General

Life

Accessibility Options

General

General Products

Simple & Transparent! Policies that match all your insurance needs.

Scan to download

Life

Life Products

Digit Life is here! To help you save & secure your loved ones' future in the most simplified way.

Scan to download

Claims

Claims

We'll be there! Whenever and however you'll need us.

Scan to download

General

General

Life

Life

Renewals

Resources

Resources

All the more reasons to feel the Digit simplicity in your life!

Scan to download

Our WhatsApp number cannot be used for calls. This is a chat only number.

Buy Health Insurance Online

9000+

Cashless Hospitals

3.8 Crore+

Lives Insured

8 Lacs+

Claims Settled

I agree to the Terms & Conditions

Get Exclusive Porting Benefits

Check Prices

Buy Health Insurance, Up to 20% Discount

Port Existing Policy

9000+

Cashless Hospitals

3.8 Crore+

Lives Insured

8 Lacs+

Claims Settled

Senior Marketing Associate

Srishti is a skilled content writer with 4+ years of experience in the insurance world. She simplifies tricky terms, explains policies clearly, and writes content that instantly connects with customers. Her skills make insurance easy to understand and truly helpful for everyone.

Chief Marketing Officer

Vivek comes with over 15 years of experience across different industries like FMCG, e-commerce and insurance. His expertise in the online space and consumer behaviour understanding is bringing new insights to Digit in making insurance simple.

Health insurance is like a safety net that helps you pay for medical care when you are sick or injured. You pay a certain amount regularly (called a premium) to the insurance company, and in return, they help cover the costs when you visit the doctor, undergo tests, or require treatment.

This includes expenses incurred during pre and post-hospitalisation, annual health check-ups, psychiatric support, critical illnesses and organ donor expenses, amongst others, as per your customised health insurance plan.

Think of it like that one friend who you know will always be there for you whenever you’re sick or even just feeling low.

Health insurance is needed to protect you financially and ensure you get the best medical care when needed. Here are some reasons why having a health insurance policy is important:

Financially Security

More than anything else, health Insurance is a smart investment to make that not only helps safeguard your health but also provides you with financial protection. It protects your savings and ensures that a medical emergency doesn’t turn into a financial crisis.

Rising Medical Costs

According to the National Family Health Survey-3, 70% of urban and 63% of rural households rely on private hospitals, where the cost of healthcare services is getting higher. This makes it harder for families to manage healthcare costs. Health insurance helps by covering a big part of these rising expenses.

Care for Chronic Illnesses

Many critical illnesses like cancer and heart disease are today diagnosed in young people <40. Health insurance ensures you will be financially covered in the event of the same. Some plans even cover health check-ups and vaccinations, helping you stay healthy.

Quick Access to Treatment

Health insurance makes it easier to get timely medical care in an emergency. With a good plan, you can visit hospitals or doctors without worrying about arranging money first.

Tax Savings

Who doesn’t want additional tax savings, right? According to Section 80D of the Income Tax, anyone who buys health insurance for themselves or their parents can claim tax benefits on the annual premium!

Peace of Mind

Knowing that your treatment costs are covered by health insurance, you can now focus on your health and recovery, rather than stressing about money. It’s a sense of security that helps you feel prepared for any medical situation.

If you believe that, read on:

Being healthy and having savings is great, but it’s not a substitute for health insurance. Medical expenses are unpredictable, and the cost of treatment is rising fast. According to the NSSO, 62% of Indians rely on personal savings for healthcare, and IRDAI reports that hospitalisation in private hospitals now costs more than ₹50,000+ on average.

Health insurance isn’t just about covering current risks; it’s about protecting your future. Buying a health policy while you’re young and healthy means lower premiums, better benefits, and uninterrupted coverage. Besides, one does not need to wait for a medical emergency to realise its value.

Shubham Sinha

Product Manager - Health

Individual Health Insurance

An Individual Health Insurance policy is one that you can buy to cover you, your spouse, children, and parents on an individual sum insured basis. This type of insurance policy covers your medical expenses for injuries and illnesses related to hospitalisation, surgery costs, room rent, daycare procedures, and more.

Ideal For: Young adults, self-employed individuals, or those without employer-sponsored plans.

Key Benefit: Each insured member receives a dedicated sum insured, providing enhanced financial protection in the event of multiple or simultaneous medical emergencies.

Family Floater Health Insurance

A Family Floater Health Insurance policy is one that you can buy to cover yourself and your family members under a single plan. This means that both your health insurance premium and sum insured will be shared among all members in the plan.

Ideal for: Families with spouses, children, and dependent parents.

Key Benefit: All insured members share a common sum insured, making it more affordable than individual plans.

Group Health Insurance

A Group Health Insurance policy is one that an employer or organisation buys to cover a group of individuals, especially the employees, under a single plan.

Ideal for: Employees in companies, members of associations, or organisations.

Key Benefit: It ensures financial protection for employees and can be extended to their families, making it a valuable part of employee benefits.

Senior Citizens Health Insurance

A Senior Citizen Health Insurance policy is designed specifically for individuals aged 60 years and above.

Ideal for: Seniors and retirees aged 60 and above.

Key Benefit: It provides higher sum insured options, cashless treatment, domiciliary hospitalisation and lifelong renewability.

Maternity Health Insurance

A Maternity cover can be bought as a rider along with the basic health insurance plan. All the expenses incurred in the prenatal stage, delivery and post-natal stage are covered.

Ideal for: Couples planning to start a family.

Key Benefit: It provides financial protection during pregnancy and childbirth, reducing out-of-pocket expenses.

Critical Illness Health Insurance

A Critical Illness Health Insurance policy provides a lump sum payout upon the first diagnosis of a serious illness such as cancer, heart attack, stroke, kidney failure, or major organ transplant.

Ideal for: Individuals with a medical history or those seeking extensive protection.

Key Benefit: It offers a one-time lump sum payment that helps cover high treatment costs, lifestyle adjustments, and non-medical expenses.

Super Top Up Health Insurance

A Super Top-Up Health Insurance policy offers additional coverage once your total medical expenses in a year exceed a fixed deductible. During a claim, the payment will be made in addition to the defined limit specified in the policy.

Ideal for: Individuals with limited employer health coverage.

Key Benefit: It works alongside your base health insurance or out-of-pocket payments, covering hospitalisation and major treatments beyond the deductible limit.

Buying health insurance at an early age has multiple benefits, including financial, medical and even emotional. Here’s why it's smart to have health insurance at a young age:

Lower Premium

The premium is lower at an early age because younger individuals are considered less risky and have a lower probability of making claims. This means you pay less for more coverage!

No Waiting Period

Most health insurance policies come with a waiting period, which is the time during which you cannot make any claims. Buying early helps you serve the waiting period while you are still healthy.

No Pre-Medical Tests

Most health insurance policies require pre-medical tests for individuals. Hence, by investing in a health insurance policy at an early age, you can skip the pre-medical tests and avoid any complications.

Your health insurance plan with Digit extends several exclusive benefits that enhance your coverage. Here are the key benefits:

* These add-ons are subject to underwriting approval and your eligibility at the time of purchase or renewal

Coverages

Double Wallet Plan

Infinity Wallet Plan

Worldwide Treatment Plan

Important Features

This covers for all hospitalisation expenses including due to an Illness, Accident, Critical Illness or even pandemics like Covid 19. It can be used to cover for multiple hospitalisations, as long as the total expenses are up to your sum insured.

You need to wait for a defined period from the first day of your policy to get covered for treatment related to any non-accidental illness. This is the Initial Waiting period.

Exclusive Wellness Benefits like Home Healthcare, Tele consultations, Yoga and Mindfullness and many more available on our App.

We provide a back-up Sum Insured which is 100% of your Sum Insured amount. How does Sum Insured Back Up work? Suppose your policy Sum Insured is Rs. 5 lac. You make a claim of Rs.50,000. Digit automatically triggers the wallet benefit. So you now have 4.5lac + 5 lac Sum Insured available for the year. However, one single claim, cannot be more than the base Sum Insured as in the above case, 5 lac. .

Digit Special

Digit Special

No claims in the Policy year? You get a bonus -an additional amount in your total sum-insured for staying healthy & claim free!

Different categories of rooms have different rents. Just like how hotel rooms have tarrifs. Digit plans give you the benefit of having no room rent cap, as long as it is below your Sum Insured..

Health insurance covers medical expenses only for hospitalisations exceeding 24 hours. Day care procedures refer to medical treatments undertaken in a hospital, requiring less than 24 hours due to technological advancement such as cataract, dialysis etc.

Digit Special

Get a world class treatment with the Worldwide Coverage! If your doctor identifies an illness during your health examination in India and you wish to get a treatment abroad, then we’re there for you.You’re covered!

We pay for your health check-up expenses upto the amount mentioned in your Plan. No restrictions on the kind of tests! Be it ECG or Thyroid Profile. Make sure you go through your policy schedule to check the claim limit.

There may be emergency life-threatening health conditions which may require immediate transportation to hospital. We absolutely understand this and reimburse for expenses incurred for your transportation to a hospital in airplane or helicopter.

Digit Special

Co-Payment means a cost sharing requirement under a Health Insurance Policy that provides that the Policyholder/Insured will bear a specified percentage of the admissible claims amount. It does not reduce the Sum Insured. This percentage depends on various factors like age, or sometimes also on your treatment city called zone based copayment. In our plans, there is no age based or zone based Co payment involved.

Get reimbursed for the expenses of road ambulance, in case you are hospitalised.

This cover is for all expenses before and after hospitalisation such as for diagnosis, tests and recovery.

Other Features

The disease or condition that you are already suffering with and have disclosed to us before taking the policy and has been accepted by us has a waiting period as per plan opted and mentioned in your Policy Schedule.

This is the amount of time you need to wait for, until you can make a claim for a specific illness. At Digit it is 1-3 years and starts from the day of policy activation. For the full list of exclusions, read Standard Exclusions (Excl02) of your policy wordings.

If You sustain an Accidental Bodily Injury during the Policy Period, which is the sole and direct cause of Your Death within twelve (12) months from the date of accident, then We will pay 100% of the Sum Insured as mentioned in Policy Schedule against this cover and as per plan opted.

Digit Special

Your organ donor gets covered in your policy. We also take care the pre and post hospitalisation expenses of the donor. Organ donating is one of the kindest deeds ever and we thought to ourselves, why not be a part of it!

Hospitals can go out of beds, or the patient’s condition may be rough to get admitted in a hospital. Don’t panic! We cover you for the medical expenses even if you get treatment at home.

Obesity may be the root cause of so many health issues. We absolutely understand this, and cover for Bariatric Surgery when it is medically necessary and advised by your doctor. However, we DONOT cover if hospitalisation for this treatment is for cosmetic reasons.

If due to a trauma, a member has to be hospitalised for a psychiatric treatment, it will be covered under this benefit, upto INR 1,00,000. However, OPD consultations are not covered under this. The waiting period for Psychiatric Illness Cover is same as Specific Illness waiting period.

Before, during & after hospitalisation, there are many other medical aids & expenditures such as walking aids, crepe bandages, belts, etc.,which need your pocket’s attention.This cover takes care of these expenses that are otherwise excluded from the policy.

Pre-Natal & Post-Natal Expenses

Pre-natal and post-natal medical expenses are not covered unless they lead to hospitalisation.

PED Before Waiting Period

A claim for a pre-existing disease or illness cannot be made until the specified waiting period is over.

Hospitalisation without Doctor’s Recommendation

Hospitalisation for any condition that doesn’t match the doctor’s prescription is not covered.

Enhance your health insurance policy with add-ons at Digit. These add-ons are subject to underwriting approval and your eligibility at the time of purchase or renewal. Here’s a list of add-ons available that provide additional layers of protection beyond the basic coverage of your policy:

Consumable Cover

Pay 10% extra premium and we will also cover your non-medical expenses once your base claim is approved.

Pre-existing Disease/Specific Disease/Initial Waiting Period Modification

You can reduce your pre-existing disease waiting period to up to 2 years.

Network Hospital Discount

Opt for treatment at one of our network hospitals and receive a 10% discount on your premium with this add-on cover. However, a co-payment will be applicable if you get hospitalised in a non-network hospital.

Not sure which health insurance policy to buy?

Talk to our advisor now!

We help you to choose the best health insurance plan basis your needs.

Schedule a Callback

You’ll hear back from our verified expert shortly.

Ideal coverage means having sufficient health insurance to cover your hospital bills without depleting your savings. An ideal health insurance plan is usually suggested to have a sum insured equal to at least half of your annual income.

