Life

General

Support

Resources

₹1 Crore Term Insurance Plan

Buy ₹1 Crore Term Insurance Online

I agree to the Terms & Conditions

Digit Glow Term Life Insurance

Online

Buying Process

Tax Savings

u/s 80C

Simple

Documentation

Written By

Fathima Tabasum

Fathima Tabasum

Senior Marketing Associate

Fathima defines Digit's voice in life insurance with her strong command of language. Her creative, clear writing and research skills simplify complex concepts and build trust and engagement.

Reviewed By

Ashok Manwani

Ashok Manwani

Vice President - Products

Ashok is an insurance professional with extensive experience in product development and management. In his role at Digit, he focuses on creating innovative life insurance solutions tailored to meet diverse customer needs.

What is a 1 Crore Term Insurance?

A ₹1 crore term insurance plan works as a financial safety net for your family. You pay a fixed premium for a chosen period, and if you pass away during that time, your nominee receives ₹1 crore in one lump sum.

This payout is generally tax-free under current Indian tax laws, provided policy conditions are met.

The best part? You don’t have to invest too much to afford it. A healthy 30-year-old non-smoker can get a ₹1 crore cover at a relatively affordable premium. The exact premium depends on age, health, lifestyle, and policy terms. Riders can be added for enhanced protection.

Is ₹1 Crore Term Insurance Plan Enough for You?

For most Indians earning ₹8–15 lakh per year, a ₹1 crore term insurance cover is a reasonable starting point. However, if you have large financial responsibilities, you may need higher coverage.

₹1 crore term insurance cover may be enough if:

- Your major loans are already paid off

- Your spouse is financially independent

- You have built sufficient savings and investments

A simple rule of thumb used by financial planners is that your life insurance coverage should be 10-15 times your annual income. Apart from income, you should also consider:

- Any ongoing home or car loans

- How many people depend on your income

- Whether your spouse earns or relies on you financially

- Children’s education costs, especially 10-15 years from now

- Inflation, which reduces the value of money over time

For a more accurate estimate, use a Human Life Value calculator that factors in income, expenses, liabilities, and future goals.

The examples below will help you understand whether a ₹1 crore term plan is enough in different situations.

Scenario 1: Who is ₹1 Crore Enough For?

Rohan was a 30 year old professional earning ₹15 lakh per year. He was married, had dependent parents, and already owned a family home. He bought a ₹1 crore term plan for 25 years.

Rohan passed away at the age of 40 due to an accident. At that time:

- His wife was earning

- He had no major loans

- He had a 6-year-old daughter whose education needed funding

- He had built good savings and investments

Because his liabilities were low and assets were adequate, a ₹1 crore term plan was reasonably sufficient for his family.

Scenario 2: Who May Need More Than ₹1 Crore?

Aryan was a 26 year old professional earning ₹10 lakh per year. At that time, his only dependents were his retired parents. He planned to get married and buy a house in the future, so he bought a ₹1 crore term plan for 30 years.

Unfortunately, Aryan passed away at the age of 42 due to a cardiac arrest. By then, he had:

- A dependent wife and two children

- An outstanding home loan of ₹40 lakh

- Dependent parents

- Future expenses like children’s higher education

In this case, the ₹1 crore cover was not sufficient to handle all responsibilities. Aryan should have reviewed and increased his coverage as his life responsibilities grew.

₹1 Crore vs ₹2 Crore Term Insurance

The table below compares ₹1 crore and ₹2 crore term insurance plans across coverage amount, premium cost, and suitability to help you choose the right level of protection.

The golden rule of term insurance is to review your cover every 5 years. Always reassess your life cover when major life changes happen such as marriage, childbirth, taking a home loan, or a significant income increase.

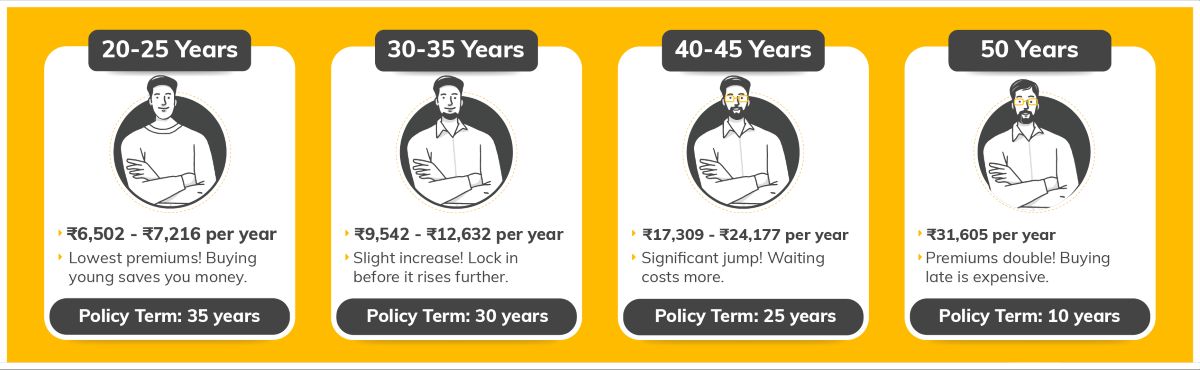

How Much Does ₹1 Crore Term Life Insurance Cost?

