Life

General

Support

Resources

Term Insurance Age Limit in India

In India, you can buy term insurance between age 18 and 65. The minimum age is 18 and the maximum entry age is 65 for most of the plans. Your coverage can continue until age 85, depending on the plan you choose.

Whether you are in your 20s planning ahead, in your 30s with family responsibilities, or in your 40s wondering if it’s too late to buy, this will help you choose the right term plan based on your age.

I agree to the Terms & Conditions

Digit Glow Term Life Insurance

How Does Your Age Affect Term Insurance Premium?

Age is a critical factor when it comes to purchasing term insurance. It influences various aspects of the policy, including:

Eligibility

Insurers set minimum and maximum age limits for purchasing term insurance.

Premium Amount

Premium calculations are directly linked to age; younger individuals are charged lower premiums as they are considered low risks.

Policy Tenure

The policy term you can choose depends on your age at the time of purchase.

Impact on Premium Rates

Each year of delay in buying term insurance increases the premium amount, and the premium difference can sometimes be 2 to 3 times higher for older people.

Health Conditions

As you age, health conditions develop, which can further increase premiums. Some applications might be rejected due to age-related health concerns.

Table of Contents

What are the Minimum and Maximum Age Limits for Term Insurance?

1. Minimum Age to Buy Term Insurance

The minimum age to purchase term insurance is typically 18 years. Individuals are legally considered adults and can enter into financial contracts at this age. Buying term insurance at a young age can be beneficial because:

- Premiums are lower due to a lower risk of health issues.

- It allows individuals to secure their future financial responsibilities early on.

- Some insurers might offer special policies starting at age 16 with parental consent.

Note: Young adults often overlook term insurance, but it's the best time to buy it.

2. Maximum Entry Age for Term Insurance

The maximum entry age for term insurance generally ranges between 60 and 65 years, depending on the insurer. However, some insurance providers may extend this limit to 70 years or even higher for specific plans. Here is what you need to know:

- Most standard term plans accept new policyholders up to age 65.

- Some specialised senior citizen plans might allow entry up to age 70.

- Premium costs increase significantly for older applicants.

- Medical examinations become more stringent as the entry age increases.

- Coverage options might be limited for those buying at higher ages.

3. Maximum Exit Age in Term Insurance

The exit age, or maturity age, is when your term insurance coverage ends. This is an important consideration when choosing a policy:

- Traditional term plans usually extend coverage up to age 70 to 75 years.

- Some modern plans extend coverage up to age 80 or even 85.

- Whole life term plans might offer coverage up to age 99 or 100.

- The longer the coverage period, the higher the premium will be.

- Exit age should align with your financial planning goals.

What is the Right Age to Invest in Term Insurance?

Reasons for Buying Term Insurance Plan in the 20s

While individuals are in their 20s, they may have student loans or familial responsibilities. They may also have to support the livelihoods of their dependents. If they are covered under a term insurance plan, they can ensure that their families do not face financial difficulties during any unforeseen events. So opt for a long-term plan of 30-40 years and choose coverage that is higher to accommodate future financial responsibilities.Reasons for Buying Term Insurance Plan in the 30s

People in their 30s have more responsibilities towards their families. They must consider the well-being of their spouses, children, parents or other dependents. Children’s education is also one of the major concerns at this age.

By staying covered under a term insurance plan for 30 - 40 years, they can get an assurance that their families can sustain their lives and manage impending expenses. Moreover, if they have any personal, home or car loan, their families can easily close it with the sum assured amount, so keep reviewing your plan based on the expenses and life changes.

Reasons for Buying Term Insurance Plan in the 40s

Getting term insurance in your 40s helps you manage important financial responsibilities like your children's education, their weddings, and any medical emergencies for your ageing parents.

Consider mid-term plans of 20-30 years and adjust coverage to include existing liabilities to ensure your family won't be burdened with debts if something happens to you. While insurance companies charge higher premiums at this age due to increased health risks, you can still find affordable options if you are in good health.

Reasons for Buying Term Insurance Plans in the 50s and 60s

Once you turn 50 or 60, the cost of term insurance premiums increases significantly. However, it's still a good idea to get the best term insurance plan available for someone your age. As long as you are within the maximum age limit for term insurance, you can get coverage.

Focus on shorter-term plans of 10 - 20 years and prioritise a health insurance plan or add-ons like critical illness coverage. The life cover you choose will help your family pay off any debts you might leave behind. It can also provide financial support if you face critical illnesses during the policy period.

How Much Does Delaying Term Insurance Actually Cost?

Even a small delay in buying term insurance can increase your total premium outgo over the long term.

