General

Life

Accessibility Options

General

General Products

Simple & Transparent! Policies that match all your insurance needs.

Scan to download

Life

Life Products

Digit Life is here! To help you save & secure your loved ones' future in the most simplified way.

Scan to download

Claims

Claims

We'll be there! Whenever and however you'll need us.

Scan to download

General

General

Life

Life

Renewals

Resources

Resources

All the more reasons to feel the Digit simplicity in your life!

Scan to download

Our WhatsApp number cannot be used for calls. This is a chat only number.

The PM SVANidhi Yojana is a government program that provides financial assistance to street vendors to help them grow their businesses. This article will explain how the scheme works, its key benefits, and how it supports vendors in improving their livelihoods.

The Scheme is available for beneficiaries belonging to only those States/UTs which have notified Rules and Scheme under the Street Vendors (Protection of Livelihood and Regulation of Street Vending) Act, 2014. Learn your eligibility for this scheme and how to apply for it.

Table of Contents

The PM Street Vendor’s Atma Nirbhar Nidhi (SVANidhi) scheme was launched on 1st June 2020 amidst the COVID-19 pandemic to support street vendors, hawkers, and thelewala, financially. This financial support comes in the form of collateral-free loans of ₹10,000 at low-interest rates for a duration of one year.

Therefore, individuals can accumulate working capital and sustain their businesses with the help of this credit.

The successive lockdowns in India because of the pandemic has adversely affected the livelihood of street vendors. Considering this, the Ministry of Housing and Urban Affairs launched a PM SVANidhi scheme offering holistic development and economic upliftment for hawkers and street vendors.

Here are some features of this scheme -

Along with these features, the PM SVANidhi Yojana comes with the following objectives:

Apart from knowing the features and objectives, individuals might also consider learning about the PM SVANidhi Yojana online application and its details.

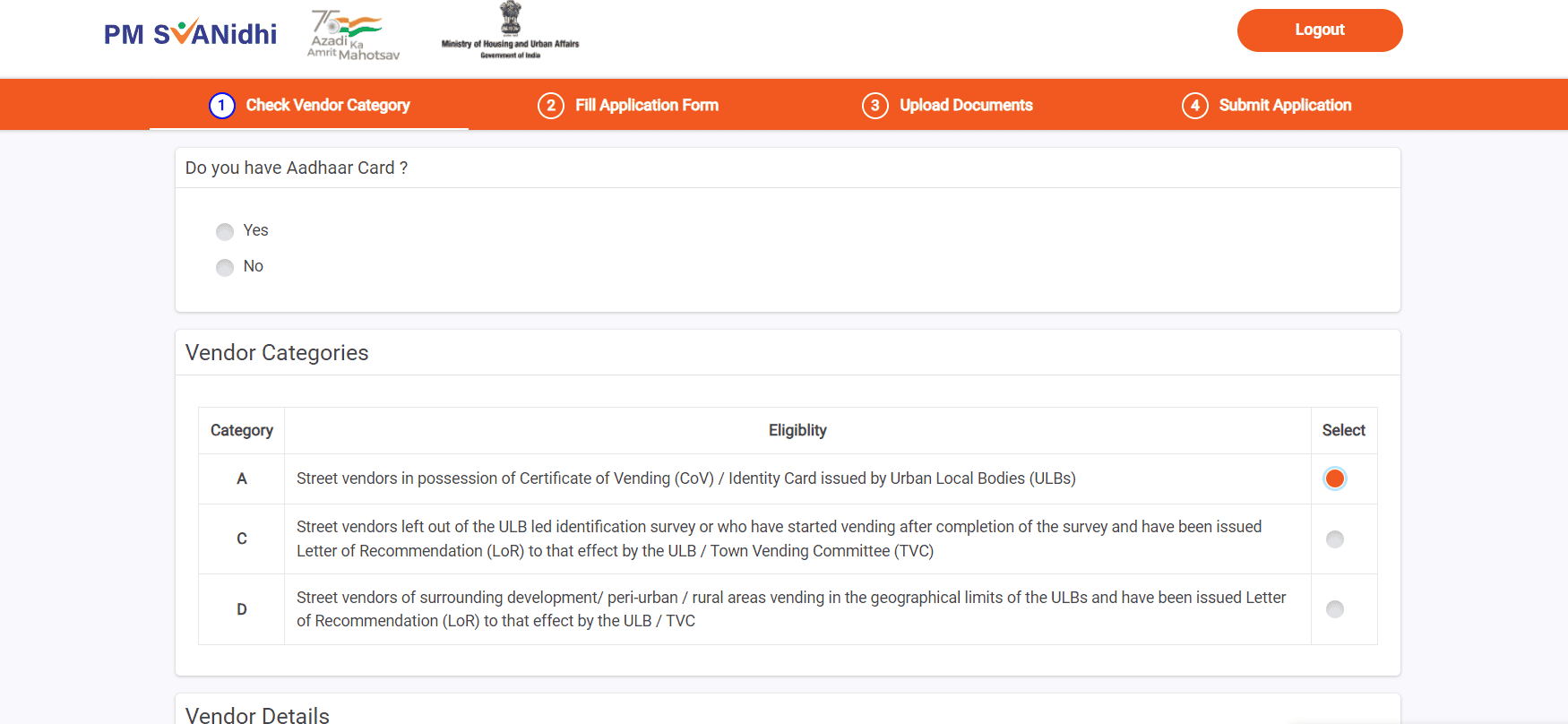

Before opting for PM SVANidhi Yojana online registration, it is advisable to check the following eligibility factors -

Other than fulfilling the SVANidhi scheme eligibility, beneficiaries might also consider knowing about the the application process.

Before beneficiaries apply for street vendors loan scheme online, they might want to consider some pre-application steps such as follows -

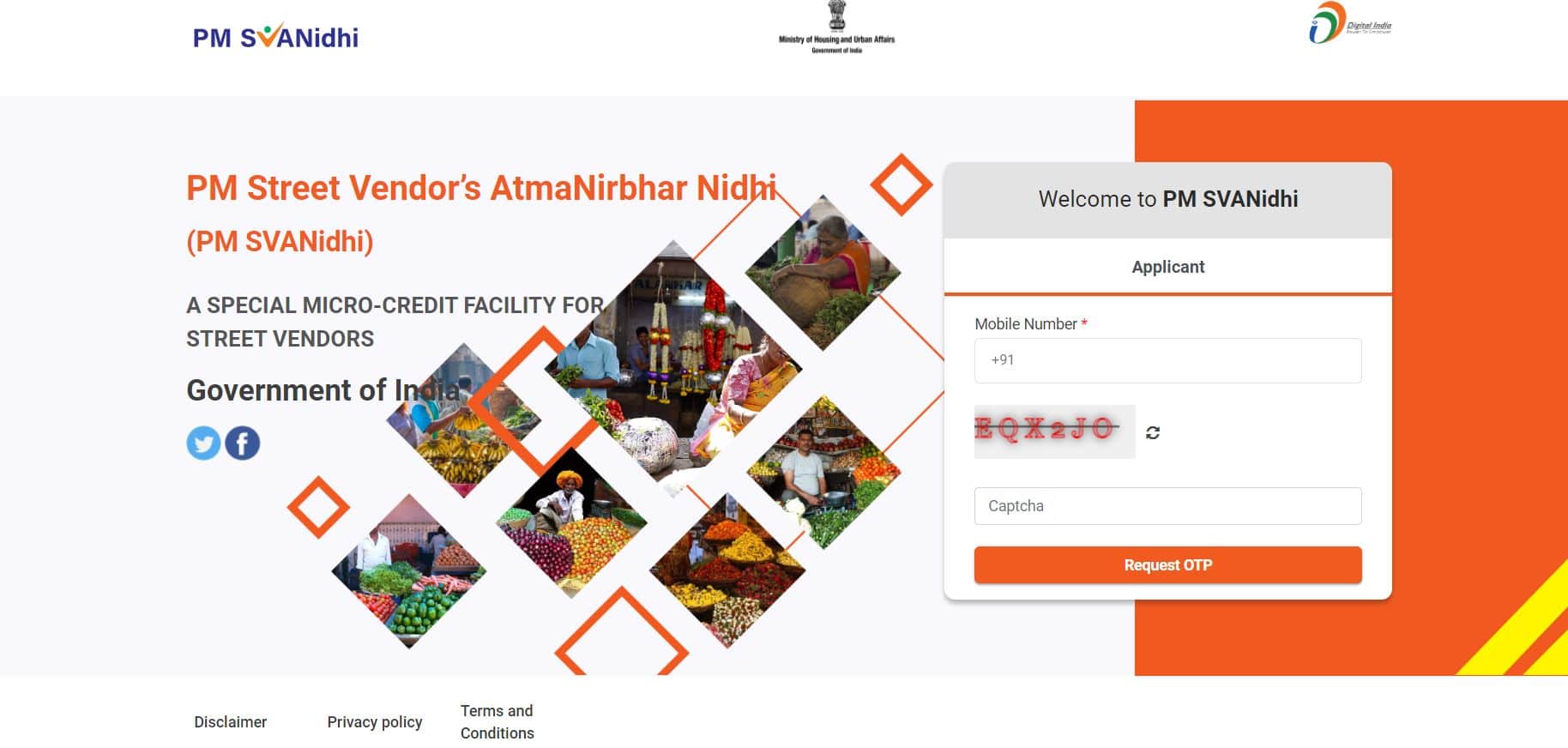

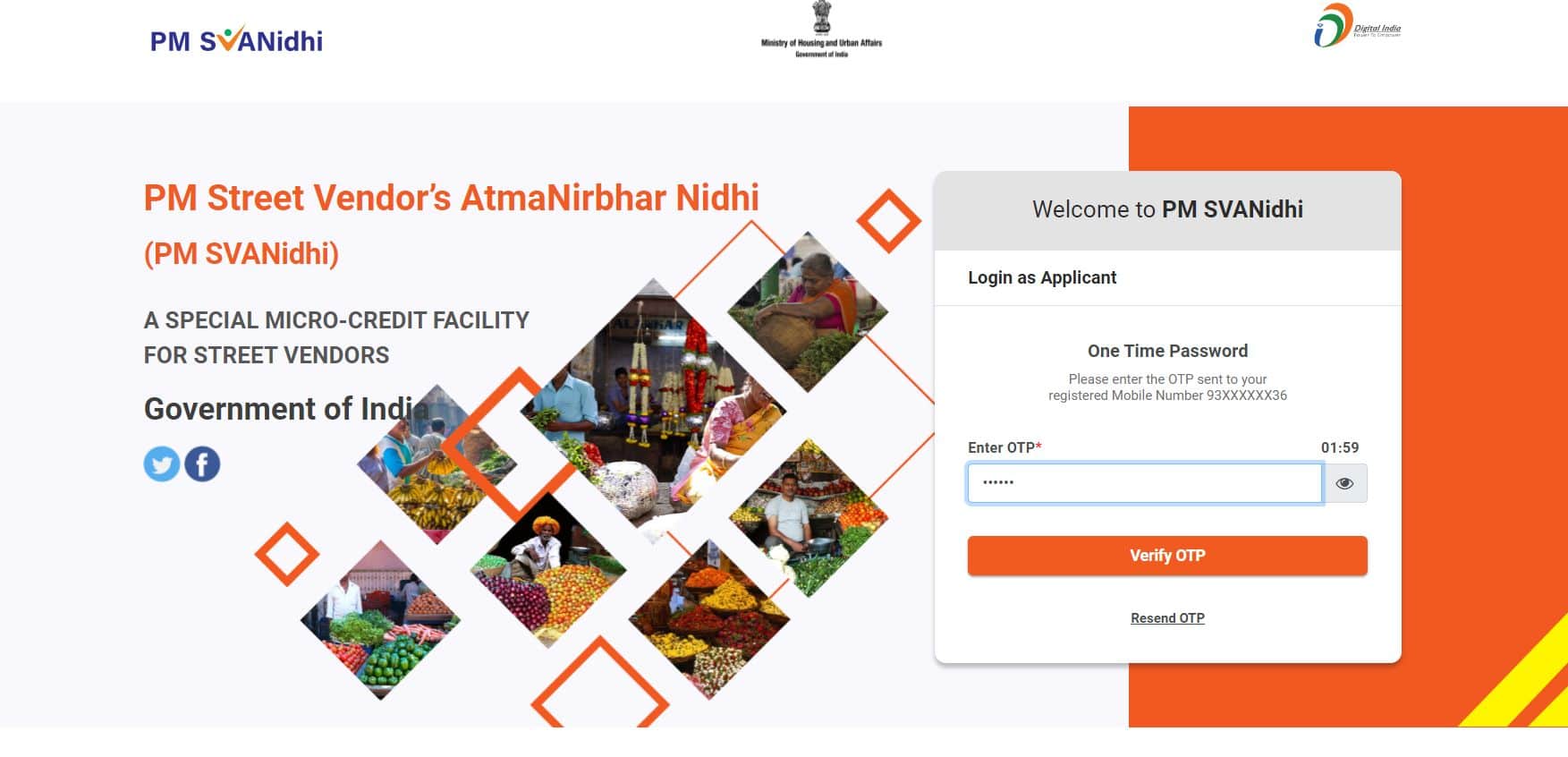

Once done, one can proceed to the SVANidhi Yojana online registration by following the below-mentioned steps.

These are the main steps to register online for PM SVANidhi Yojana without hassle:

By following these steps, you can successfully register yourself under the PM SVA scheme.

While applying for PM SVANidhi Yojana online to secure a collateral-free loan, vendors might need to present the following documents:

On successfully presenting the aforementioned documents, one can proceed to the PM SVANidhi scheme online application.

Beneficiaries will be required to follow these steps to check the PM SVANidhi status -

PM Sannidhi Yojana application status will be displayed on the screen.

Further, one might also like to know the perks they can enjoy under the PM SVANidhi Scheme.

This central government-backed scheme comes with a host of benefits as follows -

A working capital loan of ₹10,000 is available under this scheme for 1 year that can be repaid in monthly instalments. Also, these loans come without any collateral, meaning you need not put your assets on a mortgage to secure this financial product. In case of early or timely repayment of a loan, beneficiaries can obtain an enhanced loan amount limit for the next cycle.

Street vendors availing of a working capital loan under the PM vendor scheme are eligible for an interest subsidy of 7%. Borrowers will receive this amount quarterly.

This interest subsidy is available till December 2024. Credit Guarantee and Interest Subsidy claims on all loans will be paid till March 2028.