The cost of a ₹1 crore term life insurance plan mainly depends on the age at which you buy it. The earlier you buy, the lower your premium.

Premiums rise sharply after age 35 and again after age 45, even if you are healthy.

Here is a look at how premiums for a ₹1 crore term life insurance plan increase across different age groups, up to 70 years:

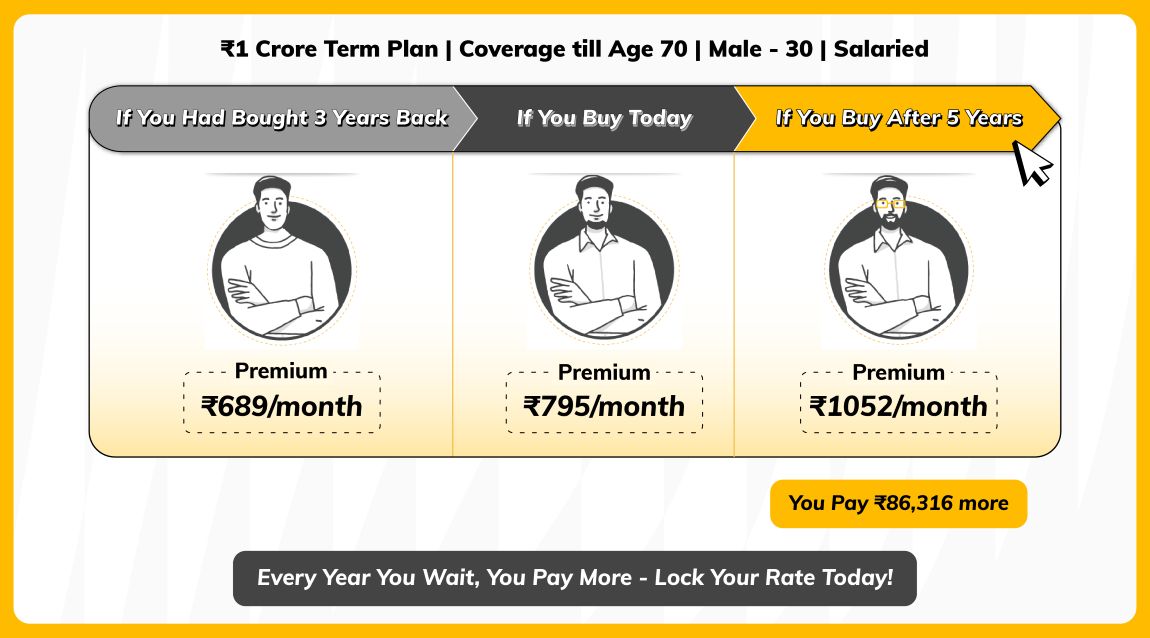

Example:

A 30-year-old salaried male can get a ₹1 Crore term plan coverage till age 70 for just ₹795/month today. If he had had the same policy three years earlier, the premium would have been ₹689/month.

However, if he waits five more years, the premium increases to ₹1,052 per month. This means paying an extra ₹86,316 over the policy term for the same ₹1 crore coverage.

So, buying term life insurance early helps you lock in lower premiums, saves money over the long run, and ensures your family is financially protected at a lower cost.

Note: The premiums shown are applicable to customers purchasing Glow Plus term insurance directly through the online portal. These are standard rates for healthy, salaried male individuals who are non-smokers and non-drinkers. Premiums may vary for direct purchase journeys and are subject to change. The final premium and eligible sum assured will depend on the outcome of the underwriting process.

Who Should Buy a 1 Crore Term Insurance Plan?

Young Earners

Youngsters who have just started earning and are responsible for dependents should consider a 1 Crore term plan to provide a substantial financial cushion for their loved ones in the event of their demise.

Married Couples

When you get married, there are increased responsibilities. Even with a working spouse, loss of income can disrupt finances significantly. In such a case, a term plan ensures that your spouse does not struggle with finances, even in your absence.

Individuals with Home Loans

If you have taken a home loan and are paying off the EMIs, that loan can burden your family in case of your unfortunate demise. These days, in any city, a decent home costs at least 1 Crore. Hence, make sure to buy a Term Plan for 1 crore dedicated to safeguarding your home.