You must check if it is sufficient to meet your medical expenses. Experts suggest buying a health cover of at least ₹10 lakhs to combat rising healthcare costs easily.

To choose the right sum insured for you and your family, here are a few important points to keep in mind:

Let’s face it! Hospital bills aren’t what they used to be. With medical costs going up faster, a ₹25 lacs health cover isn’t just nice to have - it’s a smart move!

This type of coverage acts like a strong umbrella in the event of a medical emergency. Experts at Digit recommend having ₹25 Lakhs coverage because:

Bonus Point: Opting for a higher sum insured early on can also help you lock in better premiums while you're still young and healthy. It’s an investment in your future self. 🙂

Choosing the right health insurance isn’t about picking the most popular plan; it’s about finding what fits you and your family. Start by considering these questions:

1. How old are you?

2. Do you have any existing health issues?

3. What’s your lifestyle like?

All these things help determine how much coverage you really need.

With hospital bills going up every year, even a short hospital stay can cost a lot. Hence, it’s safer to go for higher coverage, even if you’re healthy right now. And if you're on a budget, you can always start with a base plan and add a top-up later for extra protection.

Vivek Chaturvedi

CMO & Head of Direct Sales

You are a Young, Healthy Youth in the Late 20s or Early 30s, Earning, and Have a Few Financial Responsibilities

You Already Have a Corporate Health Cover & do Not Wish to Spend too Much on Health Insurance

You Have a Family to Take Care of and Want to Cover Spouse + Kids

You are Looking to Secure Your Parents

My Family Has a Critical Illness History, do I Need to Buy Any Additional Health Cover?

Choosing the right health insurance plan in 2025 isn’t just about picking the cheapest option; it’s about finding a plan that truly fits your lifestyle, health needs, and future goals. Here are some tips for choosing the best health insurance plan:

Coverage Benefits

To choose the right insurance plan, start by assessing your coverage needs and looking for plans that meet those requirements. Evaluate additional benefits like sum insured restoration, no-claim bonuses, value-added benefits, and annual health check-ups.

Pre & Post-Hospitalisation Cover

Check if the plan covers expenses incurred before and after hospitalisation, such as diagnostic tests, consultations, and post-hospitalisation expenses, including follow-up visits, medications, etc.

Waiting Periods

Check the waiting period in health insurance for pre-existing diseases, maternity, specific illnesses or surgeries. Consider getting a policy with a shorter waiting period so that you can claim sooner for any ongoing health concerns.

Customisation Options (Add-ons)

Customisation ensures flexibility. Hence, look for plans that allow customisation or add-ons, such as consumable coverage, network hospital discounts, etc.

Premium Amount

Premium amount is a crucial factor to consider before choosing a plan. The higher the premium, the better the coverage. Evaluate your monthly premium, deductible, and out-of-pocket costs to balance affordability with coverage.

Available Discounts

Some insurers offer discounts for various reasons, such as family floater policies, long-term policies, or if you maintain a healthy lifestyle (e.g., non-smoker discount). Explore available discounts to optimise your premium.

Ease of Claim Settlement

Our claim process is designed to be quick and hassle-free, with many claims settled in a very short span.

Hospital Networks

A wide cashless hospital network ensures access to quality care without financial stress. When purchasing a health insurance policy, always confirm whether or not the policy covers the major or closest hospitals to your home.

Renewability for Life

Ensure your plan offers a lifetime renewability option. This is crucial as medical needs increase with age and changing lifestyle and buying a new plan later will be difficult and costly.

Choosing the right health insurance plan can feel overwhelming, but it’s one of the most important decisions for your well-being and financial future. Here are the steps you must follow to select the right health insurance plan:

Let’s simplify it for you!

➤ Start by assessing what you require from your insurance.

➤ Next, consider your preferred doctors and hospitals.

➤ Then, evaluate the premium, deductible, co-pay, waiting period, coverage, and benefits.

➤ Additionally, look for benefits such as maternity coverage, wellness programs, or mental health services, which can be valuable as life changes.

➤ Finally, always review the terms and conditions carefully to avoid unexpected exclusions.

Remember! The more personalised the plan, the better. Choose wisely! 🙂

For Youngsters (18 - 30 years)

* Get insurance early in life, even if you're healthy.

* Opt for a higher sum insured plan; 5-10 lakhs should be sufficient.

* Ensure that you have critical illness cover included.

* Look for low premiums and a no co-payment clause.

For Families (30 - 60 years)

* Ensure that all family members are covered.

* Go for a high sum insured, as it is distributed among all family members. A family floater plan with ₹25 lakhs coverage is recommended.

* Check the waiting periods for all benefits being offered.

* If you include your parents, check if common treatments like knee replacement and cataract surgery are covered.

For Senior Citizens (60+ years)

* If you already have a plan, you can increase its sum insured with a top-up plan.

* Opt for a plan that includes no room rent, domiciliary coverage, and AYUSH coverage.

* Check if the plan you’re getting covers common treatments like knee replacement and cataract surgery.

* Check the waiting period mentioned for different pre-existing diseases.

Health Insurance for the Young & the Restless

We understand that young people are generally healthier. However, getting health insurance while you’re young means you will have cheaper premiums, cross waiting periods faster, can avail maternity benefits when the time comes and even use our OPD cover for minor treatments and injuries that can happen to just about anyone.

Health Insurance for the Great Indian Families

Health insurance for your family can be purchased in the form of a family floater plan or individual health insurance plans for each family member. With our special benefits such as no co-payment, zone-based discounts, good health discounts and more, our health insurance is perfect for families.

Health Insurance for the Old & the Wise

Whether you’re looking to protect yourself or your parents in their later years, our health insurance for senior citizens is specifically designed for the senior population. With benefits such as AYUSH treatments, home hospitalisation and no room rent capping, our health insurance understands precisely what your parents need.

Health Insurance for Fitness Enthusiasts

While health enthusiasts are less prone to illnesses, buying health insurance can reap benefits such as cheaper premiums and tax savings and also come in use in case of common workout injuries through our OPD benefit.

Health Insurance for Corporate Hotshots

You may already have corporate medical insurance that covers you. But do you know they’re often really limited? Hence, you should opt for a top-up health insurance plan to cover amounts exceeding your corporate plan.

Health Insurance for Employees

You are in human resources handling a large company or small enterprise, buying health insurance for your employees at an affordable premium won’t only ensure they’re protected but also keep them happier.

Buying health insurance online offers a faster, more transparent and cost-effective way to secure your health coverage. Here are some reasons why you must consider getting health insurance online:

A health insurance plan might come with a lot of attractive features, but those shouldn’t be the main reason to buy it. What’s more important are the basic benefits that actually help when there’s a medical emergency.

Here are the seven most important things one must consider, including no limit on the choice of room, sum-insured backup, cumulative bonus offering, zero co-payment, consumables coverage, pre and post-hospitalisation benefits and organ donor expenses coverage.

Don’t just pick a plan; understand it. Make a choice that stands strong when life throws the unexpected at you.

Vivek Chaturvedi

CMO & Head of Direct Sales

Comparing health insurance plans may seem a tiring task, but focusing on the right factors can make it easier. Here are the top tips to compare health insurance plans that offer the best coverage and protection.

See More

See Less

Buying or renewing a health insurance policy online is now as easy as booking a movie ticket. 🤩 With just a few clicks, you can compare different plans, customise your coverage, and ensure continued financial security in medical emergencies. Follow these simple steps to buy or renew a health insurance plan:

Enter Basic Details

Visit the Digit app or website. Enter your PIN code and mobile number, select your preferred health insurance plan and provide age details, family members covered, etc.

Choose Plan & Add Member Details

Compare & select the plan, sum insured, add-on covers and apply any available discounts to get the final premium amount. Further provide the member details for everyone you’re covering.

Make Payment & Submit KYC

Once done, proceed to make the premium payment and submit your KYC documents to complete the purchase process.

Final Review & Processing

Now, your application undergoes a brief review process. Digit may request a health declaration, lifestyle information, or medical details & reports if required. Now, based on your medical underwriting, your policy will be issued and sent to your email. You can also access it anytime through the Digit app.

When purchasing a health insurance policy, insurers typically require some basic documents for verification. Below is a list of optional documents that may be needed at the time of purchasing a policy:

Identity/Age Proof

✔ Aadhaar Card

✔ PAN Card

✔ Passport

✔ Voter ID

✔ Driving License

✔ Birth Certificate

Address Proof

Income Proof

Previous Medical Reports (If any)

KYC Documents

✔ PAN Card (for financial verification)

✔ Aadhaar Card (for identity and address verification)

✔ Photograph and bank details (optional)

Calculate your health insurance premium online in 2 mins. Here’s how:

Step 1

Log in to your Digit account by entering your PIN code and mobile number.

Step 2

Provide details of your family members, including the age of the eldest, then click "Continue" to customise your plan by choosing your sum insured, type of plan and add-ons.

Step 3

Review and apply any available discounts and enter further contact details. You can now see your customised premium amount.

Your health insurance premiums depend on several factors, including your age, lifestyle, location, and the type of coverage you select.

To know your premium in minutes, you can always use a health insurance premium calculator online to get quick and accurate estimates. However, let’s now look at how premiums vary at Digit, based on different zone classifications depending on your policy type:

Let's look at a practical example to understand how the premium works for one of our most popular health insurance plans, the 'Infinity Wallet Plan.'

Pritesh, a 35-year-old unmarried individual residing in Bangalore (Zone 2 city), has opted for the 'Infinity Wallet Plan' with a sum insured of ₹10 lakhs.

This table illustrates the starting premium amounts for a ₹10 lakhs sum insured under our Infinity Wallet Plan, varying by age group. The premium increases with age, reflecting the higher risk and potential medical costs associated with older age brackets.

Health insurance isn’t just about hospital bills and emergency coverage anymore; it’s about supporting your overall well-being every day. Wellness benefits in health insurance are additional features offered by Digit that reward you for maintaining a healthy lifestyle.

These benefits are designed to go beyond traditional coverage; wellness benefits offer access to preventive care, mental health resources, fitness programs, tele-consultations, and even discounts on dental care.

You also get access to monthly health sessions and wellness workshops through our WOW-12 campaign, which empowers you with the knowledge and resources to make healthier choices every day. 🙂

With your Digit’s Health Insurance, you can get exclusive access to a wide range of wellness perks, making taking care of yourself easier and more affordable:

Note: Please refer to the respective Service Provider’s T&Cs before availing services. Offers, including discounts or complimentary access, are subject to change.

Unlimited 24×7 Teleconsultations with General Physicians

Get expert medical advice anytime, anywhere.

Mental Health Consultation & Services

Consult the best and most trusted therapists at affordable rates, with up to 50% off.

Diagnostic Tests & Health Check-Ups

Stay ahead of health concerns with affordable screenings and lab tests.

Specialist Teleconsultations

Speak to top specialists in Mental Health, Women’s Health, Diet & Nutrition, and more, at flat 50%!

Women's Health Care Programs

Pregnancy Care Programs access to Mum Support Group, PCOS/PCOD Care Programs, Maternity Support, etc.

Physiotherapy Sessions

Stress and Pain relief covered with exclusive discounts on Physiotherapy consultation and session bookings.

Dental Consultation Offers

Avail unlimited, free dental consultations and exclusive discounts on dental treatments.

Sexual Wellness

Get flat 15% discount on Sexual Wellness Programs!

Chronic Care Support Programs

Personalised assistance for long-term health conditions.

After purchasing a health insurance policy, it is essential to download and keep a copy for future reference. With us, you do not need to carry hard copies of your insurance policy. You can simply download it from our website. 🙂 Follow these simple steps to download your policy document from the Digit website or app:

Log in to Your Account

Visit the Digit website or app and click on ‘Login’ at the top-right corner. Enter your registered mobile number and verify with OTP.

Visit ‘Active Policies’

Once logged in, navigate to the Active/My Policies section. Here, you can check the policy number, end date & start date.

Download the Policy

Done! You can save, share, print or email the policy for future reference anytime, anywhere.

To add or remove members from your Digit Health Insurance policy, follow these steps:

Once processed, you will receive a confirmation.

Filing or tracking a health insurance claim with Digit is easy and convenient. If you are filing for a cashless claim, confirm that your hospital is on Digit’s network list. Inform Digit in time, submit the pre-authorisation form via the hospital, and enjoy cashless treatment! 🙂 Here are the steps to file and track a claim:

Get Treated & Save Everything

Visit any hospital, pay the bills upfront, and collect all the necessary documents (bills, reports, prescriptions, discharge summary, etc).

Open Digit App & File Claim

Log in to the Digit App. Navigate to the ‘File a Health Claim’ section on the app. Choose the policy & type of claim you are filing and other details.

Submit all the Documents

Fill out the type of treatment, symptoms, hospital details etc. Scan and submit all the necessary documents in the desired format.

Register Claim & Relax

Click ‘Register Claim.’ We’ll review everything, and once approved, the amount will be reimbursed directly to your bank account.

Get cashless treatment at 9000+ hospitals across India

A cashless health insurance claim means the insurer directly settles your hospital bill with the hospital and you don't have to pay it upfront except for non-covered items. Here is how the cashless health insurance process works:

Visit a Network Hospital

Choose a hospital partnered with Digit.

Show Insurance Details

Present your health e-card or policy number and request approval.

Receive Treatment

Get treated without paying anything upfront (except deductibles).

Insurer Pays Directly

Digit will settle the bill directly with the hospital.

Pay Non-Covered Costs

You must pay any exclusions or extra charges.

A reimbursement claim works by allowing you to pay for your medical treatment upfront and then recover the eligible expenses from your health insurance provider. Here's a step-by-step explanation of how it works:

Get Treated at Any Hospital

Choose any hospital (network or non-network) for treatment.

Pay the Bills Yourself

Settle all the medical expenses upfront from your pocket and keep the bills.

Submit a Claim to the Insurer

Fill out the claim form and send it with the required documents.

Insurer Reviews the Claim

The insurer will verify the documents and approve the claim.

Reimbursement Process

Once approved, the insurer transfers the amount to your bank account.

When filing a health insurance claim, you need to submit certain documents to ensure a smooth and hassle-free process. Below is a list of essential documents that may be required while filing a health insurance claim at Digit:

Hospitalisation Documents

✔ Original hospital bills & payment receipts

✔ Detailed discharge summary

✔ All diagnosis reports (lab tests, imaging, etc.)

✔ Doctor’s consultation & prescription copies

✔ Pharmacy and medicine bills

Cashless Documents

✔ Duly filled & signed claim form (Available at the hospital or on Digit’s website/app)

✔ Diagnosis report for confirming the need for hospitalisation

✔ Health E-card

KYC Documents

✔ Aadhaar Card (Identity & address proof)

✔ PAN Card (Financial verification)

✔ Photograph

✔ Bank Details (Passbook or cancelled cheque)

Receiving a claim rejection can be frustrating, especially when you thought you had everything in order. Well, Digit Transparency Report for FY 2024-25 shortlisted some common and completely unavoidable reasons why your health claims get rejected and how to avoid them:

According to Digit’s Transparency Report, around 8% of health claims were rejected mainly due to waiting periods.

Many people think that once they have a health insurance policy, they won’t have to spend a single rupee during hospitalisation, but that’s not always the case. If you’re not careful while choosing your plan, you might still end up paying out of your own pocket.

Look closely at things like co-payment clauses, room rent limits, disease-specific sub-limits, and deductibles. These might sound technical, but they play a big role when you file a claim. The key is to go beyond just the premium and the coverage amount.

Take a few extra minutes to understand what the policy truly offers and what it doesn’t. That way, when you actually need to use your health insurance, you won’t be unprepared by unexpected expenses.

Vivek Chaturvedi

CMO & Head of Direct Sales

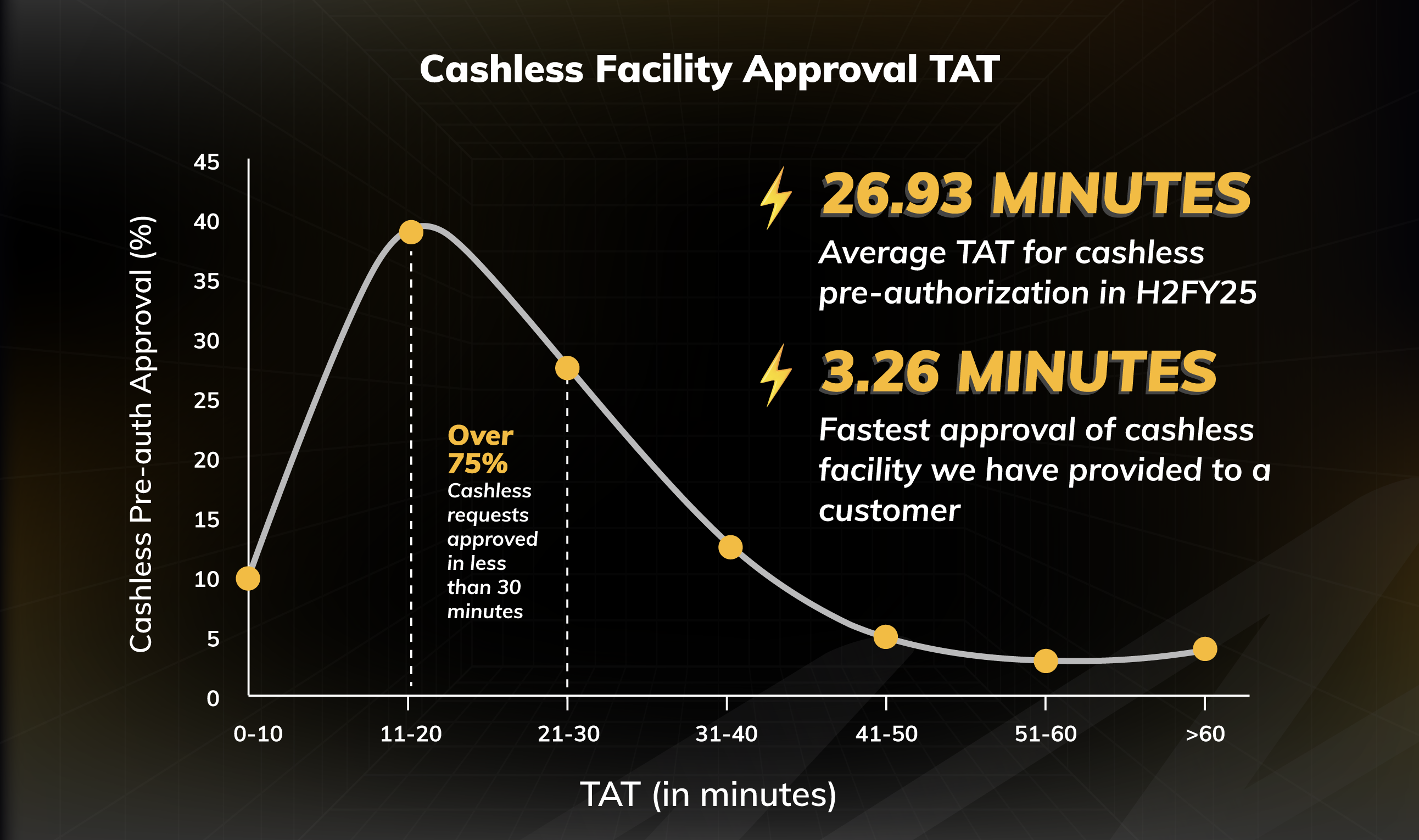

75% of Cashless Health Claims Approved in Just 30 Minutes at Digit

When you're in a hospital bed, the last thing you want is paperwork stress. That’s where cashless claim approval swoops in like a superhero. 🤩

At Digit, in the second half of FY 2024 - 2025, the average turnaround time (TAT) for pre-authorisation of health insurance cashless claims was a speedy 26.93 minutes. Even better? Over 75% of requests were approved within 30 minutes, making the process feel almost instantaneous.

Of course, some requests, around 3.3% took a little longer (over 60 minutes), mainly because they needed extra info or clarification from hospitals or customers.

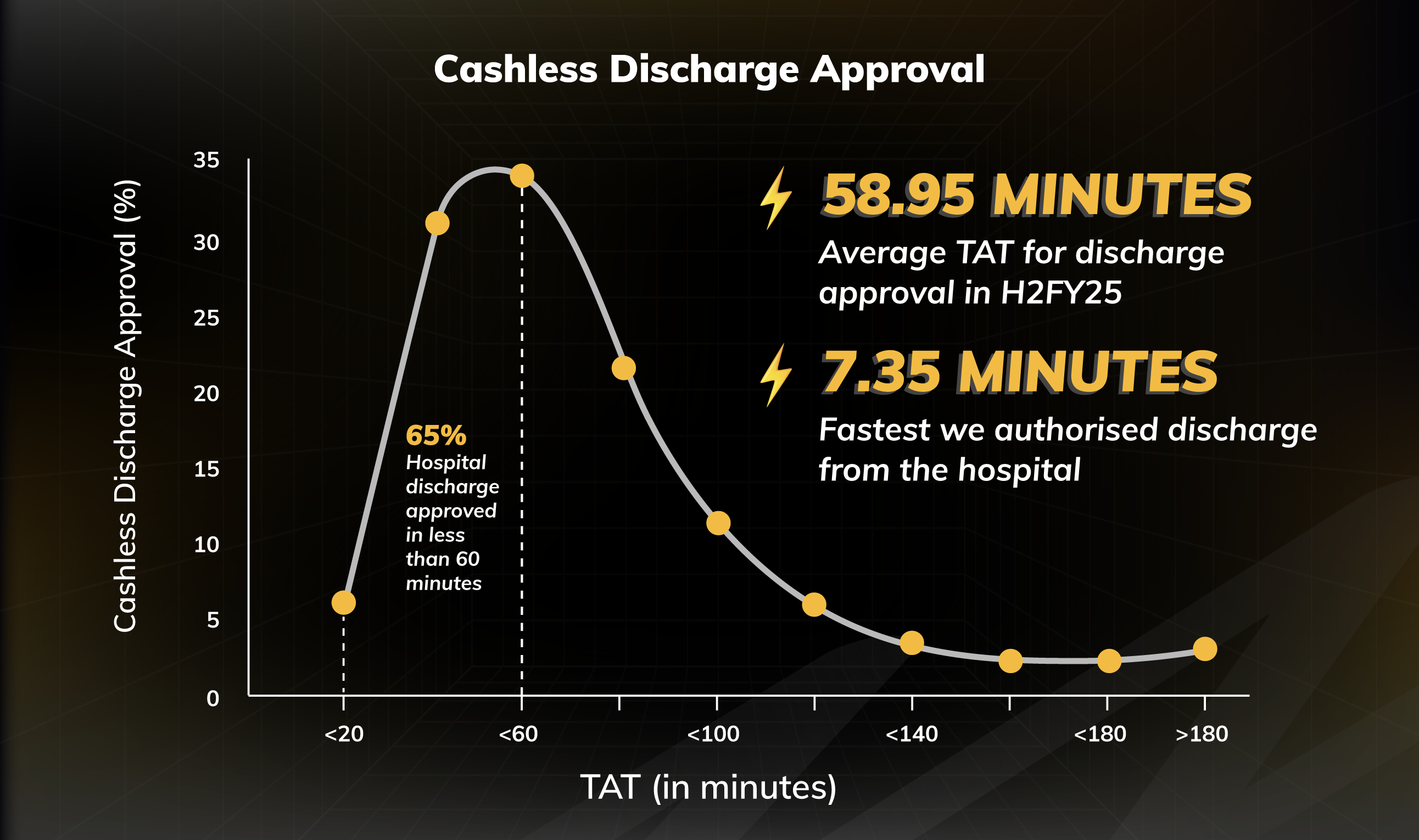

65% Cashless Discharge Approved in Just 60 Minutes at Digit

At Digit, in the second half of FY 2024-25, the average turnaround time (TAT) for hospital discharge approval in our health insurance was 58.95 minutes. Notably, 65% of discharge requests were completed within 60 minutes, ensuring patients aren’t left waiting once their treatment is finished.

While only 1.3% of cases extended beyond three hours, typically due to complex queries or pending clarifications.

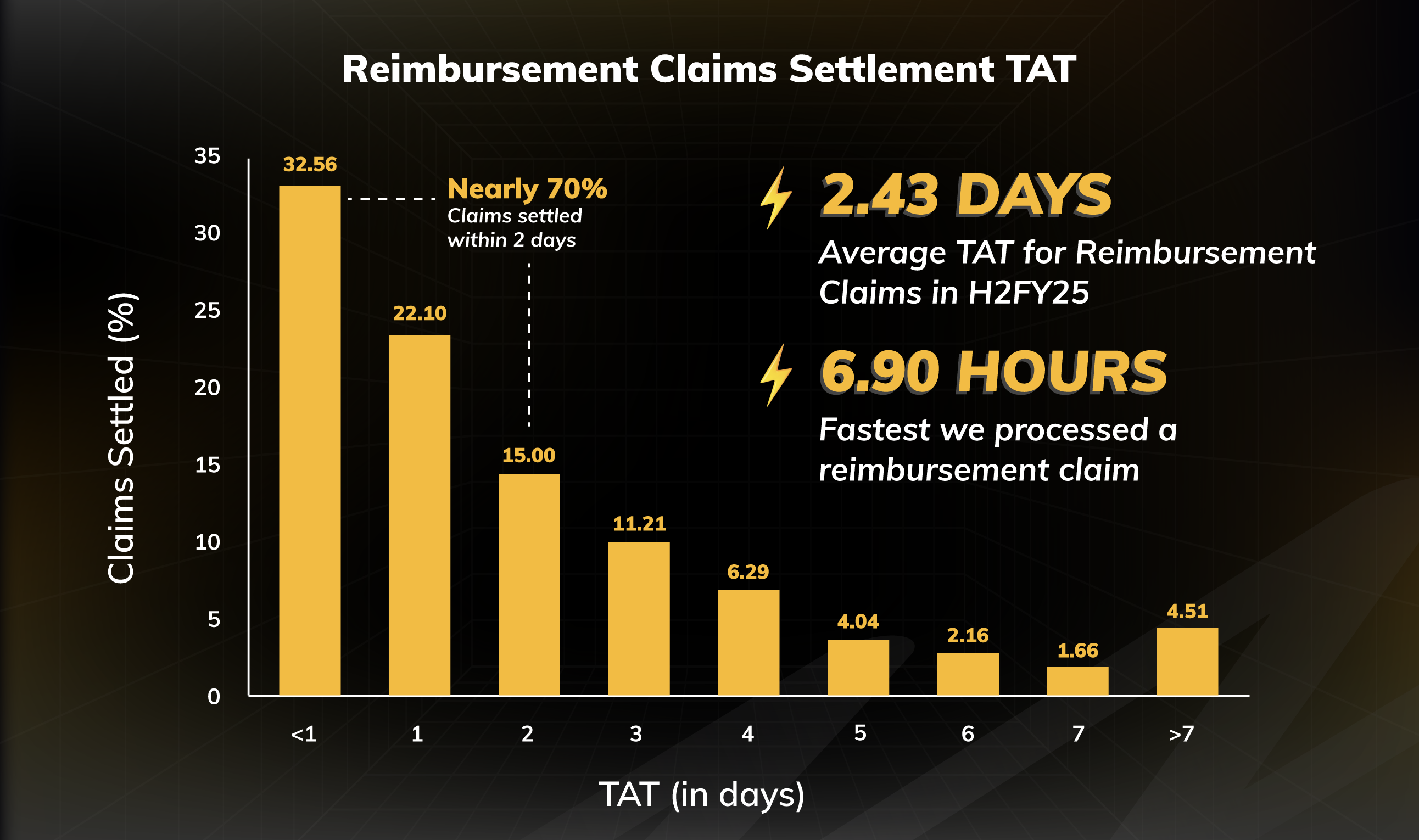

Almost 70% of Reimbursement Claims Settled in Just 2 Days

Not every hospital is part of a cashless network, and that’s where reimbursement claims come into play. Once all documents are submitted, the average turnaround time for processing a reimbursement claim at Digit in FY 2024-25 was just 2.43 days.

Nearly 70% of claims were settled within two days, providing quick relief to policyholders who initially had to pay out of pocket. While about 4.5% of claims took over a week to settle, usually due to missing documents or follow-up queries, the process is largely smooth and customer-centric.

1.1 Lakh+ Claims Registered Quickly with Smart Health Claim Bots in FY 2024-25

At the heart of smooth insurance experiences lies something you never see!! 😁

At Digit, our Health Claims Bots and Bulk Policy Issuance are quietly reshaping the way claims get processed. These smart systems fetch real-time data directly from the partner, eliminating manual uploads, reducing errors, and speeding up approvals for claims. In FY 2024-25 alone, they registered over 1.1 lakh claims, cutting down processing time.

No breaks and no delays. Fewer forms and faster care! ☺️

Highest Health Claim of ₹16.77 Lakh Settled by Digit in FY 2024-25

A Bengaluru customer faced a serious and complex medical condition, leading to a treatment bill running into lakhs. Digit settled its highest health insurance claim in FY 2024-25, amounting to approximately ₹16.77 lakh.

What mattered more was how quickly and transparently we stepped in. From the initial notification to the final settlement, the entire claim was handled with empathy, clarity, and minimal stress.

At Digit, it’s not the size of the bill that moves us; it’s the trust behind every claim we settle. 🙂

Over ₹27 Crore Settled for Pre and Post-Hospitalisation Expenses in FY 2024-25

At Digit, we believe health insurance is more than just hospital bills. This year, a patient undergoing treatment for malignancy received coverage not only for their hospitalisation but also for over 10 pre and post-hospitalisation visits, with a total payout exceeding ₹1.4 lakh. This reflects our commitment to supporting patients through every step of their recovery journey.

In fact, Digit paid out more than ₹27 crore this year alone towards pre and post-hospitalisation expenses, proving that genuine care extends before and after hospitalisation as well.

This is what we mean when we say insurance that supports the full journey, not just the hospital stay. 🙂

7,747 Babies Covered Under Their Parents' Policies in FY 2024-25

In FY 2024-25, Digit proudly covered around 7,747 babies under their parents’ policies, protecting the newest generation with the same care and commitment as every policyholder.

Among these little ones, the most popular baby names were Shivansh and Fatima, reflecting the diverse families Digit supports across India. 🙂

This wouldn’t be possible without Digit’s flexible family health plans, which automatically extend coverage to newborns, making it easy for parents to safeguard their little ones from day one.

The premium you pay towards a health insurance policy qualifies for a tax deduction under Section 80D of the Income Tax Act, 1961.

Section 80D allows individuals to claim a deduction of up to ₹25,000 from their taxes for health insurance paid within a particular fiscal year. However, senior individuals (above 60 years of age) can claim a deduction of up to ₹ 50,000 per financial year.

Therefore, people can benefit from tax savings under section 80D by buying insurance for themselves, their spouses, parents, and children.

The table below lists the section 80D tax benefits related to health insurance. It shows the maximum tax deductions for self, spouse, dependent children, and parents.

When it comes to health insurance, there's no shortage of myths, like “young people don’t need it” or “all illnesses are covered from day one.” These common misconceptions can keep you from making smart, timely decisions. Hence, here are some popular health insurance myths and the facts that everyone should know before buying a policy:

Waiting period

The amount of time you need to wait before you can start using any benefits of your health insurance policy.

Copayment

A copayment means that you and your insurer will split the bill, i.e., while your insurer will pay a large share of the bill, some part of it will have to be paid by you.

Sum Insured

Sum Insured in Health Insurance is the maximum amount your health insurer will be able to cover for you in one year.

Daycare Procedures

When one needs to be admitted to the hospital for a treatment or operation that lasts less than 24 hours, these procedures are referred to as daycare procedures in health insurance.

Pre-Hospitalisation Expenses

Medical bills go beyond what you need to pay for your stay in the hospital. Medical expenses incurred before hospitalisation are called pre-hospitalisation expenses. For eg: Expenses due to diagnostic tests.

Cumulative Bonus

When you don’t make any health insurance claims during the year, your insurer will increase your sum insured without charging you any extra premium for it. This increase in your sum insured is called a cumulative bonus.

Deductible

Some health insurance plans require you to pay out of your pocket before they can cover you. This amount is referred to as a deductible in health insurance. This amount is typically determined by you when purchasing your health insurance policy.

Pre-Existing Disease

Any disease or health condition that you have already shown symptoms of or received treatment for before buying a health insurance policy is known as a Pre-existing disease.

Portability

When you’re not satisfied with your current health insurer and want to switch without losing out on waiting periods, this process is known as portability in health insurance.

Health insurance is a significant investment that provides financial security in the event of a medical emergency. Consider the following scenarios where you may want to reconsider not having health insurance:

1. My Employer is Taking Care of my Health Insurance; I do Not Need One:

While it is great that your employer provides health insurance, it may not be sufficient. Employee health insurance may have limitations, such as a lower sum insured or coverage that may not meet your needs adequately.

Additionally, an employer's health insurance coverage typically extends only during your tenure with the company. Once you switch jobs and if there is a break between the next employer's coverage, you are left without any insurance coverage in that period.

2. My 5 lac Sum Insured is Sufficient to Cover Even Serious Illnesses if Such a Day Arrives:

You might have health insurance, but with a low sum insured. A low sum insured may not be sufficient to cover medical expenses in the event of serious illness-related hospitalisations. It is essential to review your health insurance policy and consider increasing the sum insured to meet your specific needs.

3. I am a Government Employee, Have Coverage for the Entire Family Under the Government Scheme, and I Don't Need an Extra Personal Health Cover:

As a government employee, you may have health coverage under certain government health schemes; however, please note that such facilities are available only at a few select medical centres, generally concentrated in major metropolitan cities. Hence, it is recommended to have an additional personal health insurance policy to cover emergencies when government facilities may not be readily accessible.

4. I Just Needed a Basic Health Insurance Policy, So I Purchased One with a Low Premium and Limited Coverage. I feel it's Just Fine:

You may opt for a lower-premium health insurance policy with limited coverage. While this may save money in the short term, it may not provide adequate coverage when needed. It is essential to strike a balance between premium and coverage, choosing a policy that offers sufficient coverage for your needs.

5. I Have Saved Enough Tax Under Different Sections of IT and Hence, I Don't Need Health Insurance for Saving Tax:

While health insurance can save additional taxes under Section 80D of the Income Tax Act, it should not be viewed only as a tax-saving tool. The primary function of Health insurance is to provide financial security and peace of mind in case of medical emergencies.

6. I am Young, Fit, and Fine. I do Not Need a Health Insurance Plan:

While you may be young and healthy now, medical emergencies can occur unexpectedly. Having health insurance can provide financial security and help you cover the cost of medical treatments and hospitalisation. Also, investing in health insurance at a young age can help you secure a lower premium and accumulate cumulative bonuses over time.

You can also find our product on

Determining the "best" health insurance plan in 2026 is subjective and depends heavily on individual needs and circumstances. Factors like age, family size, medical history, budget, and desired coverage play a crucial role in selecting the right plan.

Digit's Infinity Wallet plan is generally considered one of Digit's top-tier health insurance plans. Its unique features like unlimited backup sum insured, comprehensive coverage and user-friendly claim process make it a strong contender for the title of "best health insurance plan".

Life Insurance is a long-term policy that helps pay out the claim amount to the insured person’s family after death. One of the most popular and affordable types of life insurance is term insurance, which provides coverage for a specific period and ensures financial security for your loved ones in case of an untimely demise.

Whereas health insurance is to help pay for healthcare and medical expenses of the insured, that can occur due to illnesses, diseases, and accidents.

Follow these simple steps to renew your Digit Health Insurance hassle-free:

You can buy Digit Health Insurance plan for your family in two ways:

A free-look period is a certain period given to the insured by the insurer to assess whether the policy aligns with the insured’s expectations. The free look period typically lasts for 30 days.

If you find any clauses or conditions that don’t meet your requirements, you can choose to return the policy within this free-look period.

As per the IRDAI Regulation, the Company shall settle or reject a claim, as the case may be, within 30 days from the date of receipt of the last necessary document.

“Bank rate” shall mean the rate fixed by the Reserve Bank of India (RBI) at the beginning of the financial year in which claim has fallen due.

Whether 2 lakh sum insured is enough depends on several factors like your family's age, medical history, and the city you live in. Medical costs can be high, particularly in metro cities.

Digit offers plans with sum insured options ranging from 5 lakh to 1 crore. Consider your financial situation and potential healthcare needs when choosing the sum insured.

The answer is simple. The younger you are, the lower your starting and subsequent premiums. Also, if you are younger, you’ll easily pass the waiting period for various covers to be valid. Youngsters may not be financially secure, and hospitalisation and other medical expenses could be hard to meet.

Hence, it's advantageous to take health insurance early in life. As soon as you start earning.

Yes, an NRI can buy health insurance in India. The coverage can be used for treatments in India. However, the terms and conditions depend on your Insurance provider.

Additionally, it is also recommended to buy health insurance policy for NRI’s parents living in India.