arrives when a family is already carrying grief, uncertainty, and urgent decisions. In that moment, “support” can’t be a promise or a paragraph on a website. It has to work like an operating system that is built into how we underwrite, how we communicate, how we assess claims, and how quickly we act.

So, we asked ourselves a simple question: if our role is to protect futures, what should that look like in practice at Digit Life Insurance?

For us, it comes down to four anchors: showing up with empathy and respect; making every step clear and easy to follow; applying consistent checks and data-led decisioning so outcomes stay accurate and defensible; and earning customer confidence through dependable service and transparent reporting.

In Digit Life Insurance’s 4th Transparency Report, we open up the data, the decisions, and the systems behind these anchors. The idea is not to claim perfection, but to show our work: what’s improving, what we’re learning, and how we’re building a life insurance company that holds steady when life doesn’t.

BUILT-IN RESPONSIVENESS: WHEN CLAIMS

TURN INTO

REAL MOMENTS

In life insurance, reliability is experienced—not announced. It shows up in what happens after a claim is raised: how quickly we respond, how clearly we guide, and how steadily the case moves from intimation to decision.

This isn’t about motivation. It’s about design. When a family is already dealing with an emotionally difficult moment, speed without clarity creates anxiety—and clarity without action becomes a waiting room. That’s why we’ve built an operating rhythm that prioritises quick acknowledgement, simple communication, and consistent progress.

In the pages ahead, we share what this looks like in practice: our death claim settlement timelines, the claims we paid across products, and some of the largest claims we settled—so the outcomes are as visible as the intent.

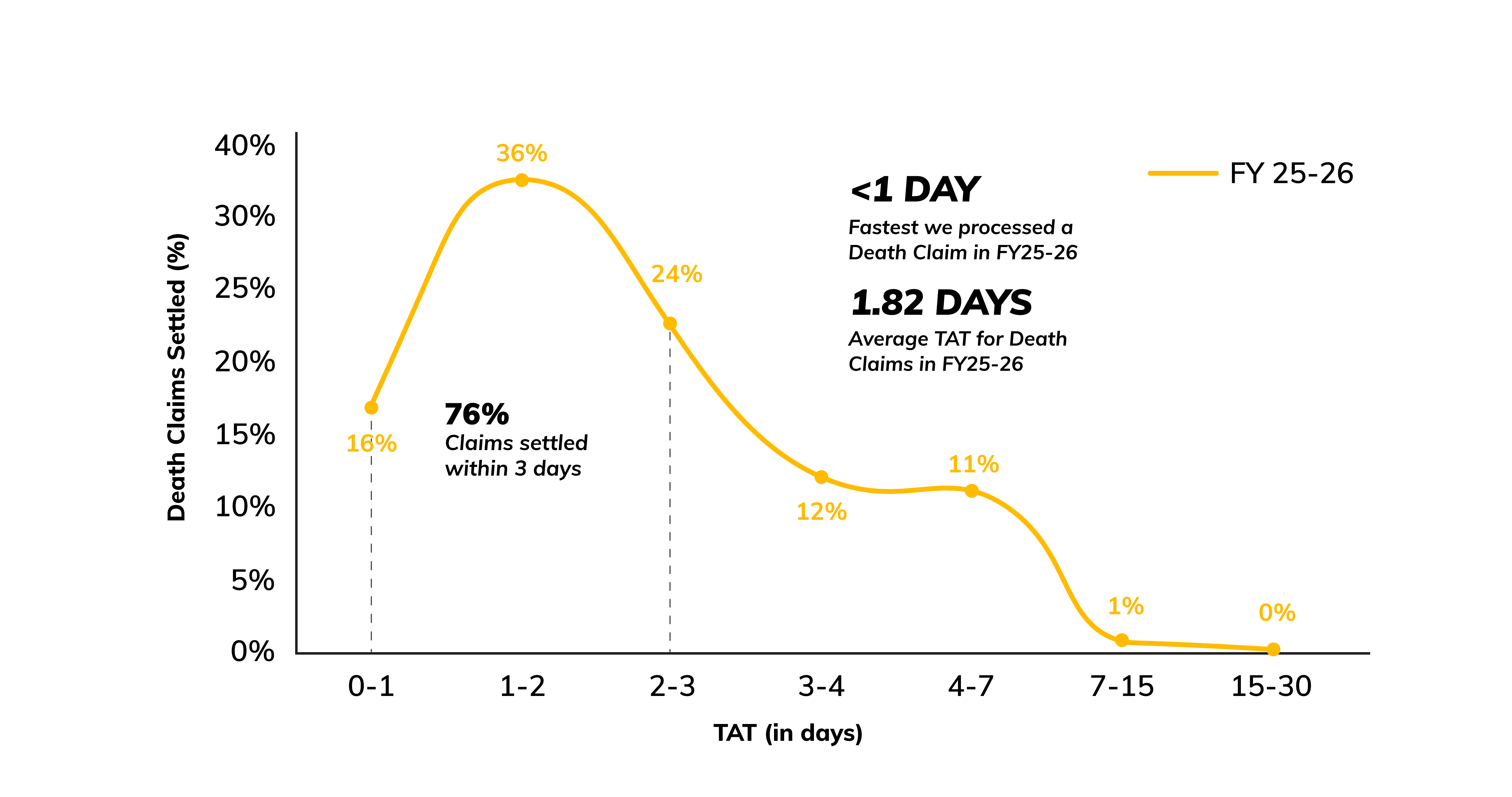

Digit Life Settles 76% Death Claims within

3 Days in FY26

Death Claims Settlement TAT

Note: The above Turnaround Time (TAT) distribution is based on all death claims settled during FY25–26 from the Last Document Received (LDR), defined as the customer’s final action, up to the time taken for completion of our claims processing.

In FY25-26, death claim settlements were largely concentrated within the first few days, reflecting a strong early turnaround. 76% of claims were settled within 3 days, with 36% (the highest share) closed in the 1-2-day window. Longer timelines form a very small tail, with just 1% of claims taking 7-15 days and negligible cases extending beyond that. The average settlement time stood at 1.82 days, while the fastest claim was processed in under a day. End-to-end death claim settlement time improved to 6 days in FY25-26 (from 13.78 days in FY24-25), reflecting faster closure across the full journey.