Small Business Owners

If you are into business, most of the expenses are on credit, and at any given time, you might find yourself under a certain debt. If it is a small business, 1 Crore Term Insurance plan might suffice to take care of these debts in case of your untimely demise and make sure that your family does not have to deal with this pressure of debts at a time when they are dealing with a personal loss.

Individuals with Dependent Parents

In cases where parents do not receive a pension and are dependent on their sole earning child, Term Plan should be purchased as it would save the parents from any financial turmoil in case of any unfortunate death of their earning child. The insurance cover would take care of their liabilities and regular expenses.

Individuals with Education Loans

If you have taken out an education loan, your family may face the challenge of repaying it if something happens to you unexpectedly. A term insurance policy of 1 crore can offer significant protection, assisting in settling the remaining education loan and easing your family's financial burden.

Does Gender Affects ₹1 Crore Term Insurance Premiums?

How Smoking Impacts ₹1 Crore Term Insurance Premiums?

What Does Digit Life ₹1 Crore Term Insurance Cover?

1. Death Benefit

If you pass away during the policy term, your nominee receives ₹1 crore. This applies whether death is caused by an illness, accident, or natural reasons.

2. Terminal Illness Benefit (Plan-specific)

If you are diagnosed with a terminal illness (such as advanced stage cancer) while the policy is active, a terminal illness rider pays a part of the sum assured to you in advance. This money can be used for treatment, care, or family needs.

3. Optional Riders

- Accidental Death Benefit: If you opt for an accidental death benefit rider, your family gets an extra payout over and above the ₹1 crore cover in case the death is due to an accident. Usually available at a low additional premium, often just a small fraction of the base term plan cost.

- Accidental Total & Permanent Disability Rider: If an accident leaves you permanently disabled and unable to work, a lump sum amount is paid. In many cases, future premiums are also waived, while your life cover continues. Slightly higher than an accidental death rider, but still much more affordable than buying a separate disability policy.

What is Not Covered in Digit Life ₹1 Crore Term Insurance Plan?

Digit Term Life insurance does not cover the following:

- Suicide within the first 12 months of policy commencement

- Death caused by drugs, alcohol, or substance abuse if it was not declared while buying

- Death during criminal or illegal activities

- Non accidental self-inflicted injuries

- Pre-existing illnesses that were not disclosed at the time of purchase

- High-risk activities not disclosed at proposal stage

- War related events or acts of terrorism

Note: Exclusions are governed by IRDAI norms and specific policy terms. Always refer to the policy document.

How to Calculate the Right Term Insurance Cover?

Choosing the right term insurance cover is just as important as choosing the policy itself. If the cover is too low, it may not meet your family’s needs. If it’s too high, you may end up paying unnecessary premiums. Below are three reliable ways to calculate the right cover amount.

Best Practice: Use the rule of thumb as a starting point, then validate it using a calculator or HLV method for accuracy.

Eligibility Criteria for a 1 Crore Term Insurance

Documents Required to Buy a 1 Crore Term Insurance Plan

To purchase a term insurance plan, applicants are required to submit the documents listed below:

Identity & Address Proof

- Aadhaar Card

- Passport

- Voter ID

- Driving License

- PAN Card

Income Proof

- Salary slips (last 3 months)

- IT returns (last 3 years)

- Form 16

- Bank statements (last 6 months)

- Profit & Loss account (for self-employed)

- Balance sheet

- Salary certificate

- CA certificate (for self-employed)

- Agricultural income certificate

Age Proof

- Birth Certificate

- School/College Leaving Certificate

- Passport

- Aadhar Card

Medical

Other Documents

- Policy Proposal Form

- Nominee Details

- Photograph

- Bank Account Details

How to Buy Digit Term Insurance Policy Online?

The five easy steps to buy term life insurance plans are as follows:

Visit Digit Website/App

Visit the official Digit Life Insurance website or app and compare the types of life insurance policy options and fill in your personal information.

Coverage & Payment

Now it’s time to choose your ideal coverage, premium payment methods, and any additional benefits you want!

Payment & KYC

Complete your payment, and then finish the KYC process and fill in your nominee details.

Access Documents

Congratulations! Your policy documents will be sent to your email and WhatsApp. You can also access it 24/7 on the Digit App.

Why Choose Digit Life with Your Family’s Security?

Digit Life Insurance is an IRDAI registered life insurer offering term insurance policies through a digital first process. All policy features, benefits, exclusions, and conditions are defined in the policy document.

- Clear Policy Terms: Coverage, exclusions, and payout conditions are stated upfront in policy wording. Benefits are payable only as specified in the policy. Customers are advised to review the terms carefully before purchasing.

- Digital Purchase & Servicing: Policy purchase, document access, and claim initiation can be done online. Most standard processes do not require physical paperwork. Customer support is available when needed.

- Claims Supported Worldwide: If the policyholder passes away outside India, the nominee can initiate the claim online. This applies to cases such as overseas travel, temporary stays, or residence abroad, subject to policy conditions and verification requirements.*

- Eligibility for NRIs: Indian citizens residing abroad may apply for coverage, subject to underwriting norms. Premiums can typically be paid through NRE/NRO accounts. Policy validity and coverage apply as per the geographical conditions mentioned in the policy document.

How to File Term Insurance Claim with Digit Life?

Filing a term insurance claim can feel stressful during an emotional period. At Digit Life, we have kept the process simple so your family can receive financial support without delays. Here’s how it works:

- Inform Digit Life Immediately: Notify us about the occurrence of the claim event as soon as possible. You can do this by contacting the helpline at 1800-296-2626 or emailing lifeclaims@godigit.com.

- Submit Required Documents: Provide necessary documents such as the death certificate, policy document, valid ID proof of the nominee and claim form duly filled and signed.

- Receive Claim Acknowledgement: Once the documents are received, Digit Life generates an acknowledgement or ticket number. This helps you track the status of the claim.

- Claim Assessment and Payout: Digit Life reviews the documents and verifies the claim. If everything is in order, the claim is approved, and the payout is transferred directly to the nominee’s bank account. Updates are shared via SMS, email, or the Digit app, so the family stays informed at every step.

Tax Benefits for ₹1 Crore Term Insurance Policies

Your term insurance premium saves you tax in two ways:

1. Section 80C: Premium Payments

The annual premium you pay towards your term plan is eligible for deduction up to 1.5 lakh per year under Section 80C of the Income Tax Act.

Example: If you pay 8,000 per year as premium, your taxable income reduces by 8,000. At a 30% tax bracket, you save 2,400 in taxes.

Who Can Qualify?

If your policy was issued on or after April 1, 2012, your premium should not be more than 10% of the sum assured. The premium should not exceed 20% of the sum assured for policies issued before that date.

2. Section 10(10D): Death Benefit

The entire 1 crore that your family receives as a death benefit is 100% tax-free. They don’t pay a single rupee in income tax on it.

- Conditions: For policies issued on or after April 1, 2012, the premium must not exceed 10% of the sum assured. The premium must not exceed 20% of the sum assured for older policies.

- TDS: If your policy doesn’t meet these conditions, a 5% tax will be deducted at the source if the payout exceeds 1 lakh in a financial year.

FAQs about 1 Crore Term Insurance Plan

What is the minimum age to buy a ₹1 crore term insurance?

Can I get ₹1 crore term insurance without a medical test?

How much does a ₹1 crore term insurance cost per month?

What happens if I survive the full term of the policy?

In a standard term insurance plan, you do not receive any money if you survive the policy term. This is what makes term plans very affordable.

If you choose a term insurance plan with return of premium, the total premium you paid is refunded at maturity. These plans cost more than regular term plans but offer added peace of mind to some buyers.

Can my family claim ₹1 crore term insurance if I die abroad?

Can I increase my ₹1 crore cover later in life?

What happens if I never review my ₹1 crore term insurance cover?

What if I hide smoking or any health details while buying the ₹1 crore term plan?

What happens if I ignore inflation while calculating ₹1 crore term cover?

What if I miss paying premium for my ₹1 crore term plan?

Should I buy ₹1 Crore because it’s popular?

What is the minimum income requirement to purchase term insurance of ₹1 crore?

What are the eligibility criteria for buying the best term insurance plan for ₹1 crore?

Should I buy a 1 crore term insurance plan or an endowment plan?

When should I buy the best term insurance plan for 1 crore?

How do I buy a 1 crore term insurance plan online?

What are the riders benefits available on a 1 crore term insurance plan?

How do insurers assess the risk profile for individuals seeking a 1 crore term insurance plan?

How does the Human Life Value (HLV) concept influence the decision to opt for a 1 crore term insurance plan?

What are the key factors when comparing different 1 crore term insurance plans?

Should I buy health insurance or term insurance?

Both. You should have both health insurance and term insurance for comprehensive financial protection. Term insurance protects your family after you, while health insurance protects you and your family while you're alive.

However, if your goal is to protect your family’s financial future in case something happens to you, then term insurance is essential. And if your concern is managing medical expenses during your lifetime, such as hospital bills, surgeries, or treatments, then health insurance is what you need.

Other Important Articles Related to Term Insurance

Renew & Download Policy Document, Check Challan, Credit Score, PUC & more

Anytime, Anywhere. Only on Digit App!

Rated App

Rated App

Scan to Download

![]()

IRDA Licensed Life Insurance Company in India - IRDAI Reg. No. 165

Sign-In to Digit Insurance

We have this phone number linked with the email ID in our database. Please login through OTP using this number or logout using below option and login again using new details.

Logout your email login