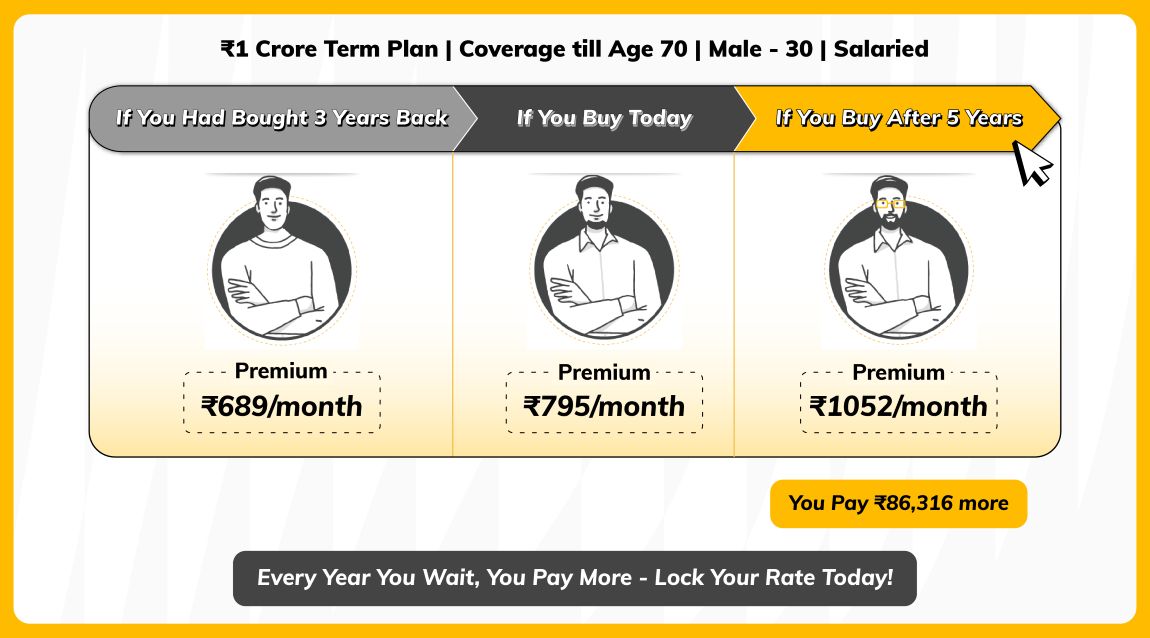

For example, a ₹1 crore term life insurance plan at age 30 may get coverage around ₹795/month. At age 35 the same coverage may cost around ₹1,052/month.

Over a typical 25-30 year policy term, even this difference of ₹200-₹300 per month can add up to a significantly higher total cost. Premiums don’t increase evenly with age. They usually rise gradually until the mid 30s, and then increase more sharply after 40 due to higher risk assessment by insurers.

Disclaimer: Indicative premiums for a healthy non-smoker; actual premiums vary based on insurer, health, lifestyle, sum assured, policy term, and underwriting.

How Much Term Insurance Cover Do You Need at Different Ages?

Cover is typically calculated as income replacement, depending on age, liabilities, and dependents. Use this table to quickly understand the right move for your stage of life.

How to Compare Term Insurance Plans Based on Your Age?

Don’t compare plans randomly; follow a clear order so you don’t pick the wrong policy for your age and needs. When you are comparing term insurance plans, look at these things in the right sequence:

1. Check if Your Age is Eligible

See if the insurer accepts your current age as the entry age. Not all plans allow entry at higher ages, especially after 60.

2. Look at Coverage Maturity Age

Different plans offer different end ages, like 75, 80, or 85 years. Higher coverage age means longer protection, but it also costs more. Pick what matches your financial responsibilities timeline.

3. Check Claim Settlement Record

Look at the insurer’s claim settlement ratio (CSR) for the last 3 years. Aim for 97% or higher; this shows how reliable the insurer is in paying claims.

4. Compare Premium for Your Required Cover

Don’t get influenced by what the insurer suggests. Your cover amount should depend on your income, loans or liabilities, and family dependents. Then compare the premium for that specific cover.

What to Do If You Miss the Age Limit for Term Insurance?

If you miss the age limit for term insurance, consider the following alternatives:

1. Whole Life Insurance

Whole Life Insurance provides coverage for your entire life with a savings component.

2. Guaranteed Issue Plans

These plans do not require medical tests and often cater to older individuals.

3. Senior Citizen Plan

Annuity plan tailored for individuals above 60, offering suitable coverage and benefits.

FAQs about Term Insurance Entry Age Limit

Will my premium amount of a term life insurance plan increase with age?

What is the minimum age to buy term insurance?

What is the maximum age limit for term insurance?

Can I buy term insurance at 50?

Does age affect term insurance premiums?

Can I extend my term insurance after the policy term ends?

Can I buy multiple-term policies at different ages?

Can I buy term insurance for a parent who is 58 years old?

Other Important Articles Related to Term Insurance

Renew & Download Policy Document, Check Challan, Credit Score, PUC & more

Anytime, Anywhere. Only on Digit App!

Rated App

Rated App

Scan to Download

![]()

IRDA Licensed Life Insurance Company in India - IRDAI Reg. No. 165

Sign-In to Digit Insurance

We have this phone number linked with the email ID in our database. Please login through OTP using this number or logout using below option and login again using new details.

Logout your email login