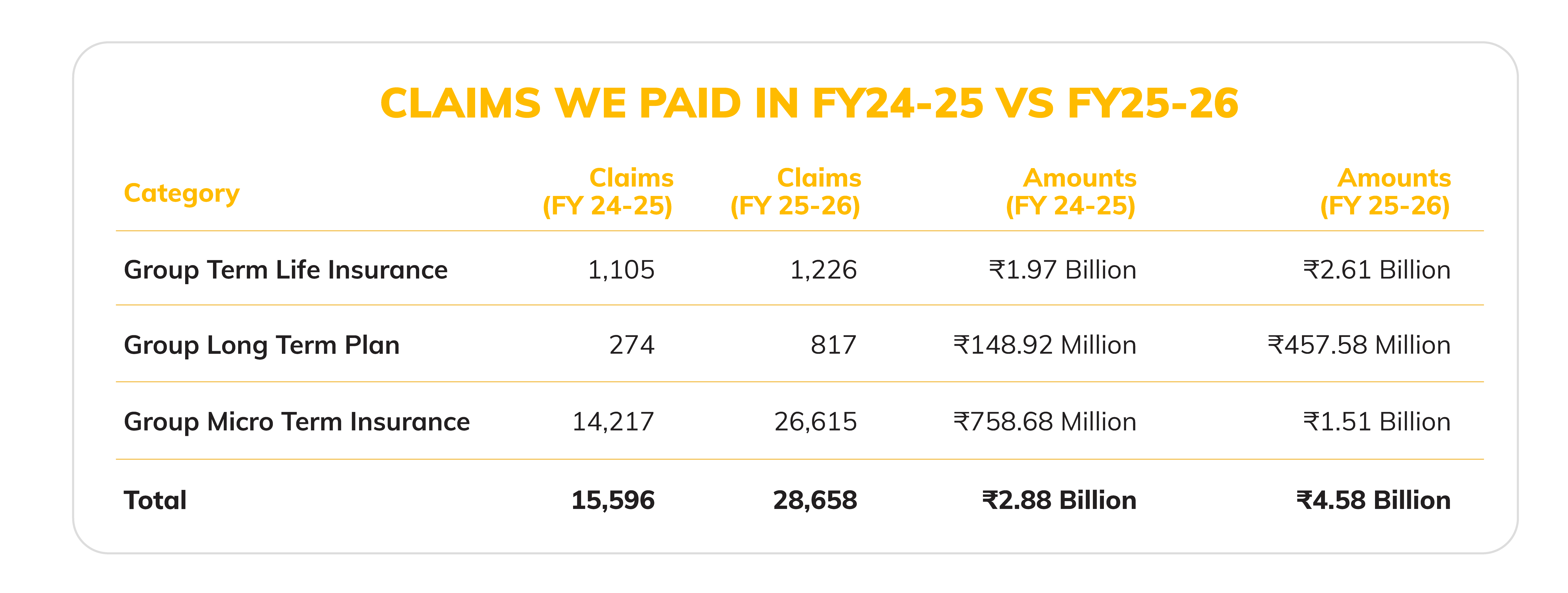

Digit Life Settles ₹4.58 Billion in Claims; Group Micro Term Insurance Category Sees Highest Number of Claims

Every claim we receive represents a life lived, and a family now navigating a difficult moment. That's why we believe being transparent about how many claims we paid across product categories is important.

In FY25-26, we paid 28,658 claims, providing financial stability to many. Our ability to show up for our customers is scaling rapidly. In FY25-26, we disbursed ₹4.58 billion in claims, a 59.18% increase over the previous year.

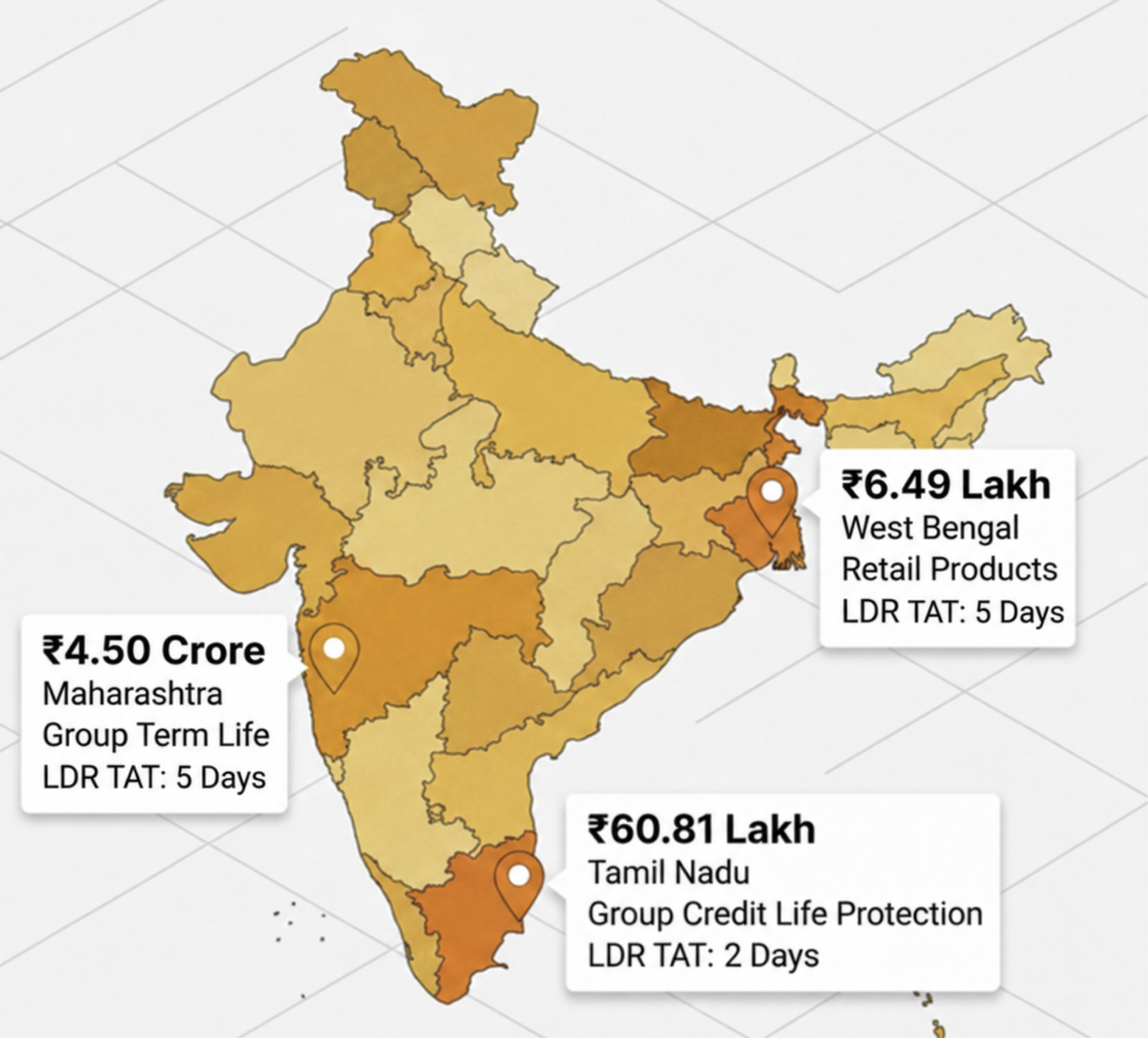

Digit Life Insurance’s Biggest Single Claim Settled Touches ₹4.5 Crore in FY 2025-26

High-value claims are where systems are truly tested. When the stakes are high, families need clarity, speed, and consistency without added friction. Here are the biggest claims we settled in FY26, category-wise.

In Group Term Life, the biggest death claim was settled in Maharashtra for ₹4.50 crore. The Last Document Received Turnaround Time (LDR TAT) for the same was 5 days. In Retail Products, the biggest death claim was settled in West Bengal for ₹6.49 lakh (LDR TAT: 5 days). In Group Credit Life Protection, the biggest death claim was settled in Tamil Nadu for ₹60.81 lakh (LDR TAT: 2 days).

Note: Claims Settlement TAT or LDR TAT is the time taken to settle the claim after receiving all the necessary claims-related documents and decision.

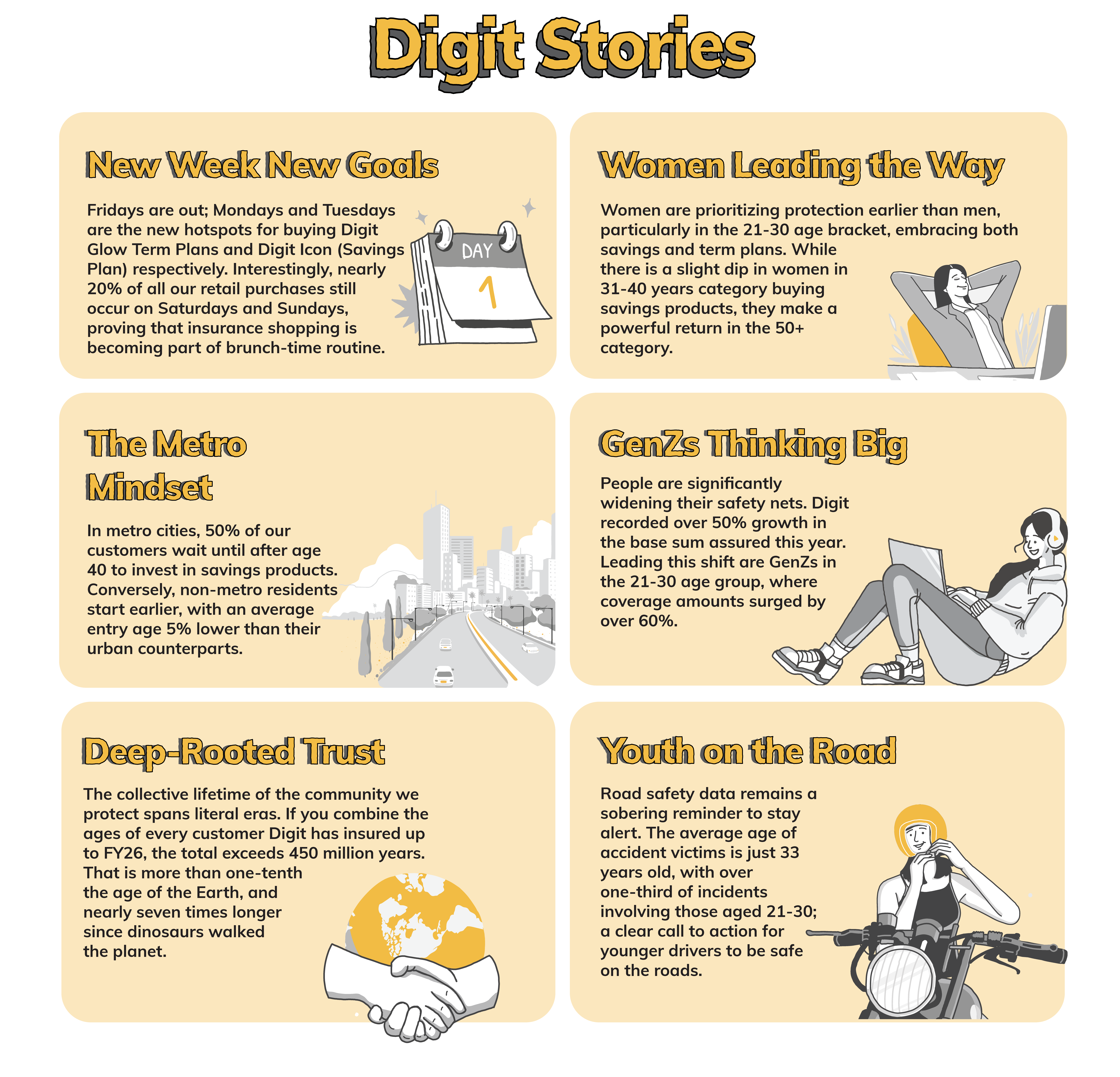

Before we dive into what’s next, let's take a look at few bite-sized stories from the year that went by.

SHOWING UP IN EVERYDAY ACTIONS

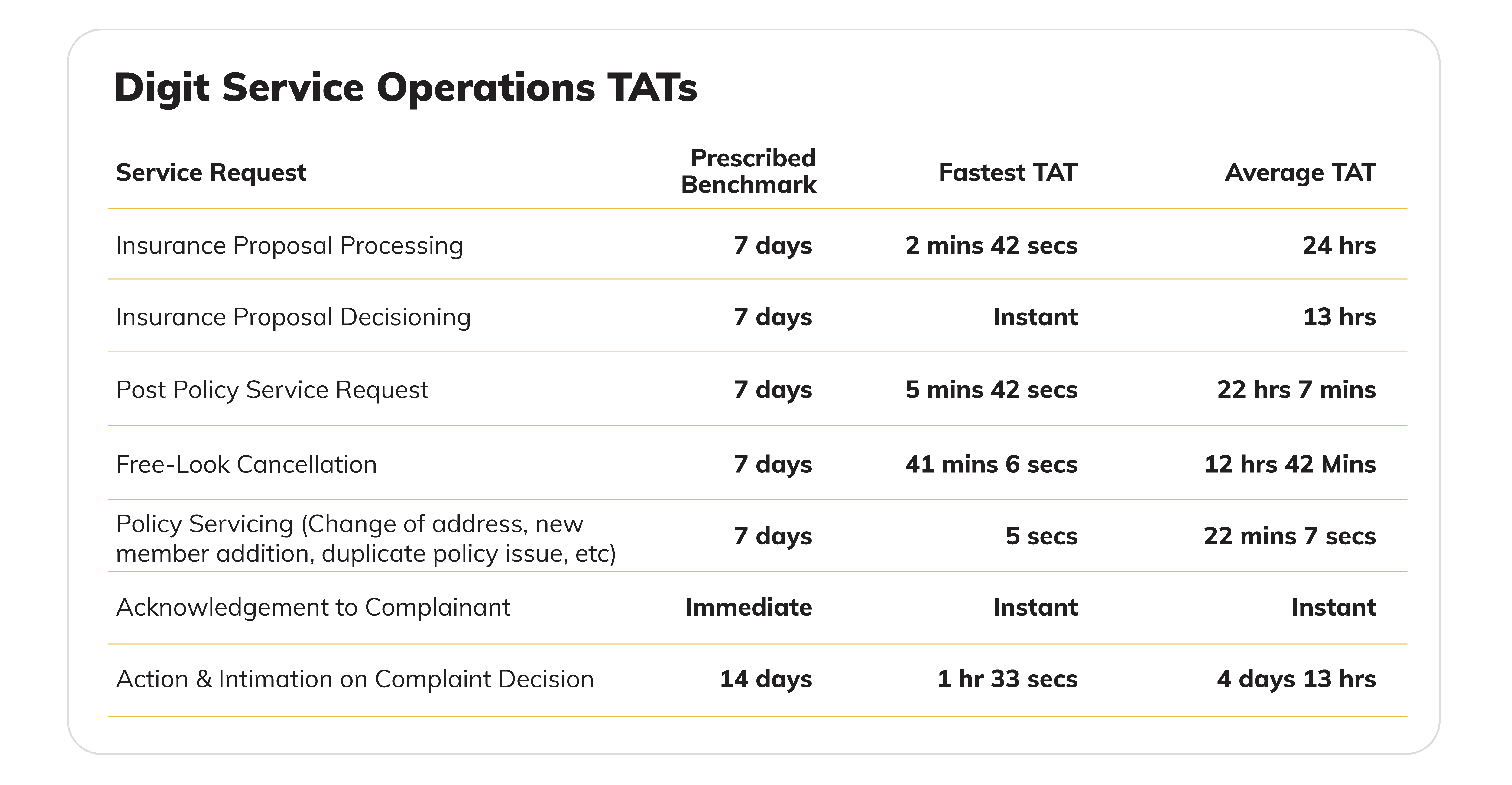

Trust in insurance is forged not just during claims, but in the quiet consistency of everyday service. While IRDAI timelines establish the baseline, our performance across key operations reflects a commitment to speed that moves well beyond the prescribed benchmarks.

Most service request fixes done on same day at Digit Life; average complaint decisioning in FY25-26 at 4.13 days

We have transformed turnaround times into instant interactions. Against a 7-day standard, our proposal processing now averages just 24 hours (with record speed of under 3 minutes), while decisions are reached in an average of 13 hours. This agility extends throughout the policy lifecycle: servicing updates that could take days are often completed in mere seconds, and free-look cancellations are processed in an average of 12 hours 42 minutes rather than the prescribed 7-day TAT.

Note: All TAT is measured from the Last Document Received (LDR), defined as the customer’s final action, up to the time taken for completion of our processing; TAT for complaint decision is measured from the receipt of the complaint up to the time of closure. TAT is calculated post receiving all necessary requirements.

Even when challenges arise, our grievance resolution outpaces the 14-day window by a significant margin, averaging just over 4 days. By treating every request with the urgency of a claim, we try to ensure that our responsiveness isn't just a metric but becomes a hallmark of our reliability.

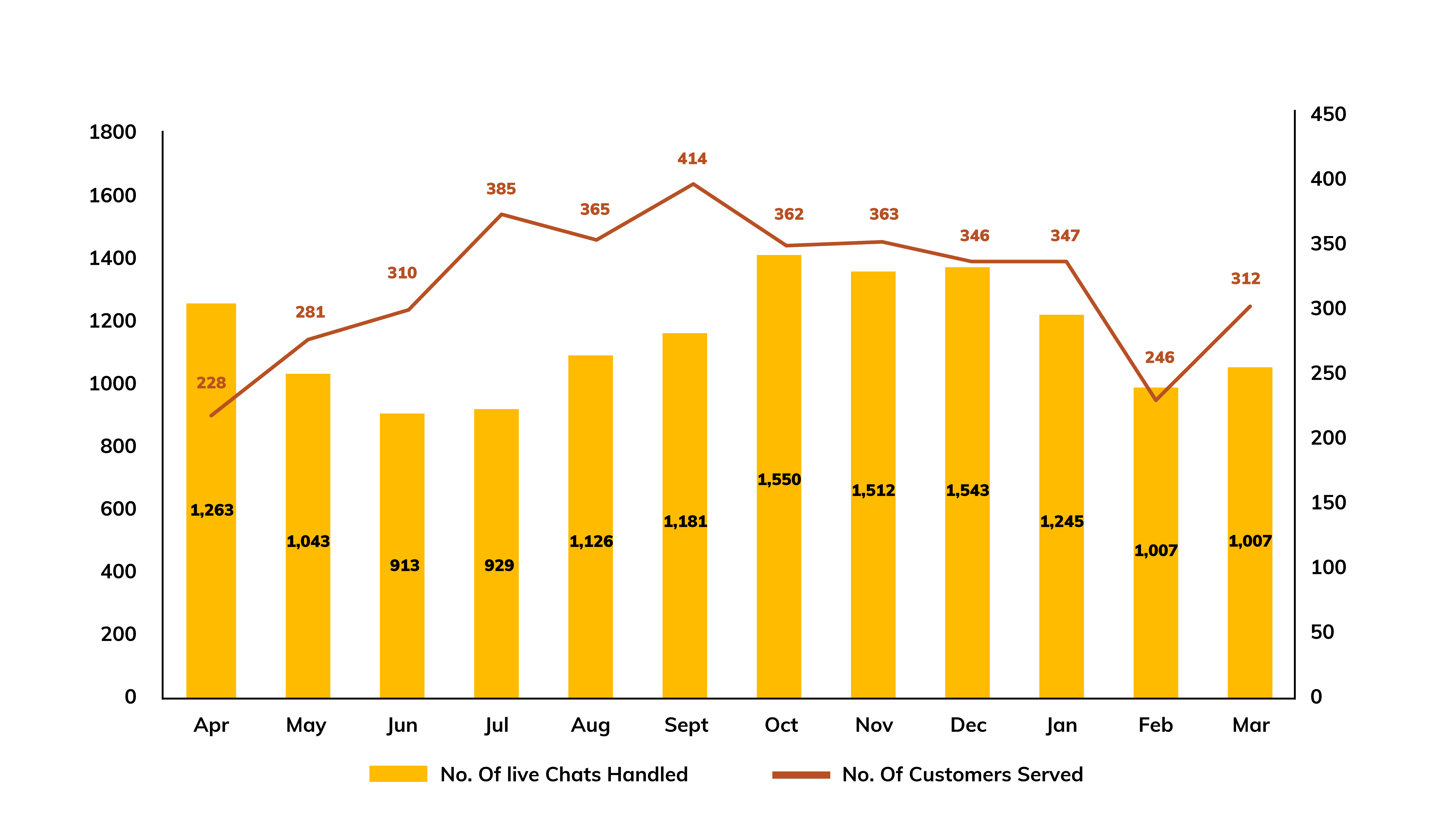

WhatsApp: Meeting Customers Where

They Already Are

For most customers, the quality of an insurance company is not experienced in the product brochure or the premium rate. It is experienced the first time they call with a question, or message on WhatsApp to check a status. Those are the moments that define whether they renew, recommend, or regret. That’s why we track our customer service metrics closely.

WhatsApp Self-Service: Customer Requests at a Glance

WhatsApp is how India communicates. Our WhatsApp support channel serviced close to 3,500 customers and handled over 12,000 live chats in FY26 alone. Customers use it to check policy status, submit claim documents, ask renewal questions, and get guided through processes that would otherwise require a call.

