Life

General

Support

Resources

Why Buying Term Insurance Early is a Smart Decision?

Buying term insurance early can help you lock in lower premiums and simplify underwriting. But buying early does not mean buying blindly or buying more than you need.

The smarter approach is simple: Buy early, but buy the right amount for your current life stage. Increase coverage as responsibilities grow. That balance keeps the decision practical, affordable, and trustworthy.

I agree to the Terms & Conditions

Digit Glow Term Life Insurance

Why are Term Insurance Premiums Lower in Younger Ages?

Term insurance premiums are primarily based on your age and health at the time of purchase. Younger applicants usually benefit because:

- Lower mortality risk

- Fewer health conditions

- Simpler underwriting

- Lower insurer risk

Most term plans follow a level premium structure, meaning once your policy is issued, the premium stays the same for the entire term. Your age and health profile on day one is what you lock in for the next 20-30 years.

Note: Premiums can be significantly lower when bought early, depending on age, health, cover amount, policy term, and insurer pricing.

Table of Contents

Why Do Term Insurance Premiums Increase with Age?

As age increases, insurers see higher mortality risk. This can lead to:

- Higher premiums

- Stricter medical underwriting

- Possible exclusions or premium loading

- Reduced eligibility for higher cover amounts

Common health conditions like diabetes, high blood pressure, thyroid issues, or previous surgeries, which are rare in your 20s, often attract stricter underwriting in your late 30s and 40s.

This does not mean older buyers shouldn’t buy term insurance. It simply means cost and complexity increase over time.

Should You Buy Term Insurance Early & How Much Coverage to Start With?

The right time to buy term insurance depends on your current financial responsibilities and how soon they are likely to increase. Buying early makes sense if:

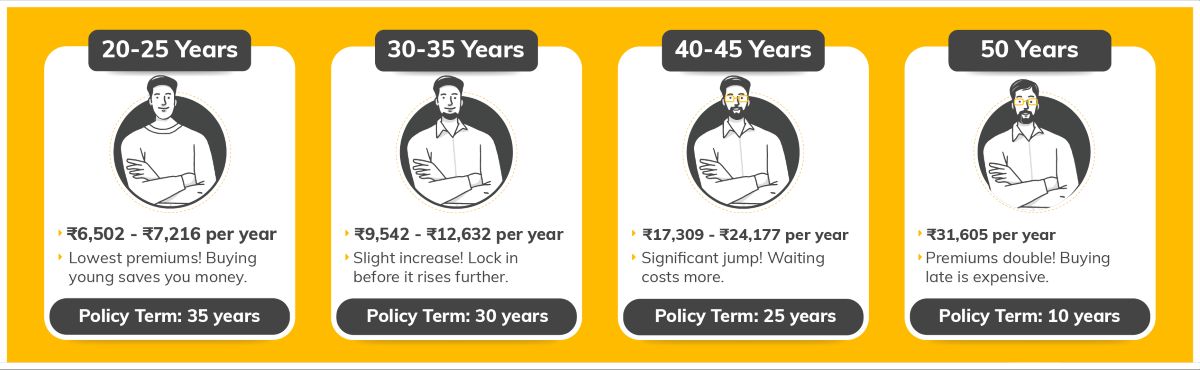

- You have financial dependents: Income replacement becomes critical if something happens to you. Consider 10-15× your annual income plus existing liabilities.

- Married/planning home loan: Buying early helps lock in lower premiums before responsibilities and risk increase. Coverage should include spouse income support and outstanding loan amounts.

- You have children: Add education costs, daily living expenses, and long term family needs into your cover planning.

If you are early in your career with no dependents, you can start with a moderate base cover, depending on affordability, job stability, and family dependency. Coverage can be increased later as income and responsibilities grow.

The goal is not to finalise your lifetime cover early. The goal is to start protection at the right level and build it gradually.

How Much Term Insurance Do You Need at Different Life Stages?

This approach keeps coverage relevant, affordable, and aligned with real responsibility.

What Happens When You Buy Term Insurance Early vs Late?

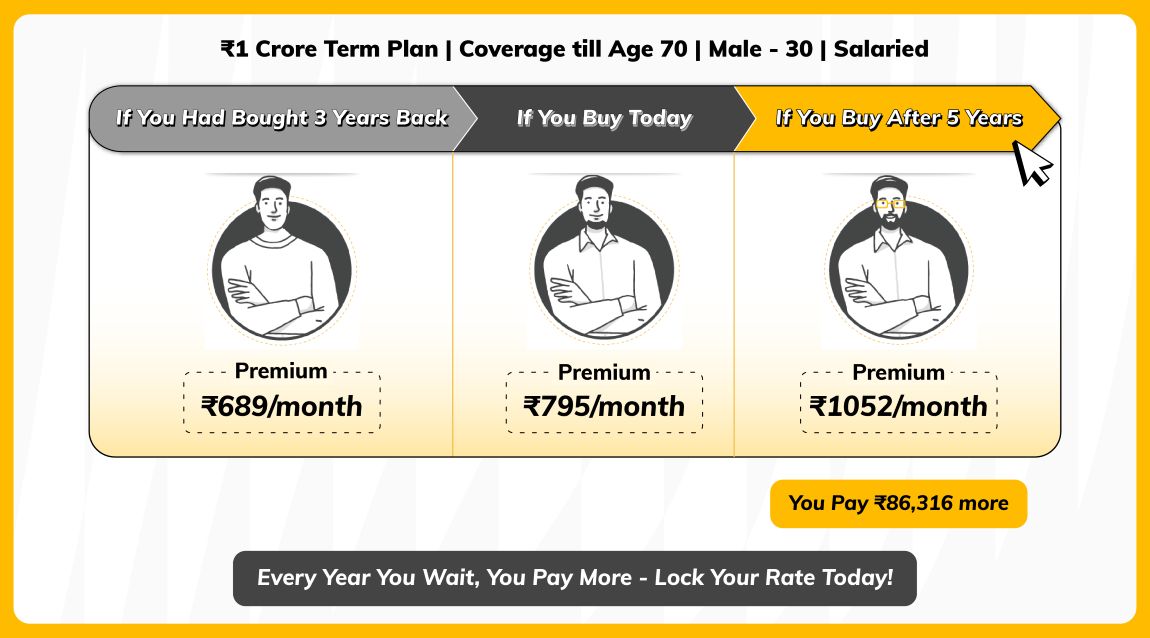

How Much Does Waiting Actually Cost Your Term Insurance?

Even a modest delay can increase overall premium outgo significantly over a long policy term.

For example, a ₹1 crore term life insurance premium rises sharply after age 35 and again after age 45, even if you are healthy. Here is a look at how premiums for a ₹1 crore term life insurance plan increase across different age groups, up to 70 years:

- A 30-year-old may get ₹1 crore coverage for ~₹795/month

- At age 35, the same coverage may cost ~₹1,052/month

This results in approximately ₹86,000+ additional outflow over the policy term.

Advantages of Buying Term Insurance Early

At some point, term insurance becomes very important in an individual's life. Hence, it is better if somebody starts early. The following portion highlights some of the benefits of buying term insurance at an early age:

Longer Protection Duration

Starting early allows you to choose longer cover durations, often till age 75 or 80, depending on the insurer. Someone buying at 25 can secure coverage for 40–50 years, while buying at 45 may limit coverage length.

Lower Premiums for Life

Once issued, most term plans follow a level premium structure, meaning the premium generally remains unchanged for the entire policy term. Buying early locks in the lowest possible rate.

Reduced Rejection Rates

Pre-existing illness is a major reason for term insurance rejection. Hence, people are generally free of any serious medical condition at a young age, increasing the chance of getting their term insurance application approved.

Better Access to Riders

Riders like accidental death benefit, waiver of premium, or critical illness cover are easier to get at younger ages and better health profiles.

Less Dependency on Employer Term Insurance

Employer provided term cover is often too small and is tied to your job which ends when you switch or leave. A personal term plan moves with you across jobs offering higher coverage.

Lower Risk of Exclusions or Rejection

Early purchase generally means a cleaner medical history, leading to fewer exclusions and smoother claim processing later.

Tax Benefits Over a Longer Period

Term insurance provides financial security and offers some tax benefits under Section 80C of the Income Tax Act of 1961. Under this, the amount spent on premiums is subtracted from your taxable income, and the limit is ₹1.5 lakhs.

Do Women Get Lower Premiums for Buying Term Insurance Early?

How Buying Term Insurance Early Improves Claim Experience?

Buying early indirectly improves future claim outcomes in several ways:

- Cleaner Disclosure History: Younger applicants usually have fewer medical conditions, reducing the risk of non-disclosure disputes at claim time.

- Lower Chances of Exclusions: Early purchase often results in policies with minimal or no health related exclusions.

- Simpler Underwriting Trail: Policies issued with straightforward underwriting are easier to assess during claims.

- Stable Policy Continuity: Long held policies with consistent premium payments face fewer claim complexities.

Common Mistakes to Avoid When Buying Term Insurance Early

Buying early is smart. But buying wrongly early cancels out all the benefits. Here are the most common mistakes to watch out for:

1. Buying Insufficient Cover

Buying early but opting for a low sum assured may leave your future financial needs under protected. Use the 10-15x income rule as a minimum, and factor in your outstanding loans and anticipated future responsibilities.

2. Choosing too Short Term

People choose a 20-year term at age 25, meaning their cover ends at 45, right when life's biggest financial responsibilities are likely still active. Opt for a term that covers you at least until 60-65, if not longer.

3. Not Disclosing Health History

Even if you're young, be completely transparent about any health conditions, family medical history, or lifestyle habits like smoking. Non-disclosure can lead to claim rejection when your family needs the most money. Honesty at the time of application is essential.

4. Ignoring Claim Settlement Ratio

Before choosing a provider, check their Claim Settlement Ratio (CSR), it should ideally be 97% or above. A policy from a reputed insurer with a high CSR gives you confidence that your family won't face unnecessary hassle at the time of claim.

5. Letting the Policy Lapse

Buying early means nothing if you stop paying premiums midway. Set up auto-debit from the day you buy. A lapsed policy means zero protection, and reinstating it may require fresh medical tests at an older age.

Tax Benefits of Buying Term Insurance at a Young Age

Tax Benefits under different sections of the Income Tax Act are:

1. Benefits Under Section 80C

Term insurance premiums are eligible for deduction within the overall ₹1.5 lakh limit, subject to conditions.

2. Benefits Under Section 80D

Premiums for critical illness riders may qualify separately, subject to limits.

3. Benefits Under Section 10(10D)

Death benefit paid to nominees is generally tax free, subject to policy conditions.

FAQs about Buying Term Insurance at a Young Age

What is the best age to buy term insurance?

Why is term insurance cheaper when bought early?

Should you buy term insurance early if you have no dependents?

How much term insurance coverage should I buy?

A widely used rule of thumb is 10-15 times your annual income. Add to this any outstanding loans and an estimate of your family's future needs.

For example, if you earn ₹10 lakh per year and have a ₹40 lakh home loan, a minimum cover of ₹1.4 crore is a reasonable starting point.

Is term insurance worth buying if I'm already 40?

How do premiums change based on age when purchasing term insurance?

What are the long-term financial benefits of buying term insurance early?

How does purchasing term insurance early protect my dependents?

What health factors should I consider when deciding to buy term insurance?

The following medical tests are to be taken before buying term insurance:

- Liver Function Test

- Blood Sugar Test

- HIV Test

- USG

- BMI Test

- Urine Test

- Complete Blood Count

- Kidney Function Test

Are there any tax benefits associated with buying term insurance early?

What flexibility does early-term insurance offer in future financial planning?

How can I evaluate if I need term insurance at a young age?

How does term insurance complement health insurance?

Does premium increase every year in term insurance?

Is term insurance cheaper at 25 than at 35?

If I buy early, can the insurer increase premium later due to new illness?

Can my term insurance application be rejected?

Other Important Articles Related to Term Insurance

Renew & Download Policy Document, Check Challan, Credit Score, PUC & more

Anytime, Anywhere. Only on Digit App!

Rated App

Rated App

Scan to Download

![]()

IRDA Licensed Life Insurance Company in India - IRDAI Reg. No. 165

Sign-In to Digit Insurance

We have this phone number linked with the email ID in our database. Please login through OTP using this number or logout using below option and login again using new details.

Logout your email login