Individuals opting for digital transactions can avail of incentives in the form of cashback. With the help of a wide network of lending institutions and digital payment aggregators, vendors can get on board with digital processes.

These are some of the ways PM Svanidhi Yojana offers financial support to street vendors. This scheme has significantly improved livelihoods across India.

Street vendors play a significant role in making goods and services affordable for city dwellers, thereby becoming a vital constituent of the urban informal economy. As they work with a small capital base, it is prudent to require working capital to keep their businesses running, especially during unfortunate scenarios like pandemics.

Considering the ongoing COVID-19 situation, the Ministry of Housing and Urban Affairs launched the PM SVANidhi scheme to provide financial support to street vendors through working capital loans, interest subsidies, incentives and more.

Under the scheme guidelines, one can find the objectives, eligibility, product details and more.

By now, you must have understood that the PM SVANidhi scheme extends several benefits to vendors and hawkers in India. Therefore, skimming the above-mentioned piece can be helpful for them as it covers essential details necessary for a successful application.

You may also like to read:

As a street vendor, your daily income often depends on your ability to work consistently. To avoid financial strain during unexpected illnesses or accidents, it's wise to secure yourself with a health insurance policy.

Even a basic or government health plan can help cover hospital bills, ensuring you don’t have to dip into your savings or stop working for long periods. Additionally, setting aside a small emergency fund and staying aware of health-related government schemes can offer extra support during tough times.