General

Life

Accessibility Options

General

General Products

Simple & Transparent! Policies that match all your insurance needs.

Scan to download

Life

Life Products

Digit Life is here! To help you save & secure your loved ones' future in the most simplified way.

Scan to download

Claims

Claims

We'll be there! Whenever and however you'll need us.

Scan to download

General

General

Life

Life

Renewals

Resources

Resources

All the more reasons to feel the Digit simplicity in your life!

Scan to download

Our WhatsApp number cannot be used for calls. This is a chat only number.

7 Crore+ Customers

Affordable Premium

GSTR 4 is a GST return that must be filed by composition dealers registered under Section 10 of the CGST Act. It came into action with the Third Amendment of 2019 to GST Rules 2017. This article covers all the essential aspects that one must keep in mind while filing GSTR-4.

Read on to learn more about what GSTR-4 is.

Good and Service Tax, popularly known as GST, serves as a replacement for other common indirect taxes, such as excise duty, VAT, and services tax. Though the Parliament passed GST on 29th March 2017, it came into action on 1st July 2017.

Unlike other GST returns, GSTR-4 is required to be filed annually, not quarterly. It keeps a record of their outward and inward supplies. To make the meaning of GSTR-4 simpler, the contents of its form have been discussed followingly:

Since GSTR-4 is clear, let us move to the next aspect.

To be eligible to file GSTR-4, one has to:

Apart from Composition Scheme, vendors also need to meet the following regimes:

For a prompt and hassle-free GSTR-4 filing, a composite vendor must keep the below documents within reach:

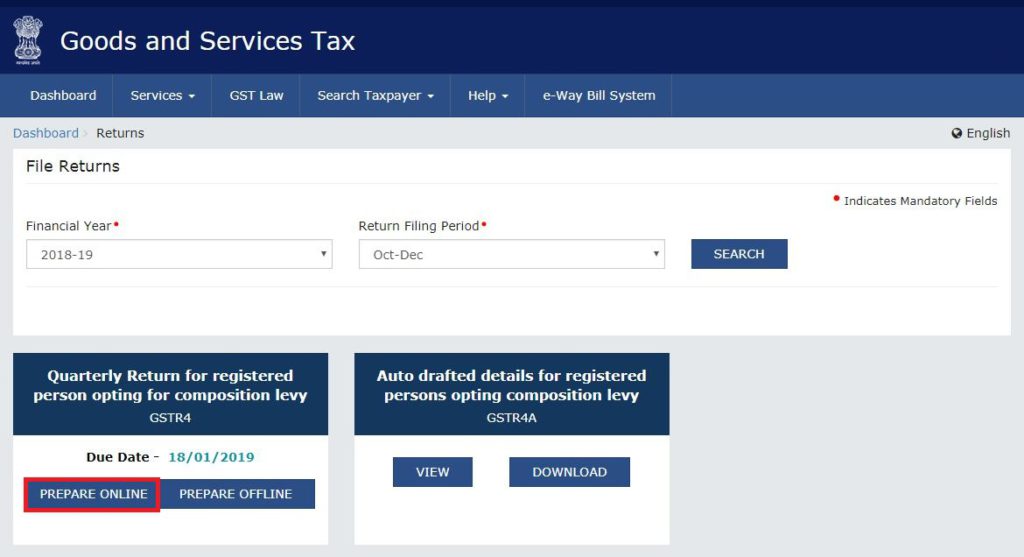

Here is a rundown of filing GSTR-4 online:

Step 1: Sign in to the GST Portal and follow the navigation from “Service” to “Return” to “Annual Return”.

Step 2: Choose the relevant financial year.

Step 3: Mindfully read the instructions and click on “Prepare Online”.

Step 4: Enter the evaluated turnover value of the former fiscal year and proceed to the save button. In case of no turnover, enter zero into the space to avoid leaving it blank.

Step 5: This step is for filing nil GSTR-4. If not needed, one can simply skip this step. However, to apply for a nil GSTR-4, taxpayers have to click on "Proceed To File".

Step 6: Furnish applicable details to all the tables by selecting them one by one from the dropdown list of “Select tables to add/view details”.

Step 7: After carefully entering the information, click “Proceed To File” for a quick preview of the saved return. Once done, keep a copy of it by pressing “Download GSTR-4 Summary (PDF)” or “Download GSTR-4 (Excel)”. Proceed to the next step with a click on “Continue”.

Step 8: Input details of tax, interest, and late fee irrespective of the fact that whether they are payable or paid. Choose your preferred payment mode from:

And proceed with "Generate Challan".

If Electronic Cash Ledger comprises enough balance, the amount will automatically be adjusted, reflecting zero in the "Additional Cash Required" column. This step permits you to review the GSTR-4 return one more time before sailing off to the final step.

Step 9: Here, taxpayers must confirm the declaration checkbox. Also, he or she has to select the authorized signatory.

Click on the "File GSTR-4 Button." Post-clicking, a warning message will pop up. Ensure to enter yes to successfully file GSTR-4 with either DSC or EVC.

Completion of the final step will lead to the following outcomes:

GSTR-4 is an annual return that must be filed by taxpayers registered under the GST Composition Scheme. As per the latest update from the 53rd GST Council Meeting and CGST Notification No. 12/2024, the due date for filing GSTR-4 has been extended to 30th June of the following financial year. For example, GSTR-4 for the financial year 2024-25 must be filed by 30th June 2025.

Failure to file GSTR-4 by the due date attracts a late fee of ₹50 per day (₹25 under CGST and ₹25 under SGST), subject to a maximum of ₹2,000. For nil returns, the late fee is ₹20 per day, capped at ₹500. Additionally, GSTR-4 cannot be filed after three years from its original due date, effective from July 2025 onwards.

If one fails to file by the due date, ₹200 is imposed per day, which can reach a maximum of ₹5000.

However, according to the state-of-the-art update, the payable late fee has been lessened to ₹50 per day with a maximum of up to ₹2000. The maximum late fee for filing nil GSTR-4 has become ₹500.

Central Board of Indirect Taxes and Customs, or CBIC, has published an additional provision under one of their earlier notifications issued on 29th of 2017.

Updated Notification 73:

Any late payable fee under section 47 of the CGST Act 2017 that stands higher than ₹250 shall be waived completely. This amendment applies to those:

Composite vendors who fall within this category must apply for the return from 1st April 2023 to 31st August 2023.

Now that we clearly understand what GSTR-4 is and its filing process. Let us take a short tour of its advantages: