General

Life

Accessibility Options

General

General Products

Simple & Transparent! Policies that match all your insurance needs.

Scan to download

Life

Life Products

Digit Life is here! To help you save & secure your loved ones' future in the most simplified way.

Scan to download

Claims

Claims

We'll be there! Whenever and however you'll need us.

Scan to download

General

General

Life

Life

Renewals

Resources

Resources

All the more reasons to feel the Digit simplicity in your life!

Scan to download

Our WhatsApp number cannot be used for calls. This is a chat only number.

8 Crore+ Customers

Affordable Premium

Implementation of the Goods and Services Tax (GST) is probably one of the most significant tax reforms our country has seen, and there have been many discussions on the topic ever since.

Some of the prominent queries here can be surrounding the GST invoice bill – the building block of this tax system. Here we provide a brief insight into what this document is and the several guidelines involving it. Read on!

If you are a GST-registered business, you are probably familiar with what a GST invoice is. However, for all the customers, here is a quick brief.

A GST-compliance purchase invoice contains the details of the parties involved in the mentioned transaction and lists all goods and services sold, with their prices. This bill also displays the percentage of discounts and taxes charged on each item, besides other details.

A GST invoice must be issued without fail by businesses that hold a GST registration. Other enterprises, however, do not need to issue these particular invoices.

Here is a list of particulars that must be present in a GST tax invoice specified under Rule 54 of the CGST Act of 2017.

Name, GSTIN, and address of the supplier

Invoice number

Date of issuance

Invoice type

Shipping and billing address

Name of the customer

Address of the recipient

Address of Delivery

State name and State Code

GSTIN of the customer if registered

Details of products and services provided, including description, quantity, etc.

SAC code or HSN code

Rate of CGST, IGST, UTGST, and SGST charged

Total tax amount and discounts, if any

Reverse charge

Signature of the invoice issuer

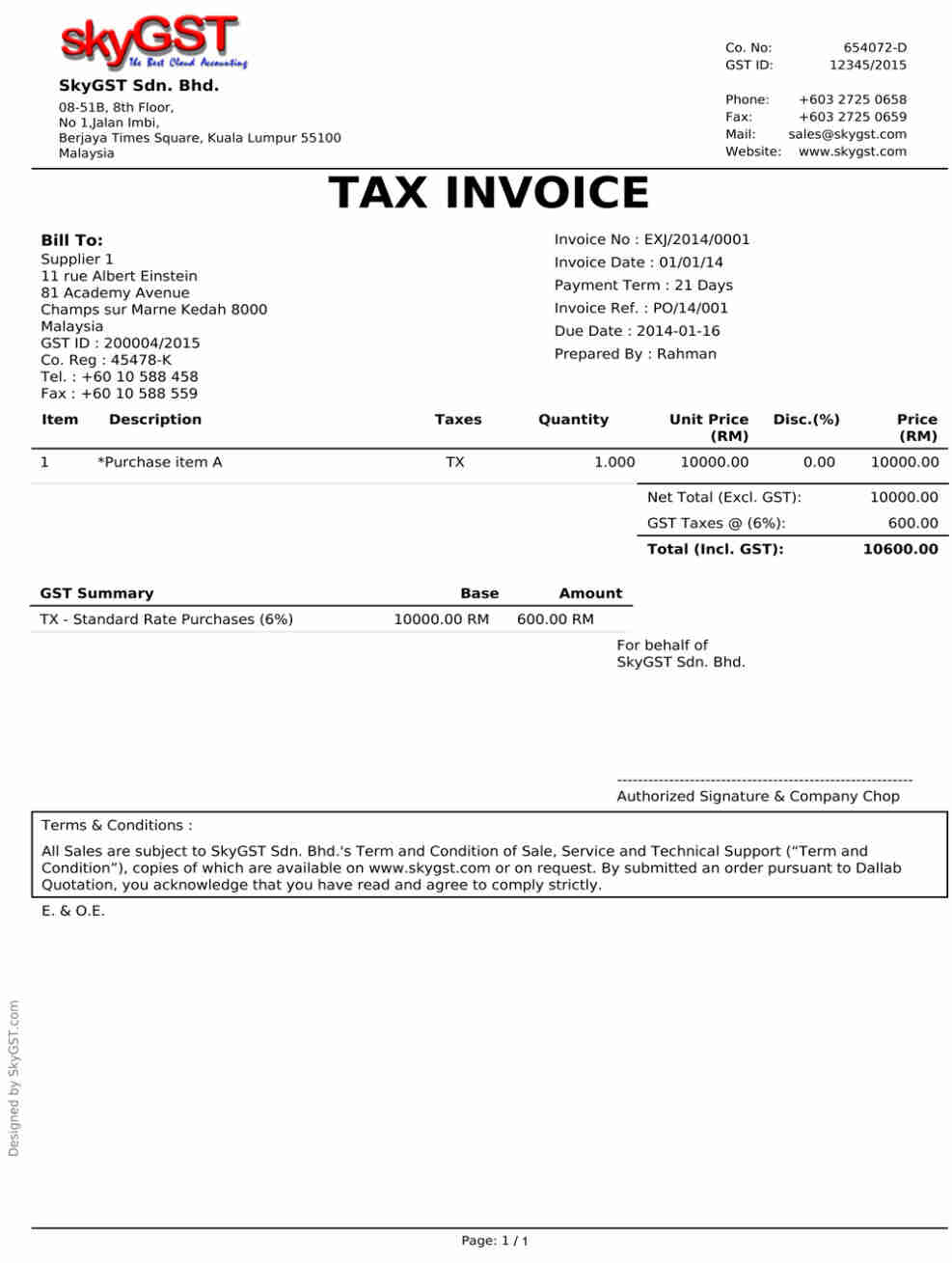

Here, have a look at how it looks on paper.

Now you might be wondering if it is necessary to enclose every single of these details in a GST invoice bill. Well, it is mandatory when there are laws to enforce it.

When following the above guidelines in terms of invoice contents, issuers need to consider certain rules that specify the “what” and “how” of these details.

Following are the mandates that issuers need to follow as per Rule 46 (b).

The CGST rules make the issuer's signature one of the mandatory fields in a GST invoice. Specifications of a valid signature are as follows.

As per section 116 (2), his/her ‘authorised representative’ can be a company secretary, a practising advocate, a chartered accountant, a retired officer of the Commercial Tax Department, or a regular employee appearing on the supplier’s behalf.

Another mandate under the CGST Act concerns a scenario where a GST-registered individual makes purchases from a seller who is not registered. There can be 2 cases here.

Now, you might be wondering that it might get difficult to always issue an invoice following such extensive guidelines right upon purchase every time.

To ease this process, the Indian government has also provided outlines regarding the time of issue of invoice under GST.

That was all about the important rules and regulations regarding tax invoices. Now, this is not the only type of invoice in practice.

Want to know about the other prevalent types under GST?

Keep reading.

The only difference between a bill of supply and a tax invoice is that a 0% or no GST is charged in the former. Therefore, this type of invoice can be issued in 2 cases.

As a result, the recipient does not have the provision to claim an input tax credit based on this document.

Also, a registered entity can issue an all-encompassing invoice-cum-bill of supply if it deals in both exempt and taxable services/goods.

If a seller issues multiple invoices to an unregistered buyer, each less than Rs.200, he/she can issue a single invoice, summing up all the amounts. This is called a bulk or aggregate invoice.

Such commercial documents are issued when there is any discrepancy found in a previously issued tax invoice for a product or service.

A debit note is issued when any of these 2 conditions arise.

On the other hand, a credit note is issued for the opposite reasons.

Besides the above types of invoices in GST, there are several other documents and vouchers relating to such transactions, depending on several conditions.

There can be several instances of incorrect GST invoices being issued. Under current GST rules, such invoices can be revised.

If a supplier becomes liable for GST registration and applies within 30 days, the effective date of registration is the date of liability. Any invoices issued between the date of liability and the date of registration approval must be revised within one month from the date of issuance of the GST registration certificate.

The revised invoice must be clearly labelled as “Revised Invoice” and include all mandatory details such as GSTIN, invoice number, date, HSN/SAC codes, and place of supply.

As of September 22, 2025, GST rates have been revised under GST 2.0. Businesses must ensure that invoices reflect the correct rate based on the time of supply rules.

Additionally, revised MRP stickers on unsold stock are now optional, and businesses may pass on GST rate benefits through point-of-sale discounts or by updating their price lists.

For businesses with turnover above ₹5 crore, e-invoicing is mandatory, and invoices must be uploaded to the IRP within 30 days of issuance.

There you go! These are the relevant details regarding a GST invoice. Given the recent rate changes effective September 22, 2025, and the stricter e-invoicing timelines, it is crucial to ensure that your billing systems and software are updated to remain compliant. If you are a registered dealer, ensure that you issue such documents to avail of Input Tax Credit (ITC). If you are not GST-registered yet, consider getting a certificate to help your business benefit from such provisions.

Since proof of transaction should remain with all parties involved, there are a specific number of invoice copies issued depending on the type of supply.

The dealer must produce 3 copies of the GST invoice bill issued.

In the case of services, the issuer needs to arrange 2 copies of the invoice.

There you go! These are the relevant details regarding a GST invoice bill. If you are a registered dealer, ensure issuing such documents to avail Input Tax Credit (ITC). If you are not GST-registered yet, consider getting a certificate to help your business benefit from such provisions.

When issuing a GST invoice online, a supplier must upload the invoice’s JSON on the Invoice Registration Portal (IRP). Now, the Invoice Registration Number is generated by IRP, and it will digitally sign the JSON using its private key. Once signed, it will become a valid e-invoice, and the IRP will send this document to the e-way bill system and GSTIN.

A supplementary invoice needs to be issued when:

While invoice date is the date on which this document is created, the due date refers to the deadline within which the amount on this invoice must be paid.