General

Life

Accessibility Options

General

General Products

Simple & Transparent! Policies that match all your insurance needs.

Scan to download

Life

Life Products

Digit Life is here! To help you save & secure your loved ones' future in the most simplified way.

Scan to download

Claims

Claims

We'll be there! Whenever and however you'll need us.

Scan to download

General

General

Life

Life

Renewals

Resources

Resources

All the more reasons to feel the Digit simplicity in your life!

Scan to download

Our WhatsApp number cannot be used for calls. This is a chat only number.

A reimbursement claim in health insurance is when you pay for your medical treatment out of pocket and later submit a claim to your insurer to get that money back.

This type of claim is typically used when you receive treatment at a non-network hospital or in situations where cashless services aren’t available. While it requires you to handle the hospital bills initially, the insurer reimburses you for eligible expenses once you submit the necessary documents and the claim is approved.

I agree to the Terms & Conditions

Get Exclusive Porting Benefits

Check Prices

Buy Health Insurance, Up to 20% Discount

Port Existing Policy

9000+

Cashless Hospitals

3.8 Crore+

Lives Insured

8 Lacs+

Claims Settled

A reimbursement claim is an official request for compensation or a refund for out-of-pocket medical expenses made by a policyholder to their health insurance policy provider.

In simple words, a Reimbursement Claim is a type of claim in which an insured must pay for medical costs and treatment out of their own pocket and later claim the bill from the insurance provider. For this kind of claim, the insured can visit any hospital for treatment, not necessarily the empanelled cashless hospital.

Let’s understand this with an example:

Shweta has a health insurance policy and resides in Delhi. She had to undergo a minor nerve surgery, for which she visited her family neurosurgeon. Unfortunately, the hospital she chose was not empanelled with the insurance company. 😣

After treatment, she paid the treatment cost herself and kept all the essential documents, invoices and receipts. She filled out a reimbursement claim for the insurance company and after verification, her expenses were returned to her. 🙂

No Location Constraints

You can visit your desired healthcare facilities and utilise your health insurance benefits. It can be any other hospital rather than an empanelled cashless hospital to help you avail yourself of your health insurance benefits.

Immediate Treatment

Before starting the treatment, you need not wait for the insurance provider's approval or other insurance-related procedures. You can receive immediate treatment at your desired hospital with a high state-of-the-art facility.

Flexibility in Claim Process

You can apply for a reimbursement claim as soon as your medical care is finished and the bills have been paid. This procedure removes delays and ensures a seamless and effective compensation experience.

A reimbursement claim works by allowing you to pay for your medical treatment upfront and then recover the eligible expenses from your health insurance provider. Here's a step-by-step explanation of how it works:

Get Treated at Any Hospital

Select any hospital (whether within a network or not) for treatment.

Pay & Keep the Bills

Settle all medical expenses upfront from your own pocket and keep the bills or invoices, such as those for doctor’s consultations, diagnostic reports, and hospital bills.

Submit a Claim to the Insurer

Complete the claim form and submit it along with the required supporting documents.

Claim Review & Verification

The insurer reviews your documents to verify the treatment, expenses, and policy coverage. They may request additional documents if necessary.

Approval and Reimbursement

Once approved, the insurer reimburses the claim amount directly into your registered bank account.

Get Treated & Save Everything

Visit any hospital, pay the bills upfront, and collect all the necessary documents (bills, reports, prescriptions, discharge summary, etc).

Open Digit App & File Claim

Log in to the Digit App. Navigate to the ‘File a Health Claim’ section on the app. Choose the policy, enter your details and & type of claim (reimbursement claim).

Enter Details & Upload Documents

Fill out additional details of treatment, symptoms, hospital details, etc. Scan and submit all the necessary documents in the desired format.

Register Claim & Relax

Click ‘Register Claim.’ We’ll review everything, and once approved, the amount will be reimbursed directly to your bank account.

When filing a health insurance claim, you need to submit certain documents to ensure a smooth and hassle-free process. Below is a list of essential documents that may be required while filing a reimbursement health claim at Digit:

Hospitalisation Documents

✔ Original hospital bills & payment receipts

✔ Detailed discharge summary

✔ All diagnosis reports (lab tests, imaging, etc.)