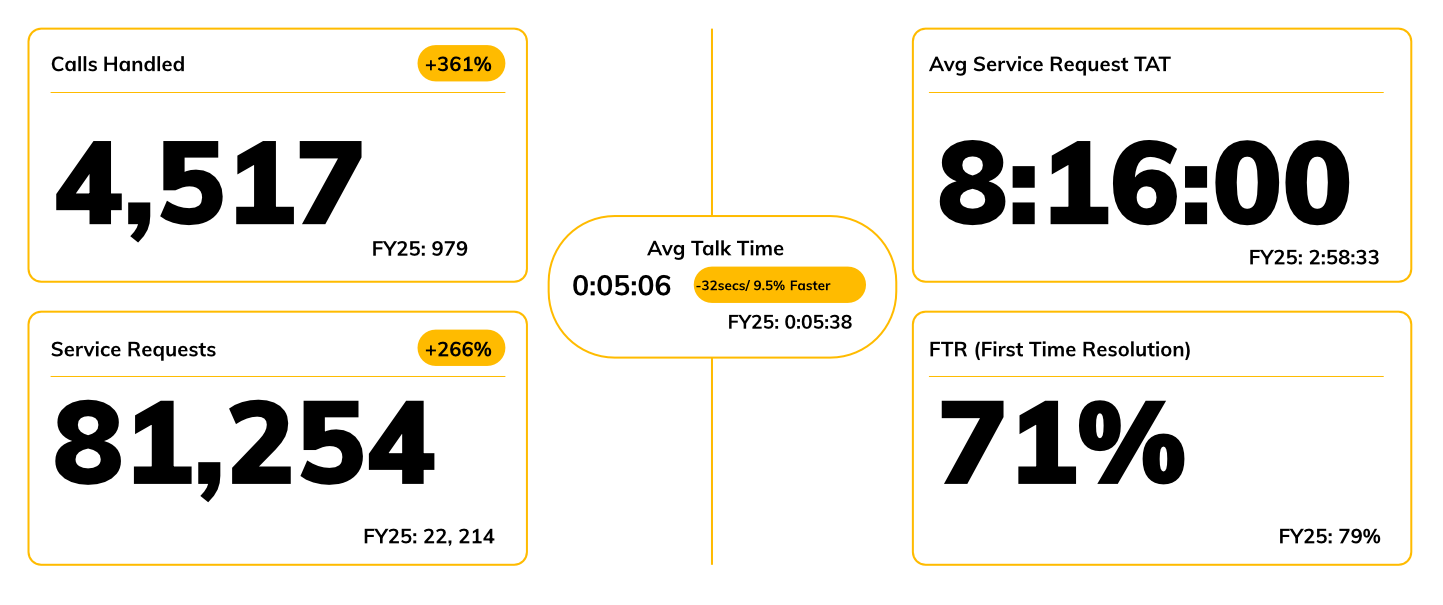

Call Centre Quality Stays Tight as Volume Grows

In FY26, we handled over 4,500 calls, a 361% jump from FY25. This volume increase is a consequence of our growing customer base, more active policyholders, and a larger claims portfolio. Despite increasing call volume, our average talk time slightly improved 5 mins 38 secs to 5 mins 06 secs. 71% of our customers in FY26 received First Time Resolution (FTR), meaning customers continued to get closure the first time they reached us.

CUSTOMER SUPPORT: FY26 VS FY25

The Blueprint of Reliability, Powered by Technology

At Digit Life, we believe technology is most powerful when it acts as a bridge, not a barrier. We continue to invest in Artificial Intelligence to simplify the complexities of life insurance, ensuring our processes are as human-centric as they are high-tech. By blending AI-driven automation with thoughtful human judgment, we aren't just making insurance faster; we are making it more accountable, fair, and accessible for every life we protect.

AI-Driven Video Medical Examination Report (VMER)

Traditionally, medical underwriting has been a significant point of friction—a necessary but often intrusive step in securing a life insurance policy. To solve this, we introduced the AI-powered VMER system, a digital interaction layer that brings the medical examination to the customer, wherever they are. The system uses a real-time Voice AI bot to guide applicants through identity verification and structured health questionnaires. Natural Language Processing (NLP) capturing inputs in standardized form while keeping the experience as natural as a conversation. Importantly, we follow a human-in-the-loop approach. AI supports secure, consistent data collection, while trained medical underwriters review the organized responses and images and make the final risk assessment. This helps reduce turnaround times without compromising rigour for the wider pool of policyholders

AI-Powered Life Insurance Renewal Calling Agent

A life insurance policy is only as good as its continuity, and to help families avoid losing their safety net due to missed payments, we deployed a Multilingual Voice AI Agent as a proactive guardian for policy persistence. Built for India’s linguistic diversity, it converses naturally in Hindi, English, Tamil, Telugu, and Marathi, and manages both ECS and Non ECS journeys so customers are informed before a policy expires. It handles identity verification and addresses policy-specific questions in real time. Every interaction is evaluated using an LLM-as-a-Judge framework, while business teams retain full oversight—no financial or policy action is executed without explicit, recorded customer confirmation.

