General

Life

Accessibility Options

General

General Products

Simple & Transparent! Policies that match all your insurance needs.

Scan to download

Life

Life Products

Digit Life is here! To help you save & secure your loved ones' future in the most simplified way.

Scan to download

Claims

Claims

We'll be there! Whenever and however you'll need us.

Scan to download

General

General

Life

Life

Renewals

Resources

Resources

All the more reasons to feel the Digit simplicity in your life!

Scan to download

Our WhatsApp number cannot be used for calls. This is a chat only number.

7 Crore+ Customers

Affordable Premium

GST or Goods and Services Tax is an indirect tax. It came into force on July 1, 2017. GST has replaced other prevalent indirect taxes like VAT, excise duty, and services tax and ideated from the concept of maintaining uniformity in a tax structure.

Taxpayers registered under the Goods and Services Tax Act must file GST returns, whichever is applicable based on the nature of their business. This article highlights all the crucial aspects of how to file GSTR-1 that are pivotal to consider while filing this form.

GSTR-1 is a return that contains the compilation of sales constituting outward supplies of a taxpayer. This return is filed either monthly or quarterly by an individual registered under the GST Act and has a valid GSTIN number. The meaning of GSTR-1 can be broken down into 13 main sections and 5 sub-sections, which are:

Under the Goods and Service Tax Act, it is mandated to file GSTR-1 by every dealer who is registered under the Act. This is irrespective of whether there are any transactions or sales for a particular month. As per the provisions of this Act, here are the types of dealers who are exempted from filing GSTR-1 are:

Apart from the list mentioned above of dealers, every registered person dealing with all outward supplies must know how to file GSTR-1.

Here is the complete guide highlighting how to file GSTR-1 online for a taxpayer looking for the same:

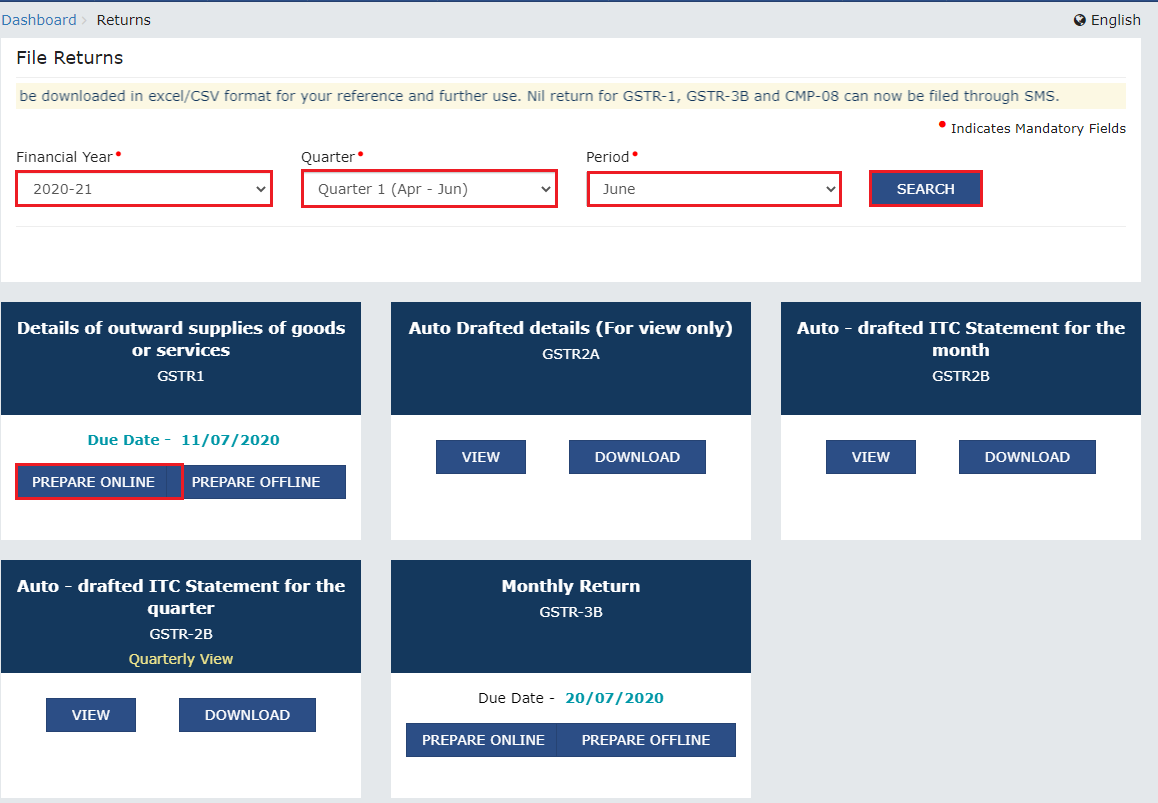

Step 1: First step of filling the GSTR-1 return starts with logging into the GSTIN portal by providing a username and password.

Step 2: In this step, click on "Services" present on top of the homepage bar. On clicking the "Service" option, you must select "Return" from the dropdown.

Step 3: On clicking the return option, it will redirect you to the ‘Return’ dashboard page. On this page, the taxpayer needs to select the financial year and month for which he or she is filing the return. Upon filling these details, the month's revenue will appear on that page in the tile position.

Step 4: On this page, select the GSTIN-1 tile. In this particular tile, the taxpayer needs to fill up all the information as mentioned in the 13 sections.

Step 5: This step to filing GSTR-1 involves adding all the heads of receipts or invoices. If the taxpayer wants, he or she can upload all invoices for convenience.

Step 6: Upon completion of adding all invoices, click on the "Generate GSTR1 Summary" option. However, to avoid the occurrence of any mistakes, it is important to validate the information that has been filled in the form.

Step 7: If the details provided by a taxpayer are accurate, click on the "PROCEED to FILE/SUMMARY" option. Furthermore, a taxpayer will need to click on File Statement and verify the same using digital signature or E-Sign to complete this process.

Step 8: In this final step, a taxpayer will be able to see a confirmation message popped-up. In addition, there will be an option to agree to or deny the pop-up. Upon pressing the "Yes" button, the taxpayer will get an Acknowledgement Reference Number (ARN).

This ARN number serves as proof that a respective taxpayer has filled in the GSTR-1 number.

Generally, applicants do not need to attach documents while filing GST returns. However, information related to the issuance of B2B invoices, B2C invoices, debit notes, credit notes and HSN summaries of sold goods must be uploaded.

Here is the following information that a taxpayer must submit:

Apart from this, documentation can vary depending on whether an individual has a valid GSTIN or not. It includes:

A taxpayer with a valid GSTIN and issuing B2B invoices must provide the following information:

Here is the information that a taxpayer must upload with no valid GSTIN filing for B2C invoice which is more than ₹2.5 lakh:

The due date for filing GSTR-1 depends on the yearly aggregate turnover of a taxpayer. The Goods and Service Tax Act says that:

Some of the highlighted amendments that have come into effect from the recent taxation indirect tax regime which taxpayers searching for “how to file GSTR-1 return” are as follows:

Taxpayers cannot file GSTR-1 after the expiry of a period of three years from the due date of furnishing the said return. For instance, returns for June 2022 are barred from being filed from 1st August 2025.

HSN Code Reporting in Table 12: Manual entry of HSN codes has been replaced by choosing the correct HSN from a given drop-down menu. Furthermore, Table 12 has been bifurcated into two tabs, namely B2B and B2C, to report these supplies separately.

Here are some of the benefits that make filing GSTR-1 quintessential are:

As per the current provision of this Act, all registered dealers with outward supplies must file GSTR-1. In case of no outward supplies for a specific month, a taxpayer needs to file a nil GSTR-1 return for that period. Moreover, failure to file this GSTR-1 within the aforesaid time period will attract a maximum late fine of Rs. 200/Day.

In addition to this, taxpayer searching for “how to file a GSTR-1 return” must know the following pivotal updates regarding penalties:

It is essential to note that these penalties do not apply to taxpayers who are filing NIL rate of GST return. Moreover, those eligible to file GSTR-1 must submit a return on time in order to avoid heavy penalties and further legal complications. Understanding all aspects and processes of how to file GSTR-1 will ensure the tax report of businesses is up-to-date.