✔ Doctor’s consultation & prescription copies

✔ Pharmacy and medicine bills

Cashless Documents

✔ Duly filled & signed claim form (Available at the hospital or on Digit’s website/app)

✔ Diagnosis report for confirming the need for hospitalisation

✔ Health E-card

KYC Documents

✔ Aadhaar Card (Identity & address proof)

✔ PAN Card (Financial verification)

✔ Photograph

✔ Bank Details (Passbook or cancelled cheque)

A reimbursement claim becomes necessary when you’ve paid for medical expenses out of pocket and must recover the costs from your insurer. This often happens when treatment is done at a non-network hospital in India, where cashless facilities are unavailable.

Additionally, expenses such as pre and post-hospitalisation costs, diagnostic tests, and outpatient treatments that aren’t covered under cashless claims may require reimbursement filing.

Let’s take different cases and understand which claim you should file in which situation:

Scenarios |

Type of Expense |

Type of Claim to File |

You went for planned surgery in a network hospital where the insurer settles the bill directly with the hospital. |

Hospitalisation |

Cashless Claim |

You had to undergo emergency surgery at a non-network hospital, where you had to pay the bills. |

Hospitalisation |

Reimbursement Claim |

You needed immediate hospitalisation due to an accident. |

Accidental Hospitalisation |

Cashless Claim (network hospital) and Reimbursement Claim (non-network hospital) |

You underwent surgery in a network hospital in India, but your cashless claim was rejected due to missing documents. |

Hospitalization |

Reimbursement Claim |

You had to undergo a consultation and lab tests weeks before and after getting hospitalised for a medical procedure. |

Pre & Post-Hospitalisation Claim |

|

You had to visit a clinic weekly for skin allergy treatment without requiring hospitalisation. |

OPD Expenses |

Reimbursement Claim |

Medical reimbursement claims might be a good option, considering the flexibility they provide in terms of selecting the medical centre for treatment. We can choose any desirable hospital, not just the empanelled hospital.

However, while opting for a reimbursement claim or selecting a non-network hospital, one must consider a few points as listed below:

For both network and non-network hospitals, reasonable and customary charges, which are the standard charges for a specific provider and consistent with prevailing charges in the geographical area for identical or similar services, taking into account the nature of the illness /injury involved, and which are medically necessary, will be considered for payment of admissible claims.

In case treatment is received at a Network hospital, payment of claims will be as per Digit’s pre-negotiated rates with the hospital and in case treatment is received at a non-network hospital, reimbursement will be limited to rates applicable at par with another comparable network hospital.

This may sound unusual, but there are several reasons why claims can be rejected. It can be due to either documentation or incorrect information. Let’s discuss the common reasons why your claim can be rejected:

Don't freak out if your reimbursement claim is denied. You can re-apply for a claim if the claim is rejected because of documentation. Here are some ways you can deal with claim rejections with the following actions:

