Life

General

Support

Resources

Term Insurance Calculator

Calculate Term Insurance Premium Instantly

I agree to the Terms & Conditions

Digit Glow Term Life Insurance

What Does the Term Insurance Calculator Estimate?

A term insurance calculator gives two estimates, based on the details you enter:

- The amount your family may need if your income stops unexpectedly.

- An approximate premium range for that cover, based on age, lifestyle, and risk.

A calculator helps you avoid being underinsured, where the coverage is not enough for your family, and overinsured, where you pay more premiums than required. These estimates help you plan, but they do not replace underwriting, medical tests or document verification.

How is Term Insurance Cover Calculated?

A good calculator does not use a flat income multiple. It looks at your actual financial responsibilities, such as:

Simple Rule of Thumb: If your income stopped today, how many years could your family maintain the same lifestyle?

That number × annual household expenses = a starting point for cover.

How Does the Term Insurance Premium Calculator Work?

A term insurance premium calculator works by using your basic personal details to estimate how much premium you may need to pay for life insurance, and how much money your family would need if your income stopped tomorrow.

You enter a few basic details, such as:

- Age and gender

- Annual income

- Smoking or tobacco use

- Occupation

- Desired cover amount

- Policy duration

Based on these inputs, the calculator instantly shows an estimated premium range. This estimate helps you understand the cost of coverage before you apply. The final premium is confirmed only after the insurer verifies your full health and job details, and may change if additional risk is found.

Note: The calculator uses basic inputs. Detailed health and risk evaluation happens after you apply, during underwriting.

How Accurate is Digit Term Insurance Calculator?

Digit’s Term Insurance Calculator helps you estimate premiums instantly, compare coverage options, and choose the right policy based on your needs before buying. The key reasons to use it:

- Instant Premium Estimate: Get an upfront idea of how much you may need to pay based on your age, income, lifestyle, and coverage needs.

- Helps Choose the Right Cover: Adjust the life cover and policy term to see how changes affect your premium and pick what fits your family’s needs.

- Simple and Easy to Use: No paperwork or technical knowledge required, just enter basic details and get results in seconds.

- Better Decision Making Before Purchase: Understand the cost first, then proceed confidently with KYC and payment.

Why Does Digit Life Offer Two Term Insurance Plans?

Digit Life offers two variants not to complicate choice, but to separate two very different income realities:

How to Use Digit Term Insurance Calculator?

Purchasing a term life insurance policy online is made simple with Digit Life. Here is what you need to do to obtain your policy coverage online:

Go to Digit Website/App

Visit the Digit Life Insurance website or application, explore and compare term insurance plans.

Enter Personal Information

Provide income, age, lifestyle habits, and other basic details to get an estimate.

Select Coverage & Benefits

Select life cover amount, policy term, payment option, how you want to pay the premium, and riders (if needed).

Make Payment & Complete KYC

Pay online and submit KYC documents and information related to the nominee details.

Policy Approval and Document Delivery

Once your policy is approved, policy documents will be shared via email and WhatsApp.

Illustration on How to Choose the Right Sum Assured

Ajay, a 28-year-old salaried professional, wants to secure his family’s future with a ₹25 lakh home loan. To understand how much life cover he needs, he uses a term insurance premium calculator.

He compares two coverage options, ₹1 crore and ₹2 crore, to see how different coverage amounts affect the premium and the financial protection offered to his family. This comparison helps Ajay see whether the chosen sum assured is sufficient to cover the home loan, daily expenses, and long-term family needs, even in his absence.

Based on this comparison, Ajay chooses the ₹2 crore cover for better financial protection, knowing that term insurance is meant for protection and not returns.

Disclaimer: The premium amounts shown are approximate and for illustrative purposes only. Actual premiums may vary based on insurer underwriting, lifestyle, and selected policy features.

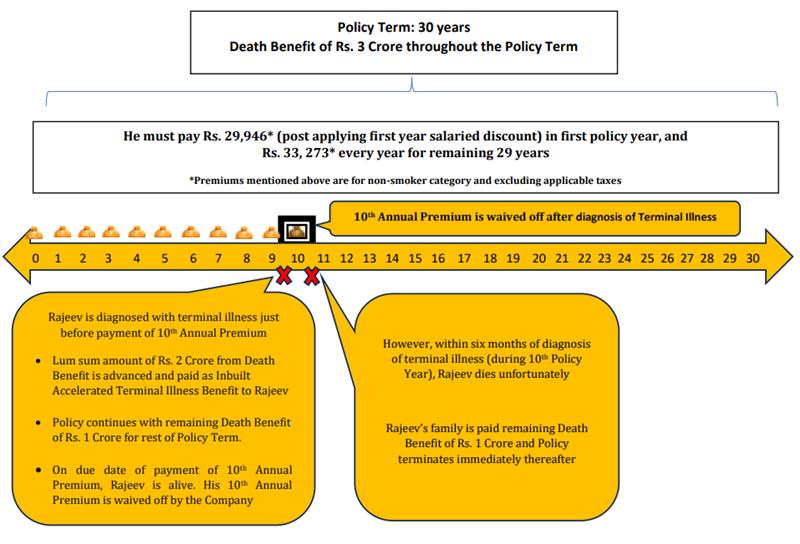

Illustration for Term Insurance

Why Choosing the Right Sum Assured is Highly Important?

As healthcare costs increase and lifestyle-related health issues change, planning for your financial future becomes crucial. One way to do this is by selecting the appropriate sum assured for a term life insurance plan because:

- Ensures your family receives sufficient funds to maintain their standard of living.

- It covers outstanding debts, such as loans, to prevent financial burdens on your family.

- It helps achieve specific goals, like children's education or marriage expenses.

- Replace your income to support your family's financial needs.

When considering this investment, consider your remaining working years. For instance, if you are 35 and plan to retire at 60, you have 25 years of income ahead. This timeframe impacts coverage and premium choices for your insurance. Existing term plan holders can explore options to increase their sum assured as they progress through different life stages, aligning their policy with changing financial responsibilities.

How Riders Help When Your Cover Feels Low?

If increasing the full cover can push the premium up sharply, riders can help cover specific risks at a lower additional cost. Common riders you can consider:

Note: Costs are indicative. Actual rider premiums depend on age, cover amount, and insurer rules. Also riders do not replace life cover, they only fill targeted gaps.

What Happens if You Don't Use a Term Insurance Premium Calculator?

Without comparing options, you may choose a premium higher than required for your age, income, and lifestyle.

- Overpaying for Insurance: Without using the calculator, you might pay more than necessary for your insurance. Not knowing the exact amount that fits your needs and budget could lead to overpaying.

- Insufficient Life Cover: You might choose a sum assured that does not fully cover loans, living expenses, or your family’s future needs.

- Financial Stress: Without knowing the estimated premium in advance, it becomes harder to plan payments confidently over the long term. Using a calculator helps align coverage, premium, and affordability before you apply for a policy.

A term insurance calculator helps you estimate the right life cover and expected premium by considering income, loans, dependents, and future goals. It gives clarity before you apply, helping you make a more confident decision.

Use the Digit Term Insurance Calculator to compare options and choose suitable protection for your family.

FAQs about Term Insurance Calculator

What is a term insurance calculator?

Do term insurance premium rates increase over time?

What should I do after using a term insurance calculator?

Is a term insurance calculator free to use in India?

Why should I use a term insurance calculator before buying a policy?

What details are required to use a term insurance calculator?

Does a term insurance calculator show the exact premium?

Can I use a term insurance calculator to compare multiple plans?

Does location affect term insurance calculator results?

Is a term insurance calculator accurate for self-employed individuals?

Can I buy term insurance directly after using the calculator?

Does the premium amount change if I add riders to my term plan?

Can I increase or decrease the sum assured during the policy term?

How does my age affect my term insurance premium calculation?

Why does occupation impact term insurance premium calculation?

Can I buy a term insurance plan if I already have a life insurance policy?

What are the online term insurance premium payment options?

How is the term plan premium calculated?

What is the minimum salary for 1 crore term insurance?

Can I use a term insurance calculator while renewing my term plan?

Other Important Articles Related to Term Insurance

Renew & Download Policy Document, Check Challan, Credit Score, PUC & more

Anytime, Anywhere. Only on Digit App!

Rated App

Rated App

Scan to Download

![]()

IRDA Licensed Life Insurance Company in India - IRDAI Reg. No. 165

Sign-In to Digit Insurance

We have this phone number linked with the email ID in our database. Please login through OTP using this number or logout using below option and login again using new details.

Logout your email login