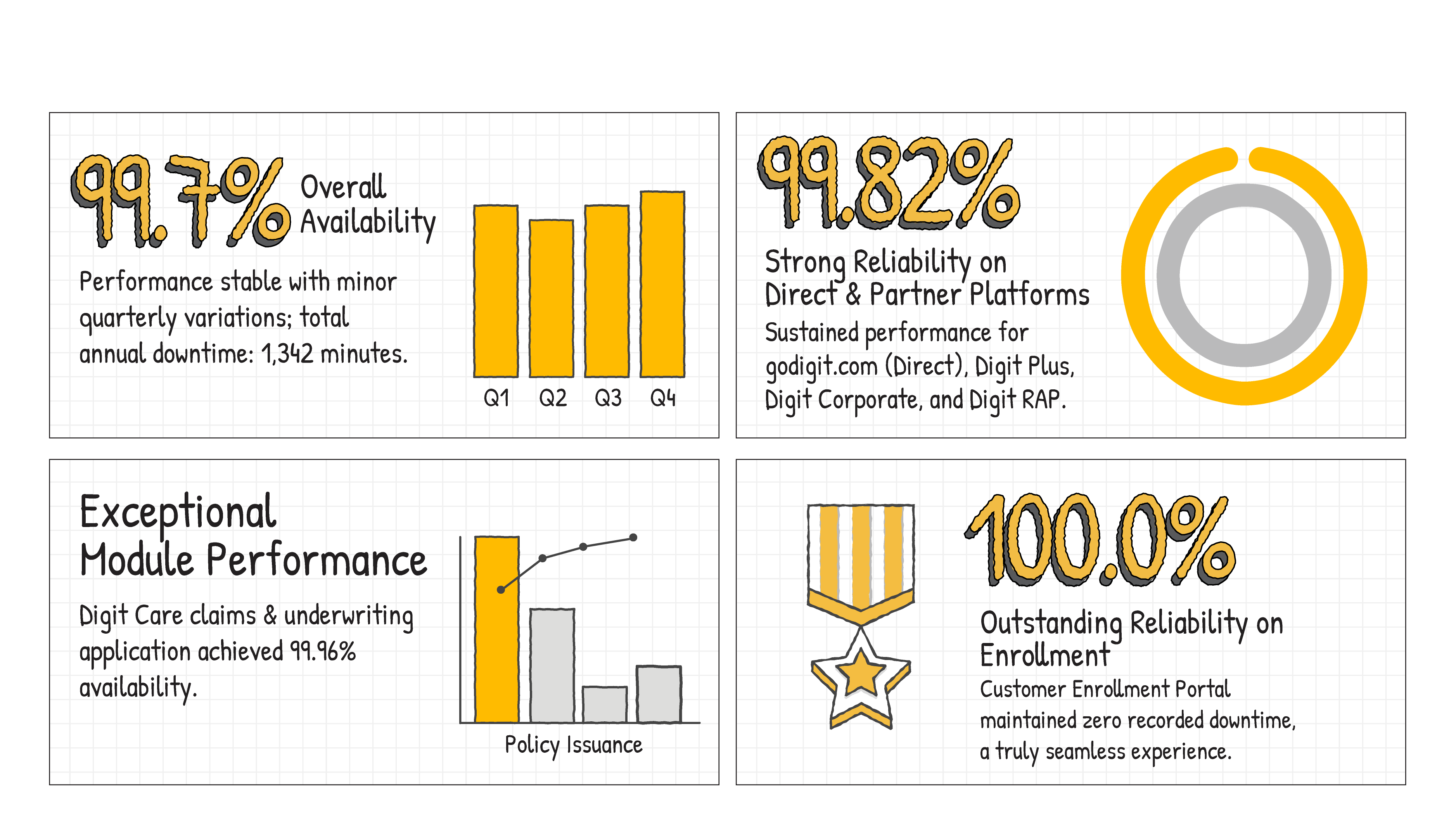

Reliability Is Not Accidental: Systems That Stay On

System reliability matters most not when everything goes right, but when something doesn't.

In FY 25-26, we fortified our digital backbone to ensure we never sleep. This resilience is reflected in our metrics: 99.82% reliability for policy issuance platforms and 99.96% for the Digit Care claims system. Most notably, our Customer Enrollment Portal achieved a perfect 100% availability, delivering a seamless experience when our partners and customers needed us most.

FY25–26 Life Insurance Systems Performance Dashboard

Note: Perfomance data reflects consolidated availability across core life insurance platforms.

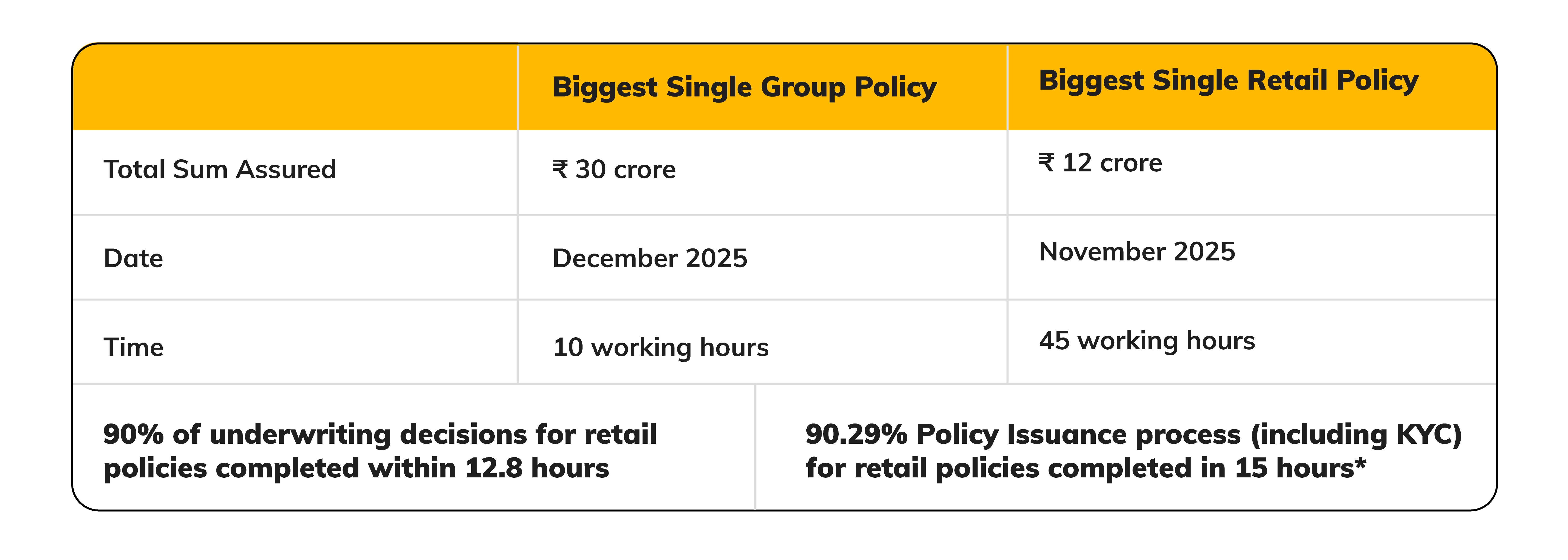

Big Policies, Issued Fast

In FY 2025-26, we accelerated our Policy Issuance efficiency: 90.29% of retail policies, including the mandatory KYC, were completed within 15 hours, while 90% of all cases received an underwriting decision within approximately 13 hours. Our systems handle high-value complexity with ease—issuing a ₹30 Crore Group policy in just 10 working hours and a ₹12 Crore Retail policy in 45 working hours from the final document submission.

*TAT for policy issuance/underwriting decision includes time taken to issue/decision the policy after last document received.

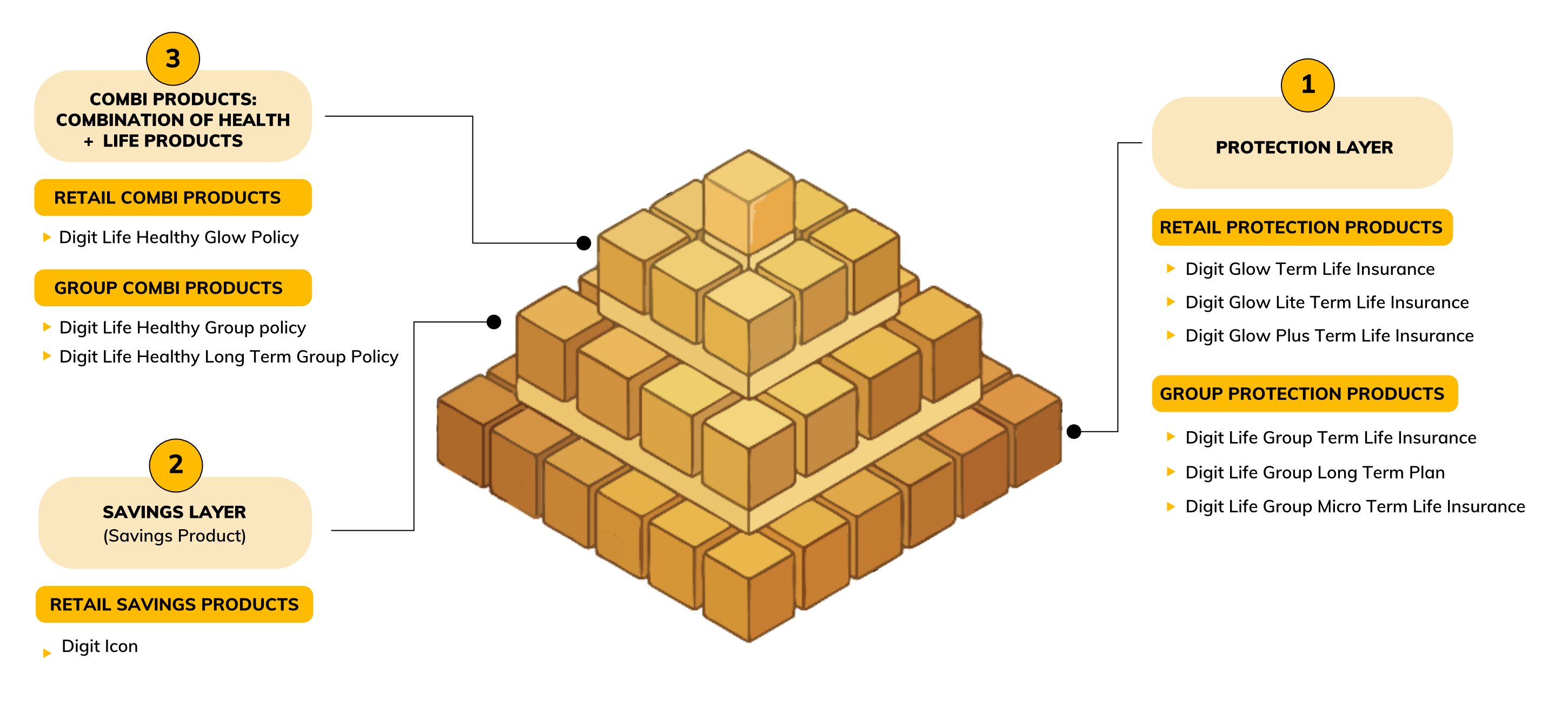

How Our Products Serve Different Lives

We built Digit Life to serve a country — not a demographic. We believe insurance should fit a life, not the other way around. Same insurer. Same commitment. Different lives.

The following portfolio represents our active product lineup of FY25-26, spanning across our Protection, Savings, and Combi layers for both Retail and Group segments.

DIGIT LIFE INSURANCE PRODUCTS

A PYRAMID APPROACH TO FINANCIAL WELL-BEING

Note: Digit Glow Term Life Insurance (UIN: 165NOO5VO1), Digit Glow Lite Term Life Insurance (UIN: 165NOO6VO1), Digit Glow Plus Term Life Insurance (UIN: 165N007V02), Digit Life Group Term Life Insurance (UIN: 165N004V01), Digit Life Group Long Term Plan (UIN: 165N002V01), Digit Life Group Micro Term Life Insurance (UIN: 165N008V01), Digit ICON (UIN: 165N011V04) are insurance products offered by Go Digit Life Insurance Limited.

Digit Life Healthy Glow Policy (UIN: GODHLIP26044V022526), Digit Life Healthy Group Policy (UIN: GODHLGP24094V012324), and Digit Life Healthy Long Term Group Policy (UIN: GODHLGP24114V012324) are insurance products offered by Go Digit Life Insurance (for Life Cover) in collaboration with Go Digit General Insurance (for Health Cover), which is the lead insurer. The products of the Combi Products are also available individually, as applicable. These are subject to terms, conditions, exclusions, and regulatory approvals. Please read the policy documents carefully before purchasing.

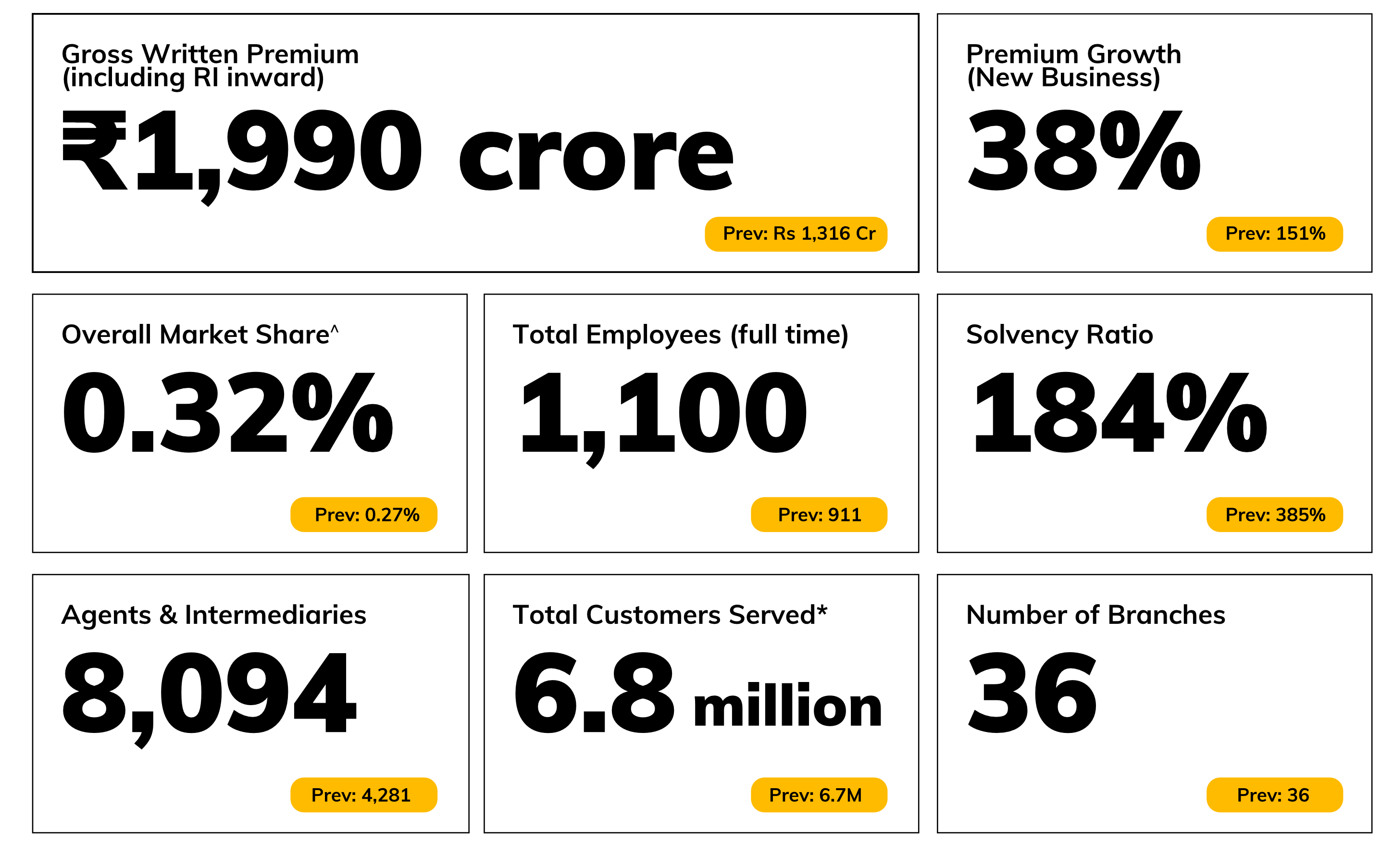

WHAT OUR NUMBERS LOOKED LIKE: FY26 vs FY25

Life insurance is a long-duration promise—one that must hold up years, even decades, after a policy is issued. That requires a financially strong, well-capitalised business that grows with discipline. That’s why it’s important to show you where we stand across key scale and strength indicators.

*Number includes customers/lives covered under policies issued during the period. ^Market share calculated based on IRDAI's monthly published data on New Business Statement of Life Insurers for the period ended March 31, 2026. All FY24-25 data as on March 31st 2025; All FY25-26 data as on March 31st 2026.

In FY 2025–26, Gross Written Premium (including RI inward) grew from ₹1,316 crore to ₹1,990 crore, while new business premium saw a growth of 38%. Customers serviced edged up to 6.8 million, and overall market share increased to 0.32%. Our agents & intermediaries nearly doubled from 4,281 to 8,094, while the solvency ratio remained strong at 184%.

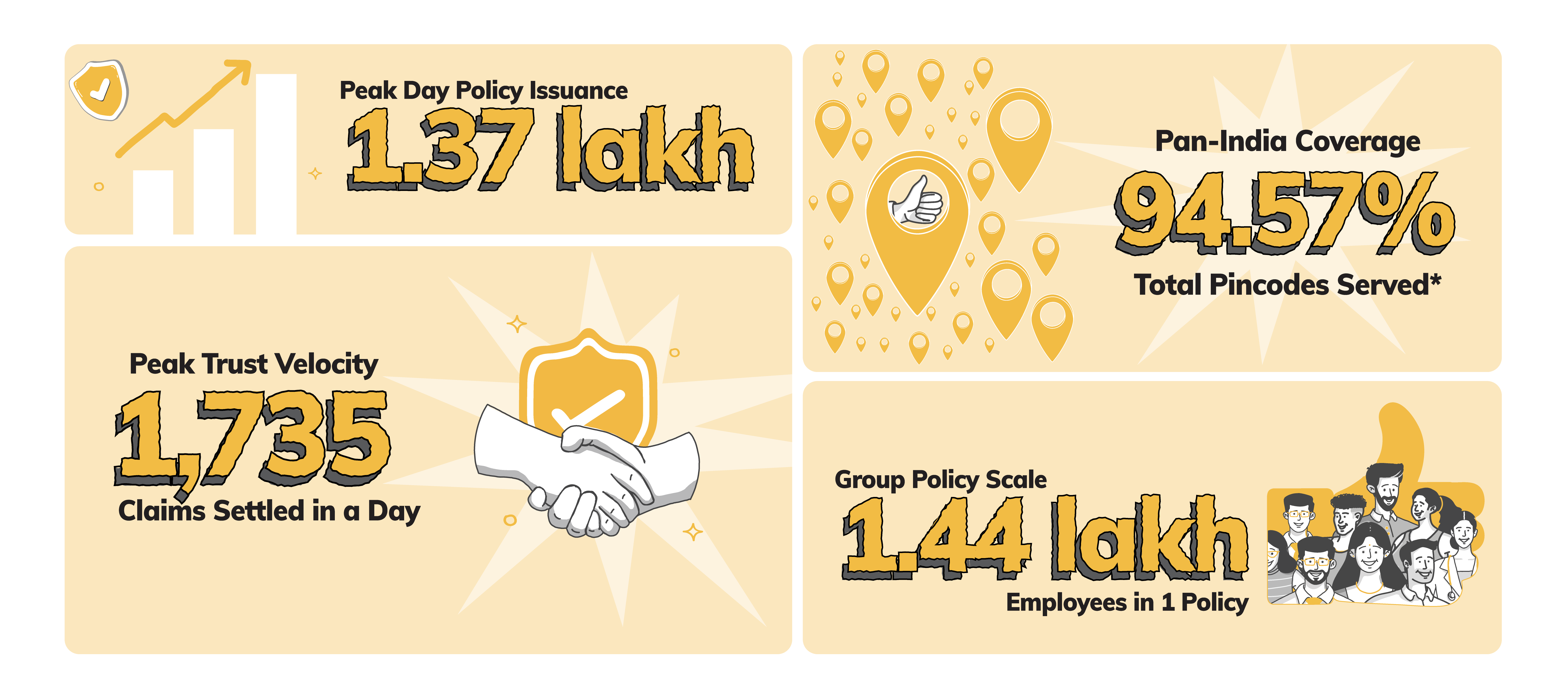

CAPTURING OUR GROWTH NUMBERS IN FY 2025–26

In FY 2025–26, we hit a peak of 1.37 lakh policies issued in a single day, reflecting strong operational scale. In group business, the largest single group policy covered 1.44 lakh employees, underscoring our ability to serve large cohorts seamlessly. Our reach expanded to 94.57% of serviced pincodes, strengthening accessibility across geographies. We also recorded a high of 1,735 claims settled in a single day, demonstrating the system’s capacity to deliver outcomes at scale.

*Pincode List in India (Source: India Post)

It's time to wrap up!

We hope this report was an easy 9-minute read. We’ll be back with the next drop in October 2026. Until then, tell us what worked, what didn’t, or what we should unpack next at corpcomm.digitlife@godigit.com.

© Go Digit Life Insurance Limited, May 2025. Go Digit Life Insurance Limited | Registered Office Address: Ananta One, Pride Hotel Lane, Narveer Tanaji Wadi, City Survey No.1579, Shivaji Nagar, Pune-411005, Maharashtra | Corporate Office Address: Atlantis, 95, 4th B Cross Road, Koramangala Industrial Layout, 5th Block, Bengaluru-560095, Karnataka | CIN: U66000PN2021PLC206995, IRDAI Registration No. 165 | "Digit Life Insurance” trademark belongs to Go Digit Life Insurance Limited (“the Company”). “Digit” logo belongs to Go Digit Solutions Private Limited and is used by the Company under sub-license from Oben Ventures LLP. This document may contain Proprietary Information of Digit Life and/or Digit Group of Companies and provided solely for information purpose for our Customers, Employees and Partners. This document shall not be used for any duplication or for commercial use. This document does not intend to create any binding or legal obligation. For details on any Products, kindly refer to the Company website www.godigit.com/life.