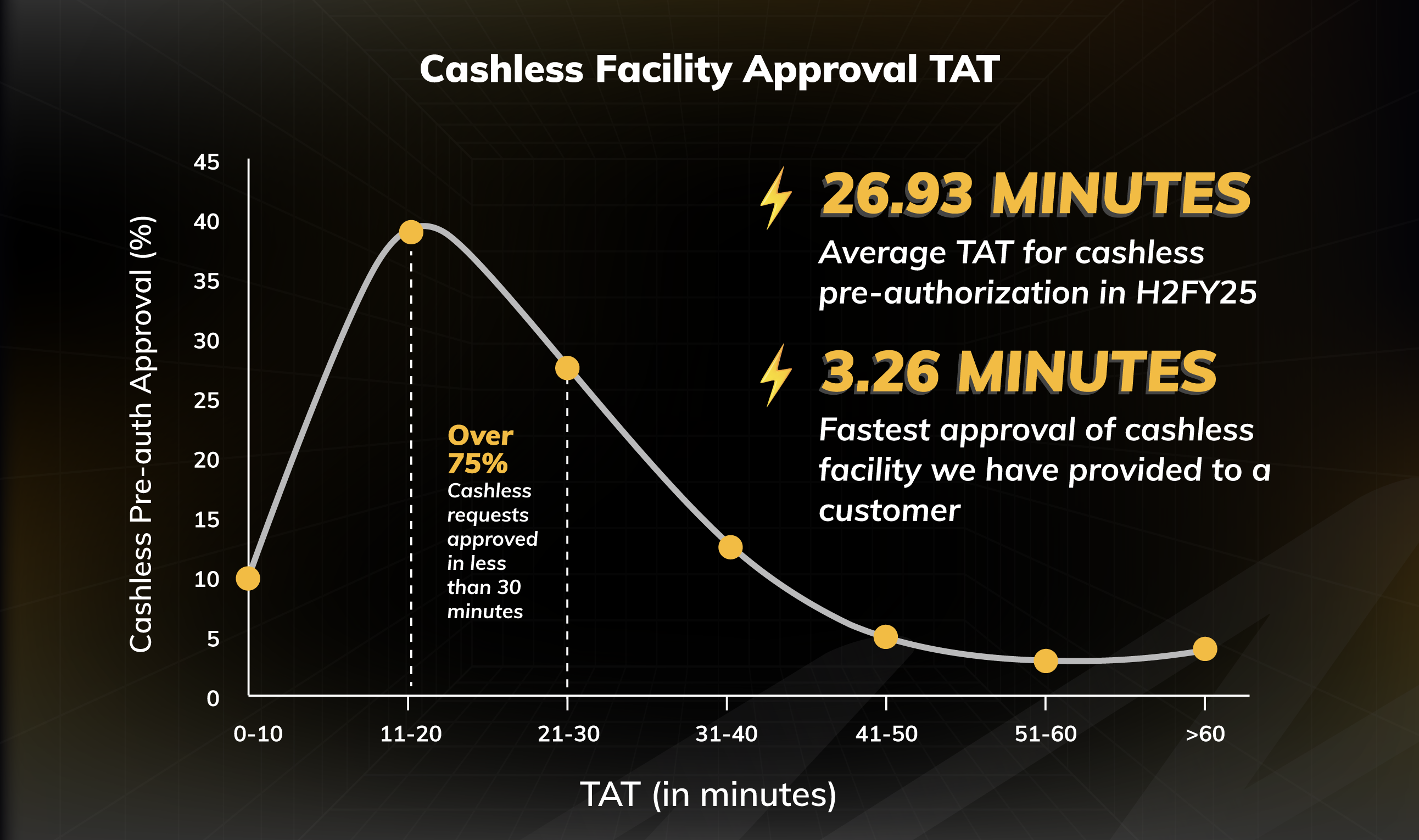

75% of Cashless Health Claims Approved in Just 30 Minutes at Digit

At Digit, in the second half of FY25, the average turnaround time (TAT) for pre-authorisation of health insurance cashless claims was a speedy 26.93 minutes. Even better? Over 75% of requests were approved within 30 minutes, making the process feel almost instantaneous.

Of course, some requests, around 3.3% took a little longer (over 60 minutes), mainly because they needed extra info or clarification from hospitals or customers.

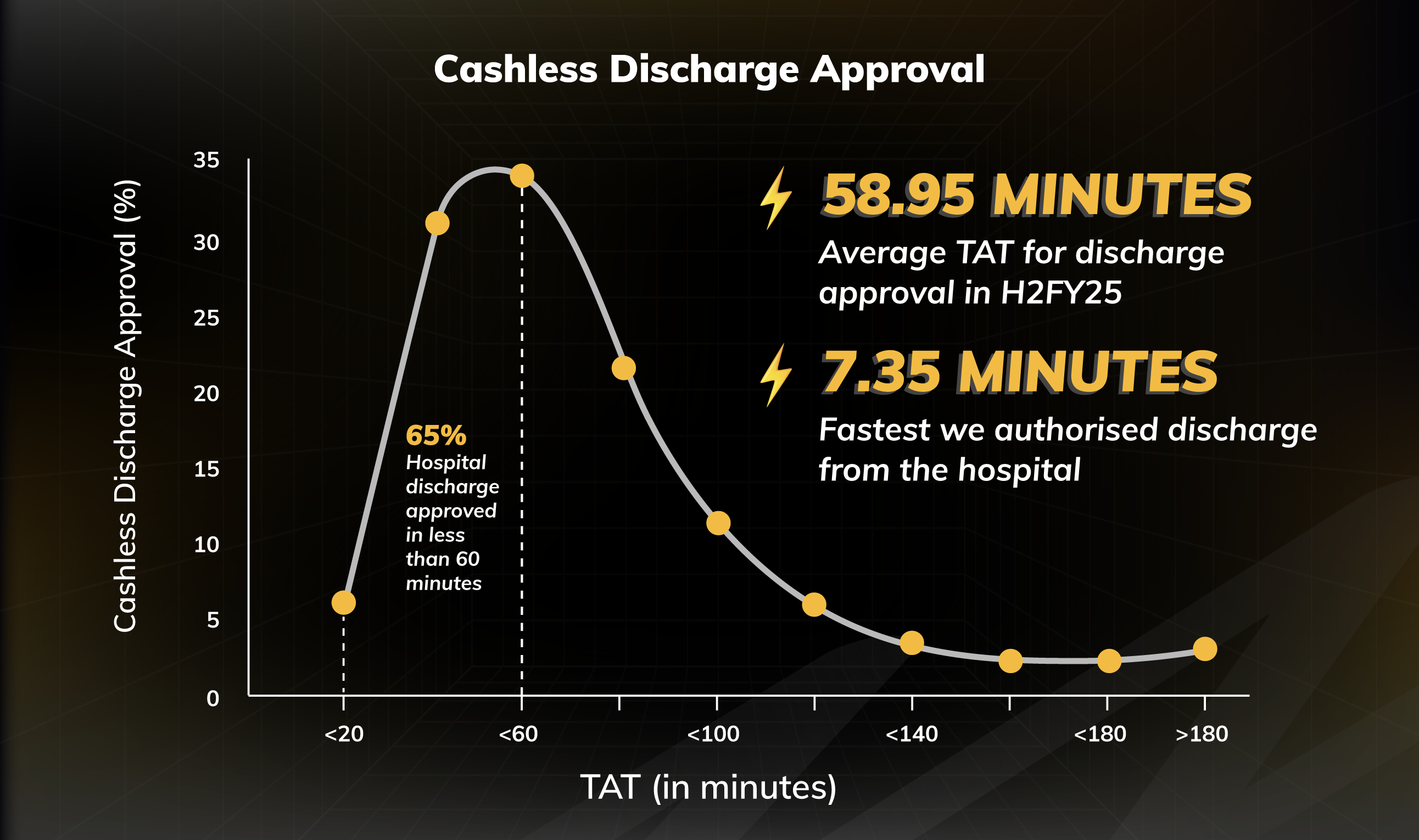

65% Cashless Discharge Approved in Just 60 Minutes at Digit

At Digit, in the second half of FY 2024-25, the average turnaround time (TAT) for hospital discharge approval in our health insurance was 58.95 minutes. Notably, 65% of discharge requests were completed within 60 minutes, ensuring patients aren’t left waiting once their treatment is finished.

While only 1.3% of cases extended beyond three hours, typically due to complex queries or pending clarifications.

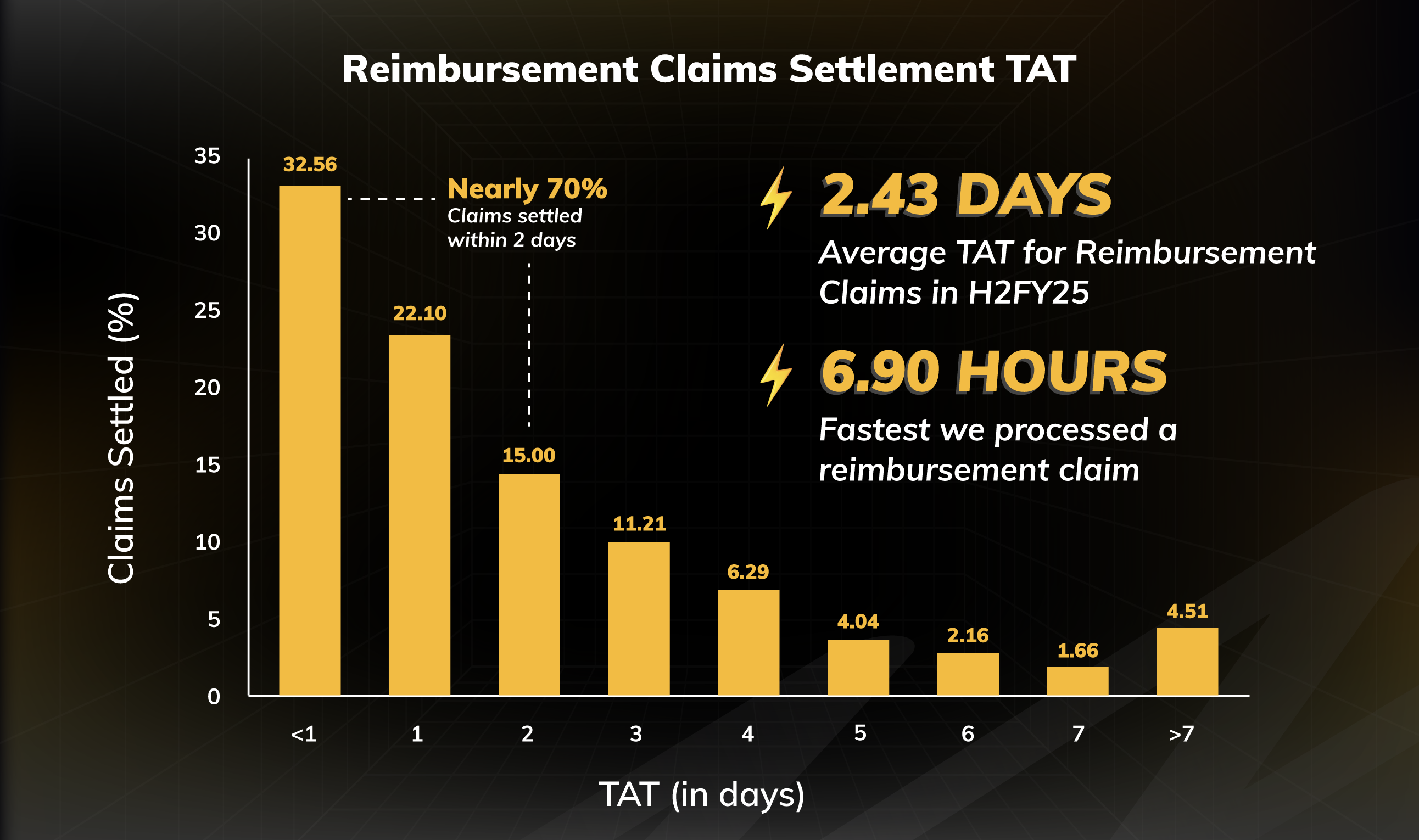

Almost 70% of Reimbursement Claims Settled in Just 2 Days

Not every hospital is part of a cashless network, and that’s where reimbursement claims come into play. Once all documents are submitted, the average turnaround time for processing a reimbursement claim at Digit in FY 2024-25 was just 2.43 days.

Nearly 70% of claims were settled within two days, providing quick relief to policyholders who initially had to pay out of pocket. While about 4.5% of claims took over a week to settle, usually due to missing documents or follow-up queries, the process is largely smooth and customer-centric.

1.1 Lakh+ Claims Registered Quickly with Smart Health Claim Bots in FY 2024-25

At the heart of smooth insurance experiences lies something you never see!! 😁

At Digit, our Health Claims Bots and Bulk Policy Issuance are quietly reshaping the way claims get processed. These smart systems fetch real-time data directly from the partner, eliminating manual uploads, reducing errors, and speeding up approvals for claims. In FY 2025 alone, they registered over 1.1 lakh claims, cutting down processing time.

No breaks and no delays. Fewer forms and faster care! ☺️

Highest Health Claim of ₹16.77 Lakh Settled by Digit in FY 2024-25

A Bengaluru customer faced a serious and complex medical condition, leading to a treatment bill running into lakhs. Digit settled its highest health insurance claim in FY 2024-25, amounting to approximately ₹16.77 lakh.

What mattered more was how quickly and transparently we stepped in. From the initial notification to the final settlement, the entire claim was handled with empathy, clarity, and minimal stress.

At Digit, it’s not the size of the bill that moves us; it’s the trust behind every claim we settle. 🙂

Over ₹27 Crore Settled for Pre and Post-Hospitalisation Expenses in FY 2024-25

At Digit, we believe health insurance is more than just hospital bills. This year, a patient undergoing treatment for malignancy received coverage not only for their hospitalisation but also for over 10 pre and post-hospitalisation visits, with a total payout exceeding ₹1.4 lakh. This reflects our commitment to supporting patients through every step of their recovery journey.

In fact, Digit paid out more than ₹27 crore this year alone towards pre and post-hospitalisation expenses, proving that genuine care extends before and after hospitalisation as well.

This is what we mean when we say insurance that supports the full journey, not just the hospital stay. 🙂

7,747 Babies Covered Under Their Parents' Policies in FY 2024-25

In FY 2024-25, Digit proudly covered around 7,747 babies under their parents’ policies, protecting the newest generation with the same care and commitment as every policyholder.

Among these little ones, the most popular baby names were Shivansh and Fatima, reflecting the diverse families Digit supports across India. 🙂

This wouldn’t be possible without Digit’s flexible family health plans, which automatically extend coverage to newborns, making it easy for parents to safeguard their little ones from day one.

You might have understood by now that reimbursement claims in health insurance offer a reliable solution for managing medical expenses when cashless facilities aren’t an option.

Understanding the process and ensuring all required documentation is in place can help you easily reclaim your financial outlays. This is crucial to ensuring comprehensive health coverage, giving you peace of mind and allowing you to focus on what truly matters—your recovery and well-being.

To monitor your reimbursement claim, you can:

There are certain advantages of having a cashless claim over a reimbursement claim because: